America’s rare earths problem is often framed as a mining problem. Dan Dreyfus, founder of Borneite Capital, argues that’s the wrong way to look at it because the United States has access to plenty of rare earth deposits. The real challenge is processing them. Speaking on a recent All-In Podcast episode, Dreyfus explained that China dominates the specialized refining and separation capabilities needed to turn raw materials into usable products, creating a critical bottleneck that cannot be solved by simply opening new mines.

The Myth of Scarcity

Dreyfus made a counterintuitive point early in the episode: “Rare earths are everywhere, and the technology to extract rare earths is going to allow us to have a huge abundance of them. But the problem is processing them.” Despite the name, “rare earth” deposits are widely distributed, and extraction technology continues to improve.

The real question with rare earth metals is what needs to be done to improve our processes with the ore once it leaves the ground. Federal data underscores the broader industrial challenge: U.S. mining value added contracted to $370.9 billion, just 1.2% of GDP, in the fourth quarter of 2025, with growth at -2.2%. It’s challenging to build a larger processing base when the underlying extractive sector is shrinking.

Processing Know-How Becomes the Real Chokepoint

According to Dreyfus, “The Chinese have all the technological know-how to convert what you take out of the ground and convert it into something that we can use.” Rare earth separation and refining is a complex, capital-intensive, environmentally demanding industrial capability built over decades. He argues that you can permit a mine faster than you can replicate that institutional knowledge.

The Pentagon’s FY 2027 budget request reflects how seriously Washington is taking that gap, with $48.8 billion targeted at critical mineral vulnerabilities and a 5-year “mine-to-magnet” rare earth investment strategy running through Defense Production Act Title III and the National Defense Stockpile. The budget explicitly calls out rare earth element metallization, permanent magnet production, and processing of critical materials waste and recycling streams as priority gaps.

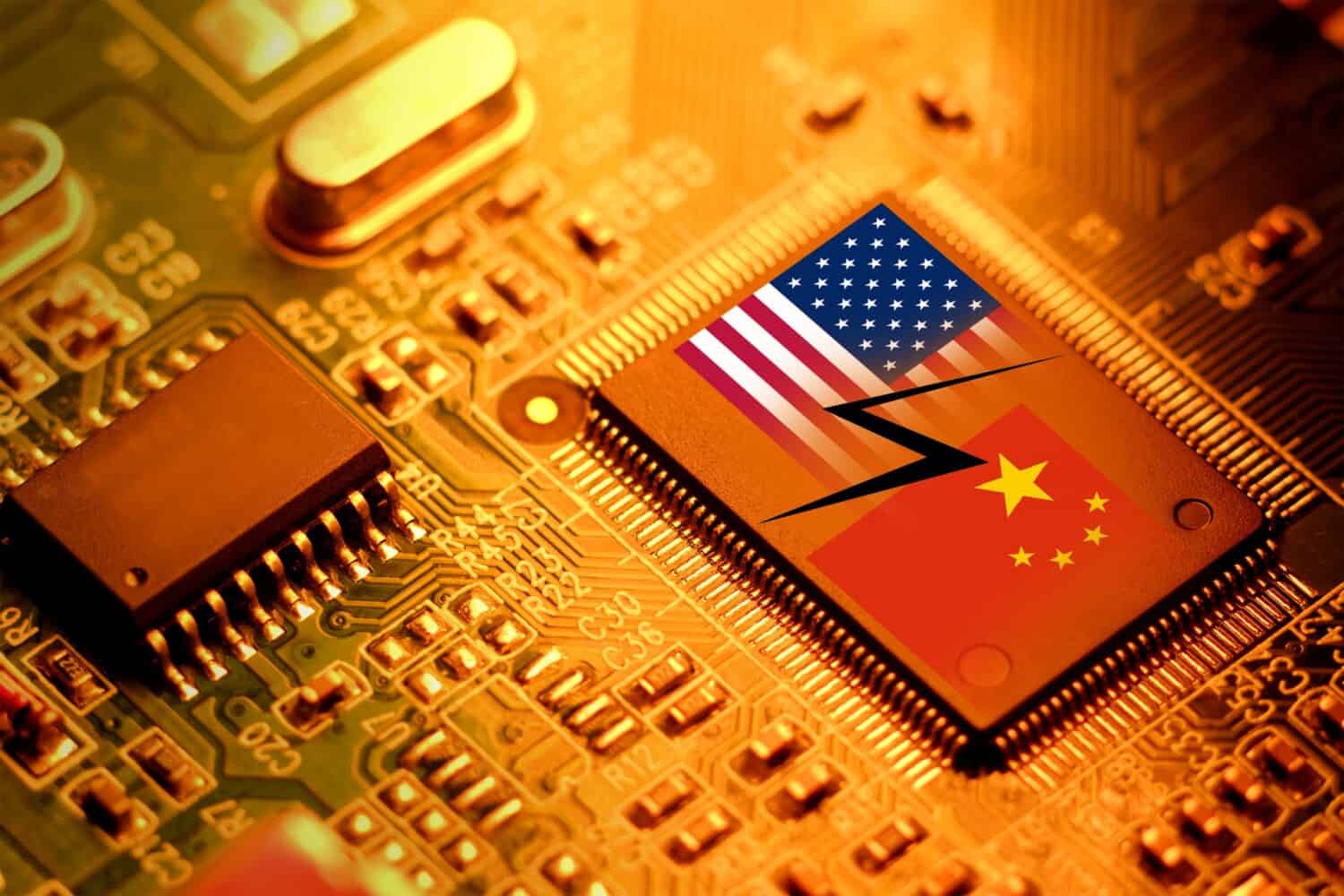

Why Rare Earths Are an “AI Chokepoint”

Rare earths sit upstream of nearly every electrification and AI hardware buildout. Permanent magnets are used in motors, specialty alloys in turbines, components in advanced electronics, and defense systems. Whoever controls the processing layer controls a critical input to the entire Western tech and defense supply chain.

The macro backdrop sharpens the point. The U.S. trade deficit ran at -$55.9 billion in April 2026, with a 12-month average of -$59.2 billion. China remains the largest exporter of knowledge- and technology-intensive manufacturing goods, with $2.2 trillion and a global KTI goods share of 19.1% in 2024. Processing dominance is the moat behind those numbers.

The Reshoring Opportunity and the Labor Dimension

The optimistic counterpoint, framed by the All-In hosts, is that solving this could generate “almost limitless” high-paying craft-labor jobs, with mining and fabrication expanding across North and South America. Dreyfus ties that to a longer arc, saying of deindustrialization: “We tore down all our factories and moved them to China, and who got killed by that? It was the blue-collar craft labor, [which] created all kinds of unintended consequences, fentanyl, you know, wealth gaps.” Deindustrialization led to many negative downstream consequences.

America’s rare-earth problem is primarily a processing and expertise problem, which is both reassuring and sobering. For investors, the theme to track is the long-cycle reshoring of critical-mineral processing and fabrication, which will likely happen in parallel with the grid and copper buildouts Dreyfus also discussed on the podcast. While the United States is investing heavily to rebuild these capabilities, China’s lead in processing has been built over decades and will take years to challenge. That creates both a strategic vulnerability and a significant investment opportunity. Progress is likely, but investors should expect a long and uneven path rather than a quick fix.

Contact [email protected] for any questions or corrections.