Credo Technology (NASDAQ:CRDO | CRDO Price Prediction) has become one of the loudest AI infrastructure stories on the Nasdaq, with numbers starting to justify the noise.

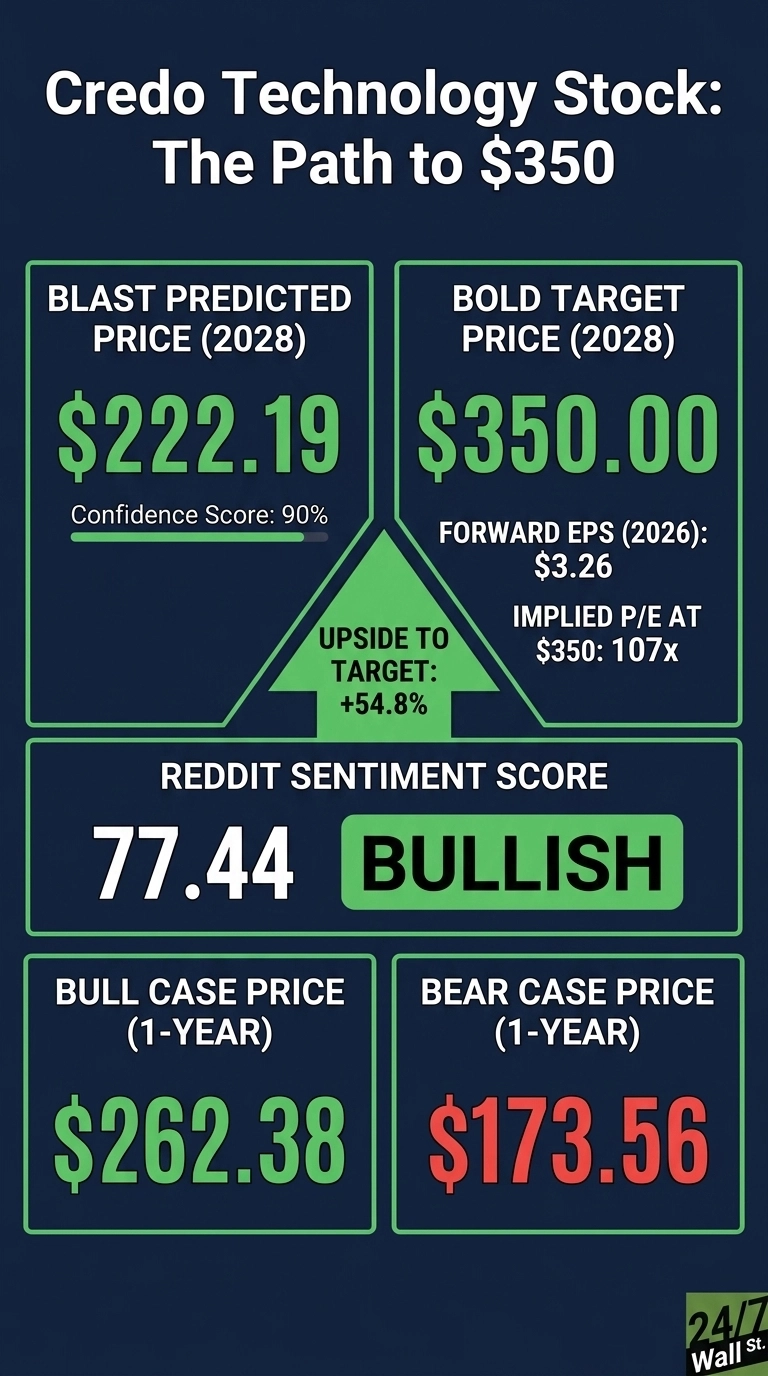

Fiscal 2026 revenue more than tripled to $1.335 billion, non-GAAP net income jumped more than 5x to $662 million, and shares are up 270.9% over the past year. The stock closed at $226.10. The question is whether Credo can hit $350 per share by 2028, and what has to go right.

What’s Holding Credo Back Right Now

For all the year-over-year gains, Credo is wobbling at the highs. Shares fell 4.21% in the most recent session and sit 12% below the 52-week high of $240.81. The one-week move is still +3.52% and the one-month performance is +22.63%, so this looks like a digestion phase.

With a beta of 3.18, Credo amplifies every twitch in AI sentiment. Management flagged near-term gross margin compression as ZeroFlap, ALCs, and OmniConnect ramp, and inventory has been building. The bull case remains intact. The volatility is the price of admission.

Wall Street Sees Modest Upside. Our Model Sees Less

The consensus target sits at $211.86, below current share price. Coverage skews heavily bullish with 4 Strong Buys, 12 Buys, and 1 Hold and a 94% bullish sentiment split.

Our base case is $222.19, implying -1.73% over the next year at 90% confidence. The bull scenario stretches to $262.38, the bear to $173.56. Analysts have not yet refreshed targets for the blowout FY2026 earnings report, and consensus is stale.

The Path to $350 Per Share

Reaching $350 from today’s $226.10 requires a 54.8% gain. With forward EPS of $3.26, a price of $350 implies a forward P/E of 107x. Our base case of $222.19 already implies 73x, meaning the bold target requires 34x additional multiple expansion. That is substantial.

CEO Bill Brennan framed it directly: “As we enter into fiscal 2027, Credo expects to achieve continued strong financial performance with our innovative and vertically integrated approach that enables customers to accelerate cluster time-to-stability, maximize GPU utilization, improve network reliability, and reduce overall infrastructure power and operating costs.”

Three new multi-billion-dollar TAMs (ZeroFlap optics, Active Line Cards, and OmniConnect) provide the EPS lever. If FY2028 EPS roughly doubles, $350 stops looking like multiple expansion and becomes earnings catching up. The primary risk is hyperscaler capex digestion, which would gut both the multiple and growth rate.

Where Credo Trades Today vs Its Earnings Power

At $226.10 against $3.26 of forward EPS, Credo trades at roughly 69x forward earnings. That is rich yet below the trailing P/E of 128, indicating forward estimates assume real earnings growth. Shares sit between a 52-week low of $66.75 and a high of $240.81. The five-year return is +1,840.77%. Pricey on today’s numbers, reasonable if FY2027 and FY2028 deliver.

The Bottom Line on $350

Hitting $350 by 2028 requires a 54.8% gain, with the multiple eventually settling to 107x forward earnings or earnings catching up to lower it.

Three things must go right: hyperscaler AI capex stays aggressive through 2027, ZeroFlap and OmniConnect scale into the multi-billion-dollar opportunities management has telegraphed, and gross margins hold near 68.3% non-GAAP level through product ramps. A hyperscaler order pause would derail it fastest. We’ve outlined the blueprint for how Credo Technology could reach $350 in 2028.