Few small-cap semiconductor names have ridden the AI optical interconnect wave as wildly as Poet Technologies (NASDAQ:POET). After a triple-digit rally and a sharp June pullback, investors want to know whether the next move is up or down. Here is where our model lands.

The 24/7 Wall St. Price Target for POET

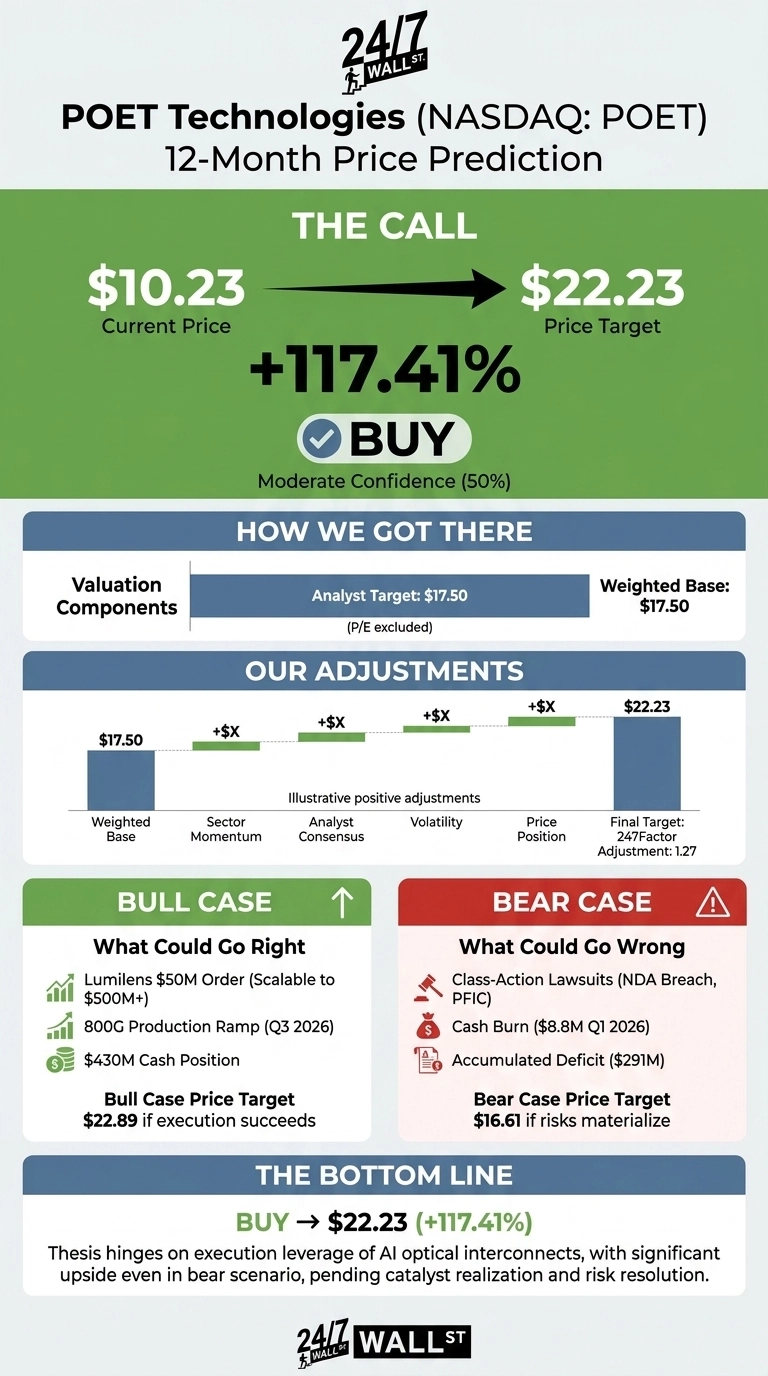

Poet Technologies trades at $10.23 as of June 25, 2026. Our 24/7 Wall St. price target for Poet Technologies is $22.23 over the next 12 months, implying 117.41% upside. Our recommendation is buy, with moderate confidence (0.5 on a 0 to 1 scale). The signal is constructive, but Poet is volatile and news-driven.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $10.23 |

| 24/7 Wall St. Price Target | $22.23 |

| Upside | 117.41% |

| Recommendation | BUY |

| Confidence Level | 50% |

A Wild Year: From $4 to $20 and Back

Poet is up 147.33% over the past year and 68.4% year to date, but the last month has been brutal, with shares down 26.94%. The 52-week range runs from $3.87 to $20.81.

The April 27 cancellation of all Celestial AI purchase orders following an alleged NDA breach triggered class-action filings, with a June 29 lead plaintiff deadline. That overhang was partly offset by the Lumilens partnership and $50 million initial order announced June 12 and a $400 million registered direct offering that closed June 15.

Q1 2026 revenue came in at $503,389, beating estimates by 44.66%, while EPS of -$0.08 missed the -$0.04 estimate on stock-based compensation and warrant accounting.

Why Bulls See a Breakout to $22.89 and Beyond

The bull case rests on Poet’s positioning at the intersection of AI networking and silicon photonics. The Lumilens agreement scales to $500M+ over five years, and Poet has guided to shipping over 30,000 optical engines in 2026, with 800G production ramping in Q3 2026 from Malaysia. Joint development programs with LITEON, Lessengers, and Quantum Computing Inc. target 1.6T and 3.2Tbps modules for frontier AI infrastructure.

CEO Suresh Venkatesan called the Lumilens deal “an important commercial milestone… supporting frontier AI infrastructure.” With roughly $430M in cash post-raise and Jane Street disclosing a 6.8% stake, the balance sheet supports execution. Our bull case scenario points to $22.89 within 12 months.

The Risks Worth Watching

Multiple class-action suits over alleged PFIC misstatements and the Celestial AI NDA breach create legal overhang. Cash burn was $8.8M in Q1 2026 operating outflow, the accumulated deficit sits at $291M, and 2025 raises totaled roughly $375M, diluting holders.

Bulls counter that much of the Q4 2025 $42.67M net loss reflected a $30.69M non-cash derivative warrant liability rather than core operating deterioration, and the planned U.S. redomicile should resolve PFIC risk. Our bear case scenario lands at $16.61, still above today’s price.

Poet Technologies Price Prediction 2026-2030

The 24/7 Wall St. price target for Poet is $22.23, with a buy recommendation at moderate confidence. The tipping factor is execution leverage: even our bear scenario implies 62.4% upside.

Catalysts to watch include the June 26 redomicile vote and the pace of Lumilens order ramp. Risks to the thesis include class-action discovery surfacing material disclosure failures or 800G production slipping past Q3 2026.

Looking ahead, here is where our model projects Poet could trade, assuming AI optical interconnect demand continues compounding and execution holds.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $14.92 |

| 2027 | $22.23 |

| 2028 | $36.00 |

| 2029 | $56.00 |

| 2030 | $72.00 |

These projections assume Poet executes on its 800G and 1.6T roadmap and the broader 800G transceiver market reaches its projected $9.8B by 2032. Significant upside could come from a hyperscaler design win, while downside risk emerges if class-action liability or manufacturing delays in Malaysia disrupt the ramp.

Contact [email protected] for any questions or corrections.