For much of the past year, investors have been focused on one question: When will the Federal Reserve finally start cutting interest rates?

That expectation helped fuel one of the strongest stock market rallies in recent memory. Investors largely assumed that once inflation cooled, lower rates would follow. But what if the new Fed chair has a very different idea of what victory over inflation actually looks like?

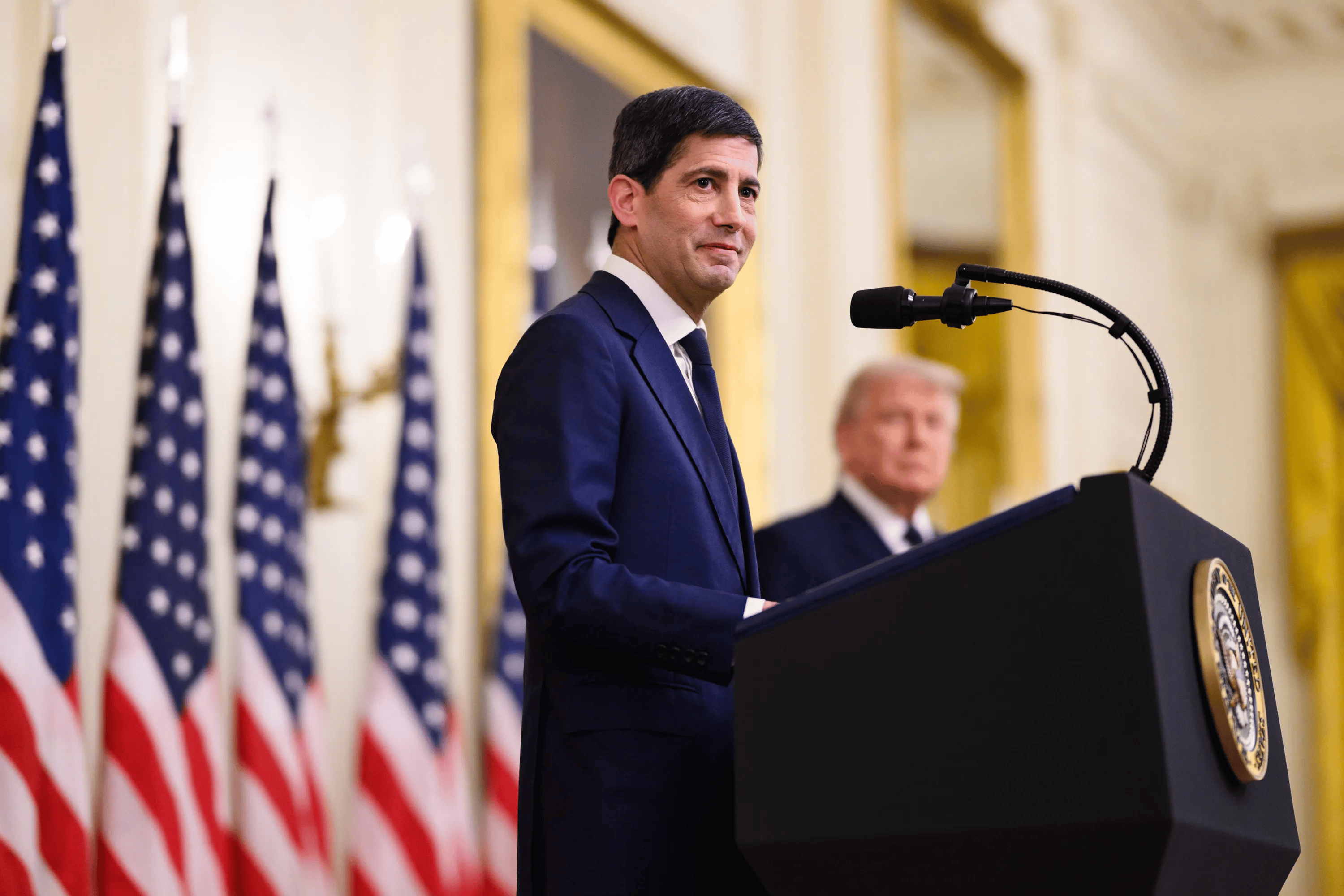

That’s the question Wall Street may soon have to answer after Kevin Warsh succeeded Jerome Powell as Federal Reserve chair following his swearing-in ceremony at the White House on May 22. President Trump selected Warsh in large part because he believed Powell had been too slow to cut rates and was unnecessarily restraining economic growth.

