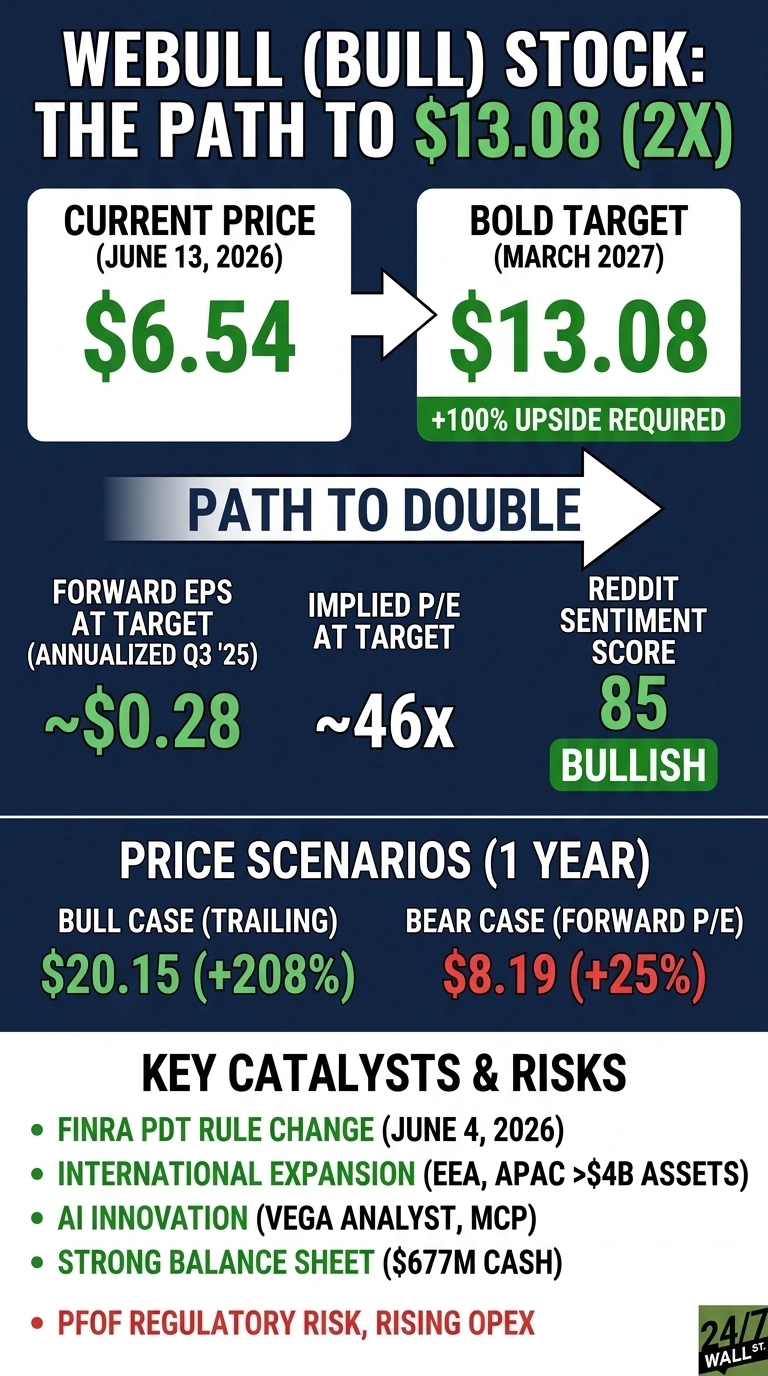

Webull (NASDAQ:BULL | BULL Price Prediction) runs one of the fastest-growing retail brokerage platforms globally, with more than 27 million registered users and operations across 15 markets. Yet shares trade at $6.54, down 15.83% year to date.

Q1 2026 revenue jumped 36% to $159.93 million, customer assets climbed 90% to $24 billion, and equity notional volume doubled to $261 billion. Can BULL double to $13 by 2027?

Why Webull Shares Are Stuck Despite Triple-Digit Growth

The disconnect is profitability. Webull posted a Q1 2026 GAAP net loss of $21.72 million, a swing from +$13.09 million a year earlier. Marketing and branding expense more than doubled to $49.41 million, and total operating expenses rose 68% versus revenue up 36%. That cost structure spooked traders.

BULL is down 38.94% over one year and 7.63% over the past month, though shares popped 16.79% last week. One Quiver Quantitative headline summed it up: “Webull slides as investors digest Q1 loss and sharply higher expenses.” With a beta of 0.57, this is fundamentals-driven. The market wants proof that growth spending converts to earnings.

Wall Street Sees 83% Upside. Our Model Says 52%

Every covering analyst is bullish. Three Buy ratings, zero Holds, zero Sells, with a consensus target of $12, implying 83.49% upside. Northland Securities’ Michael Grondahl targets $14.

Our model is more conservative. The base case is $9.97 over the next year, a 52.43% upside with 90% confidence. The bull case reaches $20.15, the bear case sits at $8.19.

Wall Street likely has it closer to right. With 100% bullish analyst sentiment and regulatory tailwinds, the gap between $9.97 and $12 looks like model conservatism.

The Path to $13 Per Share

Reaching $13 from $6.54 requires a 98.8% gain. Effectively a double.

With forward EPS near $0.15 (annualizing Q1 estimates near $0.03 to $0.05), $13 implies a forward P/E of 87x. Our $9.97 base case implies roughly 66x, so the bold target requires 21x additional multiple expansion. If forward EPS scales toward Q3 2025’s $0.07 quarterly run rate (~$0.28 annualized), $13 implies only 46x.

What drives EPS there? The FINRA PDT rule elimination on June 4, 2026 opens active trading to smaller accounts. CEO Anthony Denier said “The demand from sophisticated, self-directed investors, including institutional and B2B clients, has never been greater.”

Add the MCP server launch enabling AI-driven trading, EEA expansion, and a $100 million buyback, and the EPS ramp is plausible. Risk: PFOF regulatory action could gut the largest revenue line.

Valuation vs. Earnings Power

At $6.54, shares sit 34% below the 52-week high of $18.32 and well above the low of $4.50. On a price-to-sales basis, BULL trades at roughly 4.94x, reasonable for a brokerage growing revenue 46% annually.

Five-year performance shows a 45.59% decline, reflecting the SPAC-era reset rather than business deterioration. With $677 million in cash and a 98.4% funded account retention rate, the operating moat is real. The question is whether 2026 marketing spend converts to durable 2027 earnings.

$13 Is a Stretch, But Possible

Reaching $13 requires a 98.8% gain and a forward multiple of 87x on current EPS or roughly 46x on a normalized run rate.

Three things must break right: PDT-driven trading volumes must lift order flow revenue, international expansion must generate measurable contribution, and marketing spend must throttle back so adjusted operating profit rebuilds from the $14.82 million Q1 2026 level. A PFOF regulatory crackdown would derail the thesis. We’ve outlined the blueprint for how Webull could reach $13 in 2027.

Contact [email protected] for any questions or corrections.