Joby Aviation (NYSE:JOBY | JOBY Price Prediction) is finally turning into a revenue story. Q4 2025 brought $30.84 million in quarterly sales (up 55,965% year over year) thanks to the Blade passenger acquisition, and management guided 2026 revenue to $105 million to $115 million.

Yet shares closed at $11.90 on May 29, down 9.85% YTD. Can JOBY hit $20 in 2027?

Why JOBY Shares Are Stuck Despite Real Commercial Progress

The disconnect is real. JOBY rallied to a 52-week high of $20.95 before unwinding to a low of $7.33. The stock is up 36.78% in the past month and 8.97% in the past week, but still in the red year to date.

Three factors are pinning the stock down:

- Cash burn: Operating cash flow ran -$509.89 million in FY2025, forcing the $1.2 billion February capital raise that diluted shareholders.

- Insider selling: CEO Joeben Bevirt disposed of 322,019 shares at $10.38 on May 15 alone.

- Beta of 2.61: JOBY moves 2.6x harder than the market in both directions.

Wall Street Sees Downside. Our Model Sees Range.

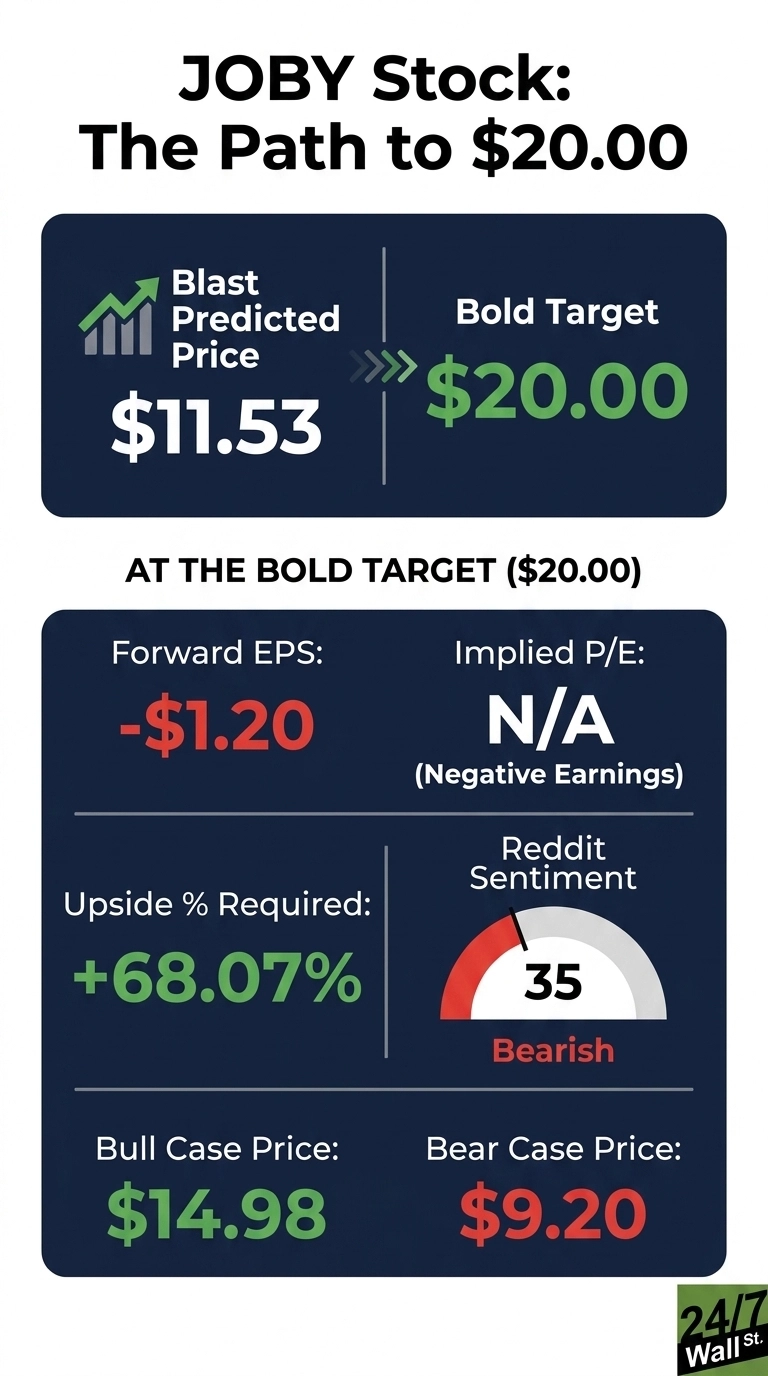

Wall Street is unusually split. The consensus target is $11.12, slightly below today’s price. The 11 analysts covering JOBY break down to 1 Strong Buy, 2 Buy, 5 Hold, 2 Sell, and 1 Strong Sell. Bullish and bearish percentages are dead even at 27%.

Our model lands at $11.53 base case (a -3.1% return) with medium confidence. The bull scenario stretches to $14.98, a 25.92% gain. Every analyst on this stock is modeling a pre-certification company. The minute FAA Type Certification flips to “granted,” the entire valuation framework changes overnight.

The Path to $20 Per Share

Reaching $20 from today’s price of $11.90 would require a gain of 68.1%. With forward EPS of -$1.20, a price of $20 implies a forward P/E of -17x, versus today’s -10x. Negative earnings make P/E useless, so the real story is price-to-sales.

JOBY trades at a TTM P/S of 150.7. Against 2026 revenue guidance of $110 million midpoint, $20 implies roughly a 179x sales multiple, expensive but not unprecedented for a pre-revenue aerospace platform with certification visibility.

What gets us there: FAA “for credit” test flights in 2026, first paying passengers in Dubai, and execution on the Toyota, ANA, and Abdul Latif Jameel orders worth over $1 billion in disclosed sales.

CEO Bevirt put it bluntly: “2026 will mark a key inflection point for Joby… we’ve begun to shift our focus from how and when we’ll go to market, to how many aircraft we can produce and where to deploy them.” Primary risk: any FAA certification slip past 2027 collapses the thesis.

The Valuation Case for Joby Right Now

JOBY trades at a TTM P/S of 150.7 with profit margins deeply negative (EPS of -$1.14). The 50-day moving average sits at $9.47, well below the 200-day at $12.85, showing recent technical weakness.

Shares are 47% below the 52-week high. Over five years, JOBY has returned 19.6%, badly trailing the market. The valuation case requires faith that 2026 revenue lands in the guided range and that the Dubai launch creates a repeatable template.

Is $20 Realistic?

Hitting $20 needs a 68.1% gain from here. It is a stretch, though achievable under the right conditions.

Three things must happen: FAA “for credit” test flights complete on schedule, Dubai carries first paying passengers without operational hiccups, and 2026 revenue hits the high end of the $105 million to $115 million range. What derails it: a certification delay into 2028 or another dilutive capital raise. We’ve outlined the blueprint for how Joby Aviation could reach $20 in 2027.

Contact [email protected] for any questions or corrections.