Yet buried within 2-1/2 hours of testimony before the Senate Banking Committee in April was an 18-word statement that could force investors to rethink everything they believe about future Fed policy.

The Quote That Changes Everything

The Federal Reserve has long operated with a clear inflation target: 2%. Whether policymakers are discussing the Personal Consumption Expenditures Price Index, the Consumer Price Index, or inflation expectations, the 2% target serves as the central guidepost for monetary policy decisions.

Warsh’s comments suggest he may be looking at the problem through a different lens. During his testimony, Warsh said:

“I believe that price stability should be a change in prices such that no one’s talking about it.”

At first glance, the comment sounds harmless enough. But investors may be overlooking its implications.

Inflation currently stands at 3.8%, up from 3.3% in March. Conventional wisdom says Warsh would focus on driving inflation back toward the Fed’s 2% target before easing policy aggressively. His statement says something different.

Price stability, in Warsh’s view, may not be defined by a specific percentage. Instead, it appears tied to public perception and confidence. If consumers, businesses, workers, and investors are still talking about inflation, then inflation remains a problem regardless of what the official data says.

Why Wall Street May Be Getting This Wrong

Warsh has long argued that the Federal Reserve became too involved in financial markets. He has repeatedly advocated shrinking the Fed’s balance sheet, which currently stands at $6.7 trillion, according to Federal Reserve data. While that is down $9 billion from the prior week, it remains $31 billion higher than a year ago.

That balance-sheet reduction effort matters because it provides an alternative form of tightening. Many investors assume Warsh will simply cut rates faster than Powell would have. Surprisingly, his inflation philosophy could point in the opposite direction.

If restoring the Fed’s credibility becomes the primary objective, Warsh may be willing to tolerate slower economic growth and softer labor markets in exchange for permanently anchoring inflation expectations.

That could mean:

- Interest rates remain elevated longer than markets expect.

- Rate cuts arrive later than investors currently anticipate.

- Quantitative tightening accelerates.

- The Fed prioritizes inflation credibility over supporting asset prices.

In other words, Warsh may seek to make the Fed appear less like a market participant and more like a neutral guardian of monetary stability.

A Dangerous Setup for Stocks

That’s where the risk emerges. Today’s stock market is priced around expectations that borrowing costs will eventually move lower. High-growth technology companies, in particular, derive much of their valuation from future earnings streams that become less valuable as interest rates rise.

Granted, Warsh may ultimately pursue lower rates than Powell would have. But if his definition of inflation extends beyond simply reaching 2%, investors could face a much longer period of monetary restraint than currently expected.

There’s another possibility that could prove even more disruptive. If inflation becomes a more fluid concept under Warsh’s leadership — defined less by a specific numerical target and more by public attitudes toward pricing pressures — the entire framework investors use to predict Fed policy could change.

Markets thrive on certainty. A clearly defined 2% target provides one. A standard based on public perceptions is harder to model.

Key Takeaway

In short, Wall Street may be focusing on the wrong part of Kevin Warsh’s record. Investors see a Fed chair appointed by a president who wanted lower interest rates. What they may be missing is a policymaker who appears deeply concerned with restoring the Federal Reserve’s credibility after the inflation surge of recent years.

Those 18 words suggest that defeating inflation, in Warsh’s view, is about more than reaching a statistical target. It’s about eliminating inflation as a topic of conversation altogether. That standard could require rates to stay higher for longer than investors expect. In some circumstances, it could even justify raising them.

And if a stock market priced for rate cuts suddenly finds itself confronting tighter monetary policy instead, today’s record highs may look far less secure than they do right now.