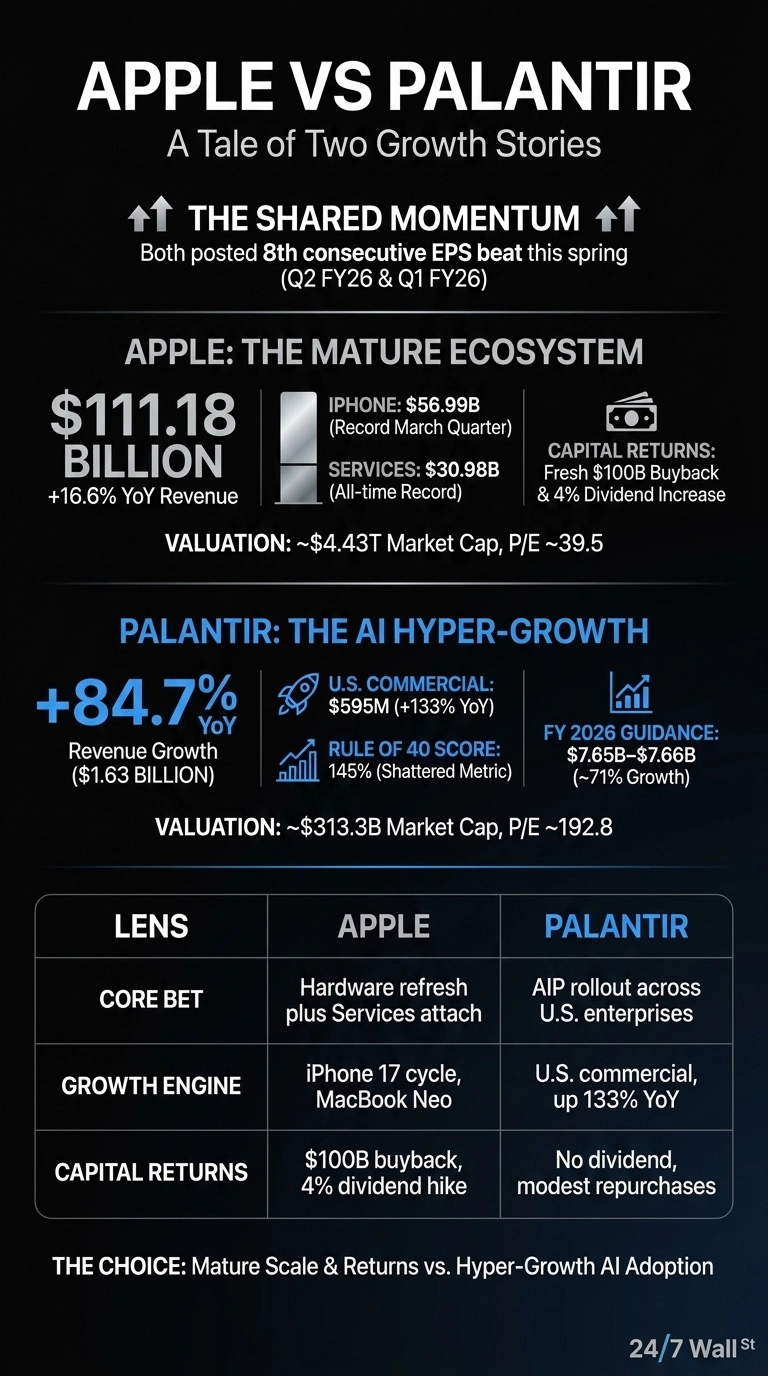

Apple (NASDAQ: AAPL | AAPL Price Prediction) and Palantir (NASDAQ: PLTR) both posted their eighth straight EPS beat this spring, but the businesses behind the numbers could not look more different.

Apple is selling more iPhone 17 units to a 2.5 billion device installed base. Palantir is signing AI deployment contracts at a pace that doubled its U.S. business. Comparing the two right now is really a question about what kind of growth you want to own.

Record iPhone Quarter Meets a Software Land Grab

Apple’s Q2 FY26 revenue hit $111.18 billion, up 16.6% year over year, with iPhone alone delivering $56.99 billion and Services setting an all-time record at $30.98 billion.

Tim Cook credited “extraordinary demand for the iPhone 17 lineup” alongside the launches of the iPhone 17e, M4 iPad Air, and MacBook Neo. Greater China revenue of $20.50 billion finally looks healthy again, which matters because that region has been the swing factor on every recent print.

Palantir’s Q1 FY26 looks like a different category of business entirely. Revenue jumped 84.7% to $1.63 billion, U.S. commercial revenue surged 133% to $595 million, and the company closed 206 deals of $1 million or more.

Alex Karp framed it bluntly: “Palantir’s Rule of 40 score has soared to 145%. We have shattered the metric, a feat matched only by other fellow AI infrastructure companies: NVIDIA, Micron and SK hynix.” The Artificial Intelligence Platform, or AIP, is doing the heavy lifting in commercial accounts.

Cash Machine vs. Compounding Software Bet

| Lens | Apple | Palantir |

| Core Bet | Hardware refresh plus Services attach | AIP rollout across U.S. enterprises |

| Growth Engine | iPhone 17 cycle, MacBook Neo | U.S. commercial, up 133% YoY |

| Capital Returns | $100B buyback, 4% dividend hike | No dividend, modest repurchases |

| Valuation | P/E around 37 | P/E around 152 |

Apple is leaning into what already works: premium hardware, expanding Services, and returning enormous cash to shareholders. Gross margin of 46.9% reflects a business that has earned the right to be boring.

Palantir is doing the opposite, plowing into a customer land grab where U.S. commercial remaining deal value sits at $4.92 billion, up 112%. The stock-based compensation bill of $201.6 million in a single quarter is a real cost of that growth, and one I do not love.

What I Want to See Next Quarter

For Apple, the test is whether Services can keep compounding at a double-digit clip and whether Apple Intelligence finally drives a measurable Services attach lift. The $45.57 billion cash pile gives Cook room to keep buying back stock even if iPhone growth normalizes.

For Palantir, I want to see if the $7.65 billion to $7.66 billion full-year guide proves conservative again. Karp has now raised guidance four straight quarters, and the $1.797 billion to $1.801 billion Q2 setup looks beatable.

Why I Lean Apple for Now, but Hold Palantir Honest

If I had to allocate fresh capital today, I would lean Apple. The valuation is demanding but defensible at 10x sales, the buyback floor is real, and a healthy China quarter removes a major overhang.

Palantir is the more exciting story, and the Rule of 40 score of 145% genuinely belongs in rare company. I just struggle to underwrite 62x sales when one bad guide could compress that multiple in a hurry.

Growth investors with tolerance for volatility may find Palantir’s setup more compelling, while investors prioritizing capital returns and lower multiple risk may find Apple’s profile more comfortable this quarter.

Contact [email protected] for any questions or corrections.