NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) shares have drawn renewed investor attention following the company’s May report, with the chipmaker positioned at the center of an accelerating AI infrastructure cycle that has lifted both order flow and capital returns.

The bull case is straightforward. NVIDIA sells the picks and shovels for the largest infrastructure buildout in modern computing, and the order book keeps growing. CEO Jensen Huang called it “the buildout of AI factories, the largest infrastructure expansion in human history, accelerating at extraordinary speed”, and the numbers behind that line underscore the scale of demand.

The data behind the latest quarter

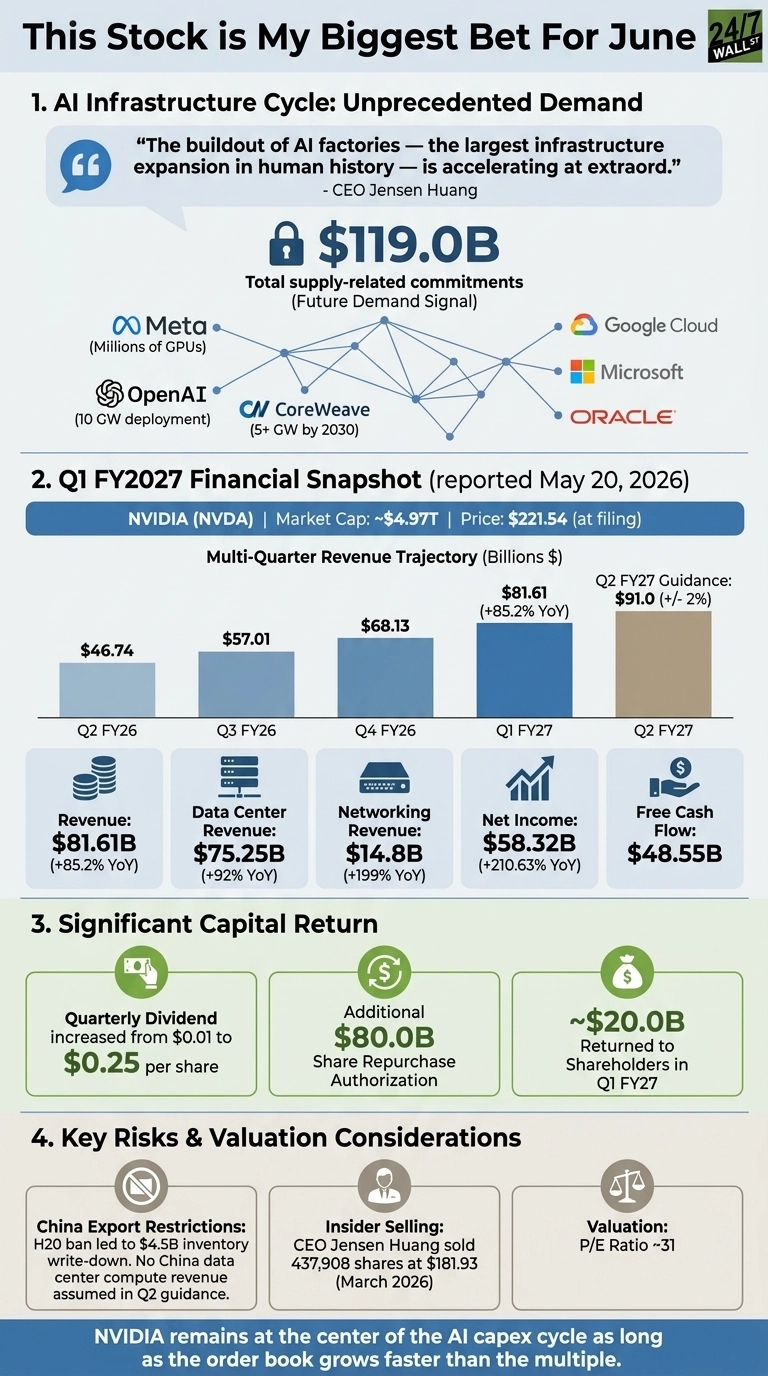

Start with the latest quarter. Q1 FY2027 revenue hit $81.61 billion, up 85.2% YoY, the fourth straight beat. Data Center revenue reached $75.25 billion, up 92% YoY, with networking at $14.8 billion, up 199% YoY. Non-GAAP EPS came in at $1.87. Net income of $58.32 billion grew 210.63% YoY. Free cash flow landed at $48.55 billion in a single three-month window.

The forward picture is where the trajectory compounds. Q2 guidance calls for $91 billion in revenue at a 75% non-GAAP gross margin, and that excludes any China data center compute. Look at the trajectory: $46.74B, $57.01B, $68.13B, and $81.61B over four consecutive quarters. That curve is still accelerating.

Capital return turned serious

Capital return is the second pillar of the story. The board lifted the quarterly dividend from $0.01 to $0.25 per share. It authorized another $80 billion in buybacks on top of $38.5 billion still unused.

Around $20 billion came back to shareholders in Q1 alone, and FY26 returned $41.1 billion. A company funding its own float reduction at this scale, while the business is still compounding, is a rare combination.

A moat measured in dollars booked

Third is the moat, and it shows up in dollars booked. NVIDIA carries $119 billion in total supply-related commitments, which is the most honest demand signal a chip company can publish.

The customer roster reads like a directory of the AI economy: Meta’s multi-year deal for millions of Blackwell and Rubin GPUs, OpenAI’s 10 GW deployment, Anthropic, Google Cloud, Microsoft, Oracle, xAI, and CoreWeave’s commitment for 5+ GW by 2030. Every cloud, every frontier model, runs on this platform.

The honest risks

The risks deserve equal weight. China is the live one. The H20 export ban produced a $4.5 billion inventory write-down, and management assumes no China data center compute revenue in Q2 guidance.

Huang himself said “the $50 billion China market is effectively closed to U.S. industry”. The Q2 guide of $91 billion already strips it out and still grows from $81 billion. Insiders also sold heavily through March, including Huang’s 437,908 shares at $181.93, which reads as executives diversifying after a vertical run.

Valuation deserves a fair hearing too. At a P/E around 31 against earnings growth running well above that, the multiple already prices in some skepticism. Vanguard’s 2026 outlook warns that AI scaler earnings expectations will face renewed scrutiny, a caution worth keeping close.

What the forward setup hinges on

The forward setup comes down to one question: who else gets paid first when a hyperscaler signs a multi-gigawatt AI contract? For now, the answer is unchanged, and as long as the order book grows faster than the multiple, NVIDIA’s position at the center of the AI capex cycle remains intact.

Contact [email protected] for any questions or corrections.