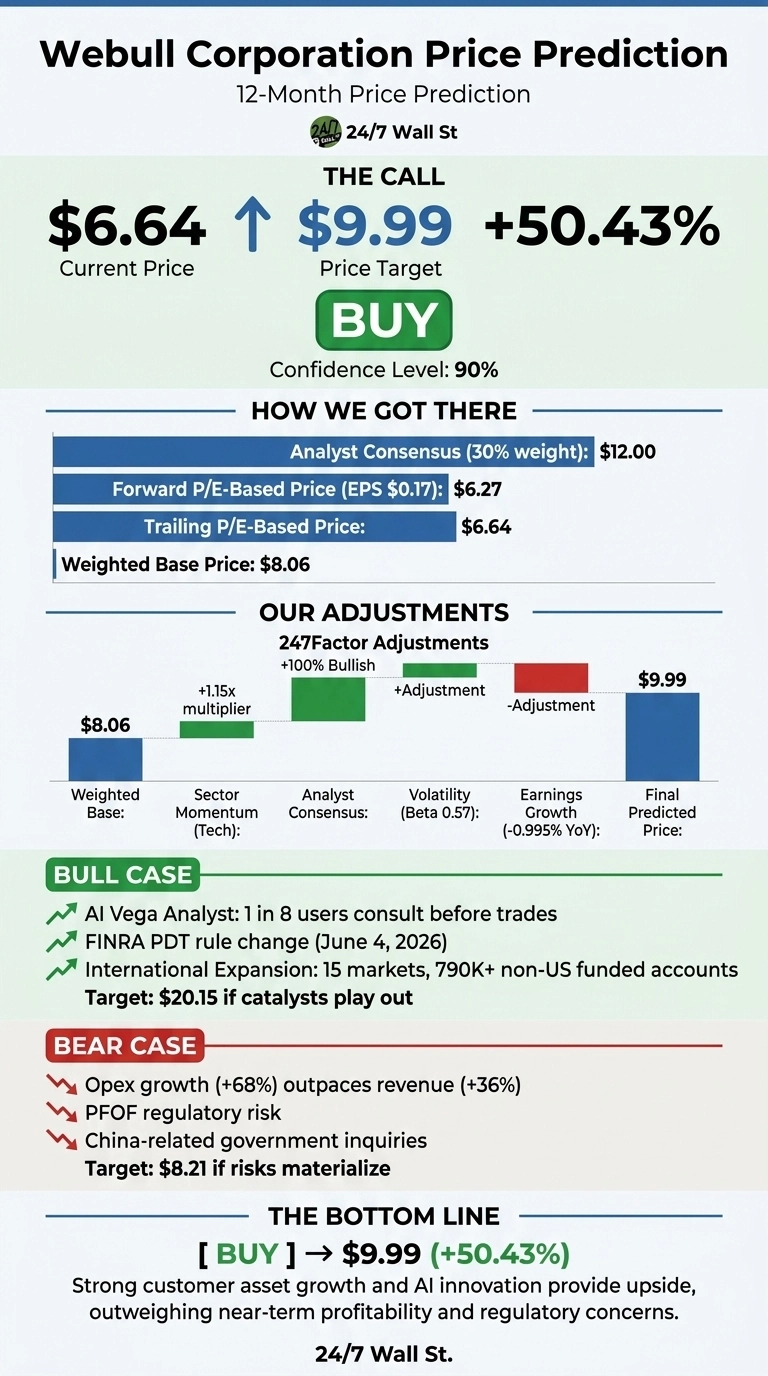

I’m starting with the punchline. Webull (NASDAQ:BULL | BULL Price Prediction) trades at $6.64 after a brutal twelve months, and our proprietary model sees meaningful room for recovery.

Our 24/7 Wall St. price target for Webull is $9.99, implying 50.43% upside over the next 12 months. The recommendation is buy at a 90% confidence level, which we consider high conviction.

| Metric | Value |

|---|---|

| Current Price | $6.64 |

| 24/7 Wall St. Price Target | $9.99 |

| Upside | 50.43% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Brutal Year, A Recovering Stock

Webull is down 36.28% over the past year and 14.54% year to date, with shares sitting 34% below the 52-week high of $18.32 and well off the $4.50 low. Encouragingly, the stock has rebounded 7.44% in the past month.

Webull’s most recent quarter showed divergent signals. Revenue grew 36% year over year to $159.93 million, equity notional volume surged 104% to $261 billion, and customer assets jumped 90% to $24 billion.

But marketing expense more than doubled to $49.41 million, pushing Webull to a GAAP net loss of $21.72 million and EPS of -$0.04. The full year 2025 still delivered revenue of $570.99 million, up 46.3%.

The Case for $20+

Our model’s bull case projects Webull at $20.15 in 12 months, a 203.49% return. The catalysts are real: the FINRA pattern day trader rule change on June 4, 2026 should accelerate active trading, the AI Vega Analyst is already being consulted by 1 in 8 users before trades, and Webull now operates across 15 markets with 790,000+ funded accounts outside the U.S. and APAC customer assets above $4 billion.

Analyst targets back the bull thesis. All 3 covering analysts rate it Buy with an average target of $12, and at the time of the Q3 2025 earnings report, multiple firms carried targets in the $15 to $18 range. Partnerships with BlackRock, Coinbase Prime, and Meritz Financial extend the moat.

What Could Go Wrong

The bear case lands at $8.21 over 12 months, still positive but reflecting real risk. Operating expenses grew 68% in Q1 against 36% revenue growth, a worrying inversion. Payment for order flow regulatory risk hangs over the entire business model, and government inquiries tied to China connections remain unresolved. The forward P/E of 37 leaves little margin for execution missteps.

That said, bulls would argue the opex spike reflects deliberate investment in international licensing, Vega AI development, and the doubled marketing push that drove customer assets up 90%. Adjusted operating profit of $14.82 million in Q1 still demonstrates underlying profitability beneath the GAAP loss.

Webull Price Prediction 2026-2030

My verdict is buy with our 24/7 Wall St. price target of $9.99 and 90% confidence. The tipping factor is the gap between operating fundamentals (customer assets up 90%, DARTs up 42%) and the depressed share price near 52-week lows.

The bullish thesis holds if marketing spend converts to durable account growth and AI Vega drives engagement. The thesis weakens if PFOF regulatory action accelerates or international expansion costs balloon further.

Looking further ahead, here is where our model projects Webull could trade, assuming current growth trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $9.99 |

| 2030 | $20.42 |

These projections assume Webull continues executing on international expansion and AI monetization. Significant upside could come from a successful B2B clearing buildout, while downside risk centers on PFOF regulation or China-related disclosures.

Contact [email protected] for any questions or corrections.