NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) just delivered the kind of quarter that should have sent shares to new highs. Revenue of $81.6 billion grew 85.2% year over year, Data Center clocked $75.2 billion at 92% growth, and Jensen Huang told investors “the buildout of AI factories, the largest infrastructure expansion in human history, is accelerating at extraordinary speed.”

Yet shares sit at $208.19, well off the $236.26 high. So when does NVDA reclaim $250?

What’s Holding NVIDIA Back Right Now

The pullback is narrow. NVDA is down 6.46% over the past week and 3.15% over the past month, even with the stock up 11.76% year to date and 46.17% over the past year. With a beta of 2.2, this stock amplifies every macro tremor.

Three headwinds are damaging the stock. China export restrictions removed Data Center compute from Q2 guidance. Jensen Huang declined an invitation to testify before the U.S. Senate Banking Committee on June 11 regarding AI chip exports, keeping regulatory noise loud.

A broader semiconductor rotation took the iShares Semiconductor ETF down 8.6% in a single session, sweeping NVDA along with high-beta peers despite no company-specific bad news.

Wall Street Sees 43% Upside. Our Model Says 23%

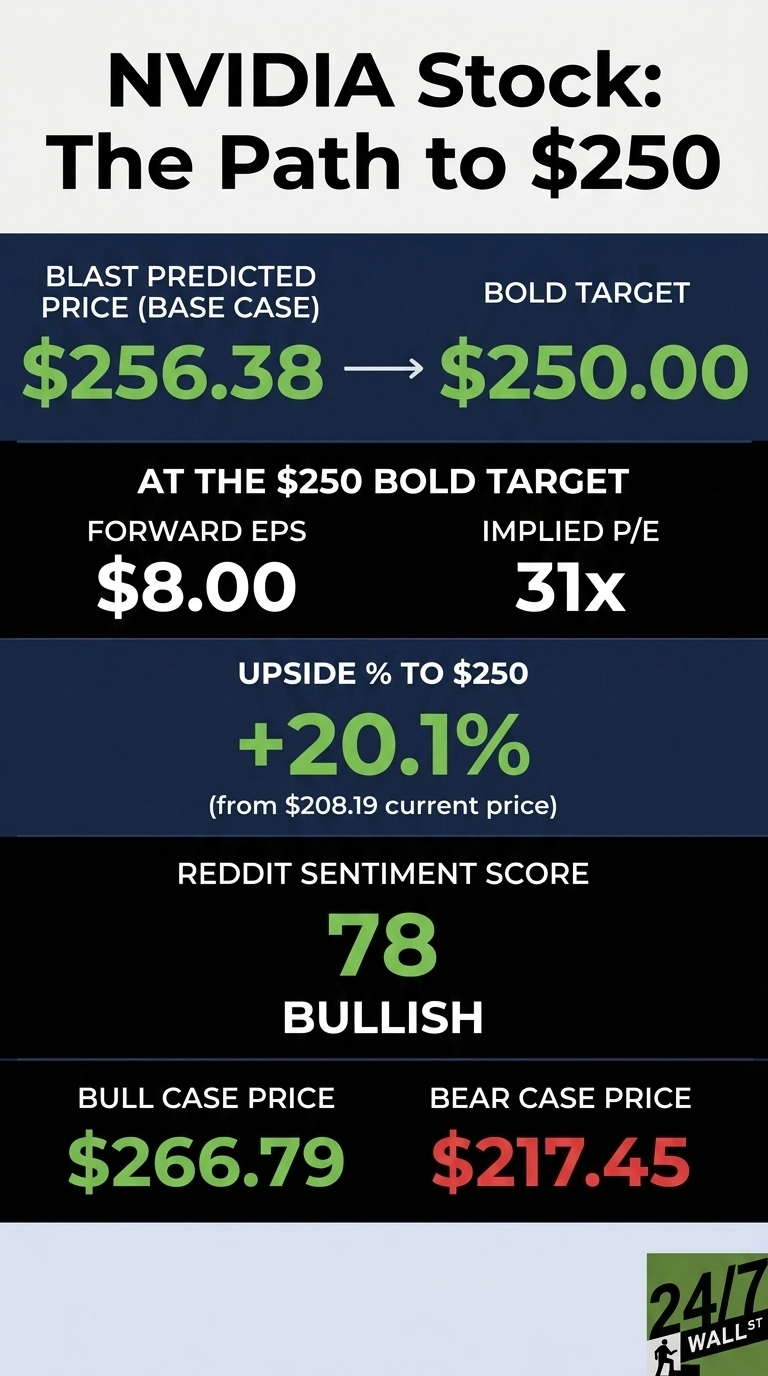

The Street is bullish. 58 buy ratings, 2 holds, and 1 sell back an analyst consensus target of $298.42. 95% bullish sentiment across the analyst pool is one-sided.

My model is more measured. The base case lands at $256.38, a 23.15% gain, with a bull scenario of $266.79 and a bear of $217.45. Confidence sits at 90%. The gap between Wall Street and my work reflects mega-cap dampening: a $5.05 trillion market cap simply cannot compound at startup velocity, even with 214.5% earnings growth.

The Path to $250 Per Share

Reaching $250 from today’s price of $208.19 requires a gain of 20.1%. With forward EPS of $8, $250 implies a forward P/E of 31x. The current forward multiple is 26x, so $250 needs roughly 5x of multiple expansion on top of the EPS the Street expects.

That is achievable. The bull case crosses $250 by February 10, 2027 at $248.25, and the base case sustains the break by April 10, 2027 at $251.74.

The fuel is loaded. The OpenAI partnership commits 10 gigawatts of NVIDIA systems, Meta signed for millions of Blackwell and Rubin GPUs, and total supply commitments reached $119 billion. Huang called Blackwell “the king of inference today” while teasing that Vera Rubin will extend the lead. The single largest risk is a slowdown in hyperscaler capex that strands those supply commitments.

Where NVIDIA Trades Today vs Its Earnings Power

At $208.19, NVDA trades at roughly 26x forward earnings against a trailing P/E of 32. For a business growing earnings 214% year over year with 75% gross margins and $48.6 billion in quarterly free cash flow, that is a cheap multiple.

Shares sit between the $140.67 52-week low and $236.26 high, while the 10-year return of 18,279.91% reminds you what compounding at a platform monopoly looks like.

Can NVIDIA Really Hit $250? My Verdict

$250 requires a 20.1% gain, and my work points to that level being reached between February and April 2027.

Three things need to go right: Blackwell shipments stay on schedule, hyperscaler capex holds through next year, and the China export overhang stops worsening. What derails it is a sudden slowdown in AI infrastructure spending that exposes the $119 billion supply book. We’ve outlined the blueprint for how NVIDIA could reach $250 in 2027.

Contact [email protected] for any questions or corrections.