NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) just printed one of the most extraordinary quarters in mega-cap history. Q1 FY27 revenue hit $81.6 billion, up 85.2% year over year, with Data Center alone delivering $75.25 billion and 92% growth. Free cash flow was $48.55 billion in a single quarter.

Yet shares trade at just $205.10, only 10.1% higher year to date. Can NVIDIA stock reach $300 by 2027?

What’s Holding NVIDIA Back Right Now

NVIDIA has digested its own success. Shares are down 2.75% over the past week and 1.2% over the past month, lagging a market that keeps grinding higher. With a beta of 2.2, every macro wobble hits NVDA twice as hard.

China poses another overhang. Management explicitly assumes no Data Center compute revenue from China in the Q2 outlook, and H20 export restrictions cost roughly $8 billion in a single quarter. Add chatter about softening GPU rental prices and high-profile bearish commentary, and you have a stock that has gone sideways while fundamentals exploded. The setup looks tired. The numbers say otherwise.

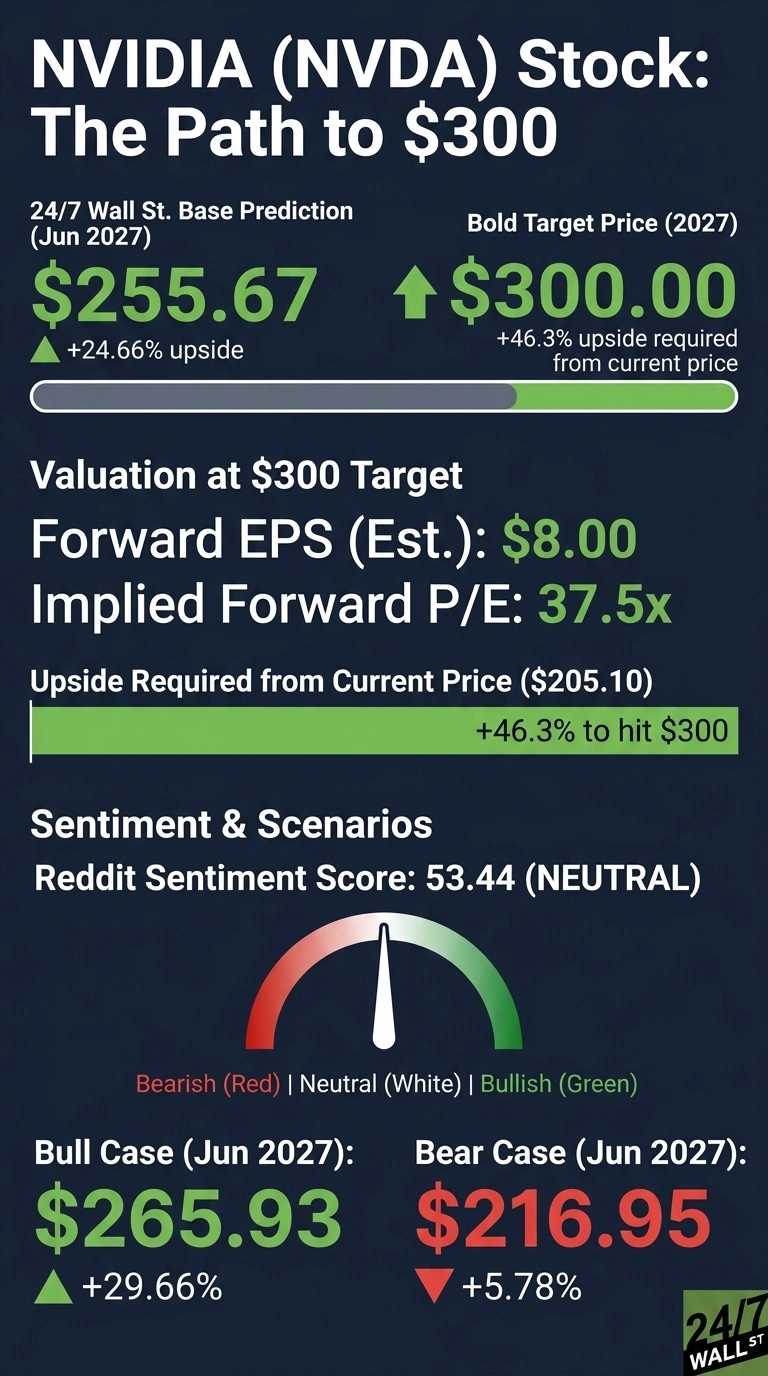

Wall Street Sees 45% Upside. Our Model Says 25%

The consensus is overwhelmingly constructive. The Street’s average target sits at $298.42, supported by 10 strong buys, 48 buys, 2 holds, and 1 sell. Our internal model is more measured, pegging a base case of $255.67 by June 2027, implying 24.66% upside, with a bull case of $265.93 and bear case of $216.95.

Confidence on that base case sits at 90%. With 95% bullish analyst sentiment and quarterly earnings growth of 214.5% year over year, the model’s caution reflects mega-cap dampener cutting contributions in half. Strip that and the Street looks closer to right.

The Path to $300 Per Share

Reaching $300 from today’s price of $205.10 would require a 46.3% gain. With forward EPS of $8, a price of $300 implies a forward P/E of 38x. Our base case of $255.67 already implies 35x, meaning the bold target requires roughly 2.4x additional multiple expansion.

That expansion is defensible. Q2 FY27 revenue is guided to $91 billion, and supply commitments already total $119 billion. Jensen Huang put it bluntly: “The buildout of AI factories, the largest infrastructure expansion in human history, is accelerating at extraordinary speed.”

He also noted that “Blackwell sales are off the charts, and cloud GPUs are sold out.” Layer in the $80 billion buyback authorization and you have meaningful per-share tailwinds. The primary risk is a sudden hyperscaler capex pause that breaks the demand narrative.

Where NVIDIA Trades Today vs Its Earnings Power

At $205.10 on forward EPS of $8, NVDA trades at roughly 26x forward earnings. That is cheap for a business compounding revenue at 85% and earnings at 214% year over year.

Shares sit between a 52-week low of $140.67 and 52-week high of $236.26, so there is room before the stock reclaims its prior peak. The 10-year return is staggering: 17,956%. Sentiment is the real obstacle here.

Is $300 Realistic?

Hitting $300 requires a 46.3% gain and a 38x forward multiple. That is a stretch, though not a long shot.

Three things need to break right: Blackwell and Vera Rubin shipments must sustain triple-digit Data Center growth, gross margins must hold near 75%, and forward EPS estimates need to drift toward $9 by late 2026. A meaningful capex slowdown from hyperscalers would derail it. We’ve outlined the blueprint for how NVIDIA could reach $300 in 2027.

Contact [email protected] for any questions or corrections.