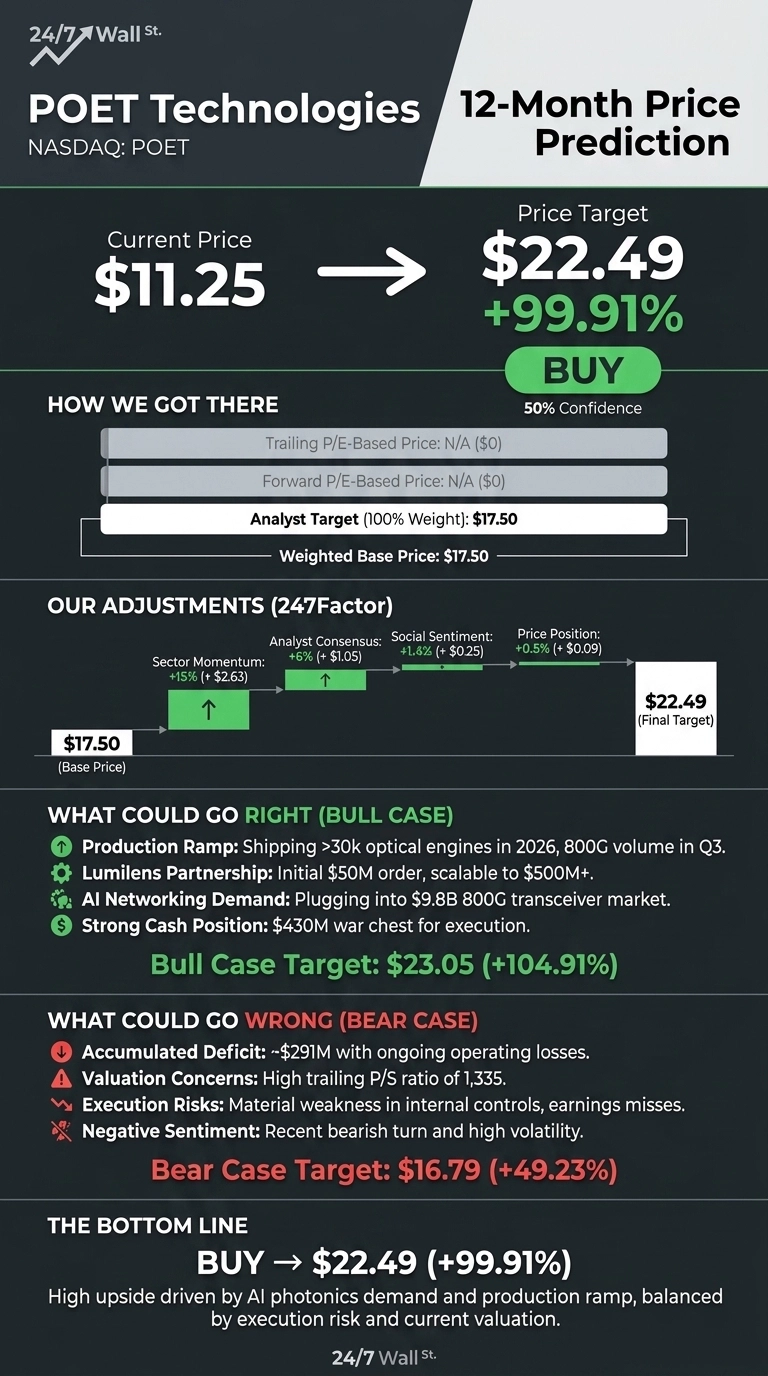

Our POET Technologies (NASDAQ:POET) call is straightforward: the stock could nearly double from here over the next 12 months. With shares trading at $11.25 after a sharp pullback, our 24/7 Wall St. price target for POET is $22.49, implying 99.91% upside.

We rate POET a buy with 50% model confidence, a moderate conviction level that reflects strong commercial catalysts balanced against pre-revenue execution risk.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $11.25 |

| 24/7 Wall St. Price Target | $22.49 |

| Upside | 99.91% |

| Recommendation | BUY |

| Confidence Level | 50% |

A Whiplash Quarter for POET Shareholders

POET has been one of 2026’s wildest rides. Shares are up 77.73% year to date and 170.43% over the past year, but the last week tells a different story. The stock fell 27.3% in seven days and 18.06% over the past month, leaving POET 16% off its 52-week high of $20.81.

The pullback followed a Q1 2026 earnings report that was a tale of two halves. Revenue of $503,389 beat consensus by 44.66% and grew 201.9% year over year, but EPS of -$0.08 missed the -$0.04 estimate. The headline catalyst was a Lumilens joint development agreement carrying an initial $50 million purchase order that POET says could scale beyond $500 million over five years.

The Case for $23 and Beyond

The bull case is a production ramp story. Management guided to ship more than 30,000 optical engines in 2026, with high-volume 800G output starting in Q3 2026 from Malaysia.

POET is plugged directly into the AI networking bottleneck through partnerships with LITEON, Lessengers, NTT Innovative Devices, Sivers Semiconductors, and Quantum Computing Inc. The 800G transceiver market alone is projected to reach $9.8 billion by 2032 at a 22.8% CAGR.

Our bull-case scenario takes the stock to $23.05, a 104.91% return. CEO Suresh Venkatesan framed the moment bluntly: “In Q4 2025, we made a decisive transition from development to execution.” A $430 million cash war chest gives POET the runway to execute without near-term dilution.

The Risks Worth Watching

The bear case is real. POET carries an accumulated deficit of roughly $291 million and a trailing price-to-sales ratio of 1,335, which leaves no margin for execution slip-ups. A prior audit flagged a material weakness in internal controls, and Q4 2025 revenue missed by 51.27%.

Much of the EPS volatility comes from non-cash derivative warrant adjustments tied to Canadian-dollar warrants that should largely disappear after the planned U.S. redomiciliation. Our bear case still lands at $16.79, a 49.23% gain from here, reflecting how far the recent pullback has already discounted bad news.

POET Technologies Price Prediction 2026-2030

Our 24/7 Wall St. price target of $22.49 implies POET roughly doubles over the next year. The recommendation is buy at 50% confidence. The factor tipping the scale is the gap between the recent 27.3% weekly drawdown and the genuinely improving commercial fundamentals.

The thesis strengthens if the 800G ramp begins on schedule in Q3 2026 and Lumilens converts toward its $500 million scaling path. The thesis weakens if Q2 2026 revenue misses meaningfully or U.S. redomiciliation slips into 2027.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $22.49 |

| 2027 | $31.00 |

| 2028 | $42.00 |

| 2029 | $55.00 |

| 2030 | $68.00 |

These projections assume POET continues converting its partnership pipeline into shipped product and that 800G and 1.6T platforms reach meaningful scale. Our five-year base case lands near $74.62, with significant upside or downside dependent on execution at the Malaysia facility and the broader AI capex cycle.

Contact [email protected] for any questions or corrections.