Shopify (NASDAQ:SHOP | SHOP Price Prediction) is one of the most polarizing growth stories in software right now. The platform processed $123.84 billion in gross merchandise volume in Q4 2025 alone, grew revenue 30.58%, and commands over 14% of US ecommerce.

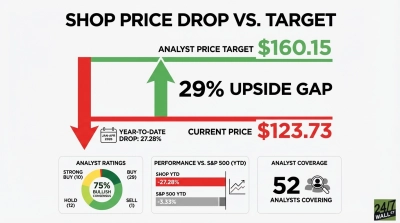

Yet the stock is down 26.25% year-to-date. It trades at $118.71, far below where fundamentals suggest it could go. The question is whether shares can reach $200 by 2028.

Why Shopify Shares Are Stuck Despite 30% Revenue Growth

The headline problem is earnings optics. Net income fell 42.54% year-over-year in Q4 2025 and 39.03% for full-year 2025. The decline stems almost entirely from mark-to-market accounting on equity investments. Operating income rose 35.7% in Q4. Free cash flow grew 17.02% to $715 million.

SHOP is down 2.1% over the past month and 26.25% year-to-date, with a beta of 2.644 that amplifies macro shocks. After touching $159.85 in December, shares fell to a 52-week low of $94 before recovering 15.25% over the past week. This high-beta stock faces a market that has lost appetite for growth.

Wall Street Sees 26% Upside. Our Model Disagrees

The Street is firmly bullish. The consensus target sits at $150.11, with 10 Strong Buys, 29 Buys, 12 Holds, and one Sell. Bullish sentiment is 75%.

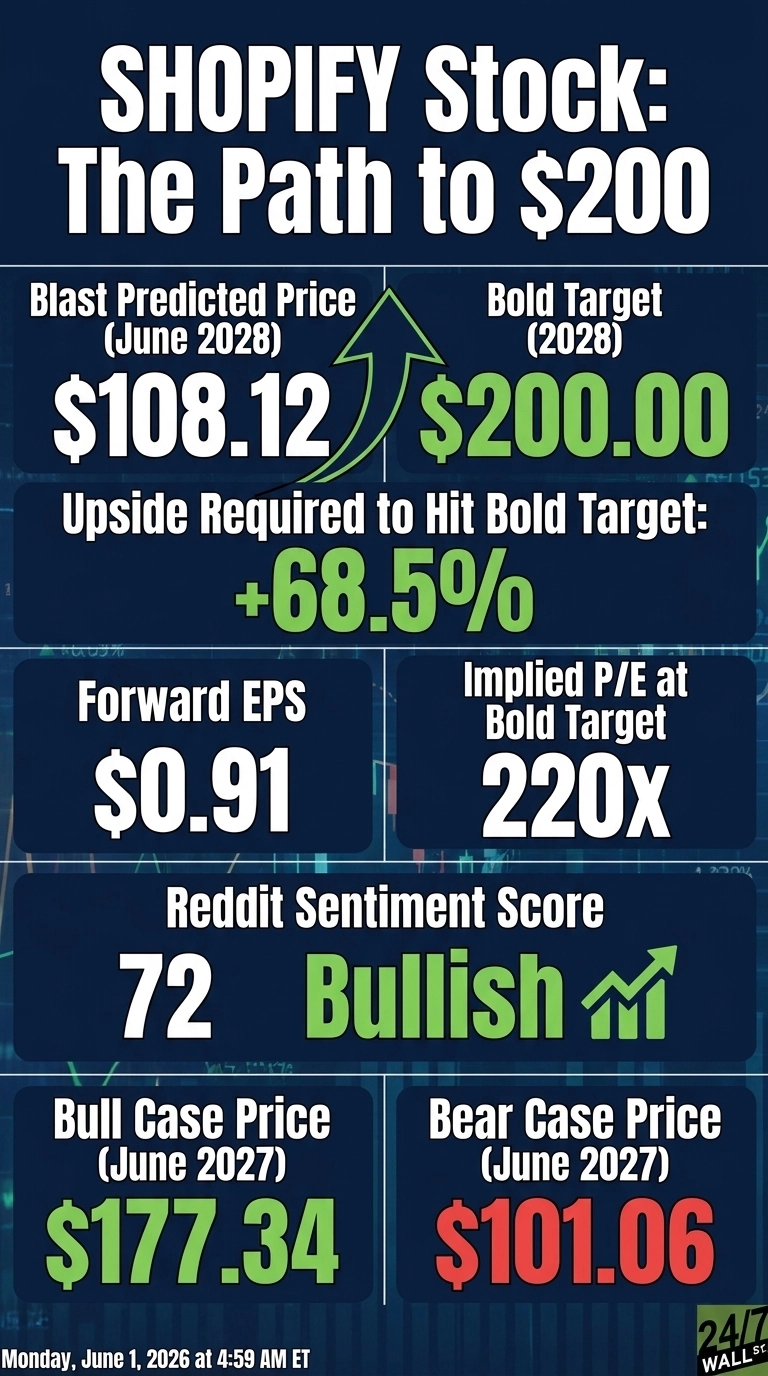

My model is more cautious near-term. The base case lands at $108.12 by mid-2027, implying -8.92% total return with 90% confidence. The optimistic scenario hits $177.34, and the conservative case is $101.06.

Wall Street anchors on real operating leverage but underweights multiple compression risk while EPS optics remain poor. Strip out accounting noise and growth justifies a premium. The Street is right directionally, but the 12-month price target is too aggressive.

The Path to $200 Per Share

Reaching $200 from $118.71 requires a 68.5% gain. That is a stretch.

With forward EPS of $0.91, $200 implies a forward P/E of 220x. Our base case of $108.12 already implies 165x, meaning the bold target requires roughly 55x additional multiple expansion. That math works only if forward EPS estimates climb materially as equity-investment noise normalizes.

The bull setup: Q1 2026 guidance points to low-thirties revenue growth, continuing 11 straight quarters of 25%+ growth. B2B GMV grew 96% in 2025 and international revenue rose 36%. The $2 billion buyback authorized February 17, 2026 will shrink share count. If 2026 EPS roughly doubles as accounting drag clears, the 220x multiple becomes digestible. The primary risk is consumer-spending slowdown cutting GMV growth in half.

Where Shopify Trades Today vs Its Earnings Power

At $118.71, SHOP carries a forward P/E of 130x on $0.91 EPS. Rich, but distorted by mark-to-market losses that shouldn’t recur at this magnitude. Shares sit 18% below the 52-week high of $182.19 and well off the low of $94. The 10-year return is 3,952.92%, a reminder of compounding when a platform takes share. The five-year return is -4.49%. That gap is where the bull case lives.

Is $200 Realistic?

Reaching $200 by 2028 requires a 68.5% gain. Realistic, but a clear stretch.

Three things must go right: EPS optics must normalize as equity-investment volatility settles, revenue growth must hold above 25% through 2027 via international and B2B expansion, and the buyback must absorb meaningful float. A consumer recession would derail the thesis. We’ve outlined the blueprint for how Shopify could reach $200 in 2028.