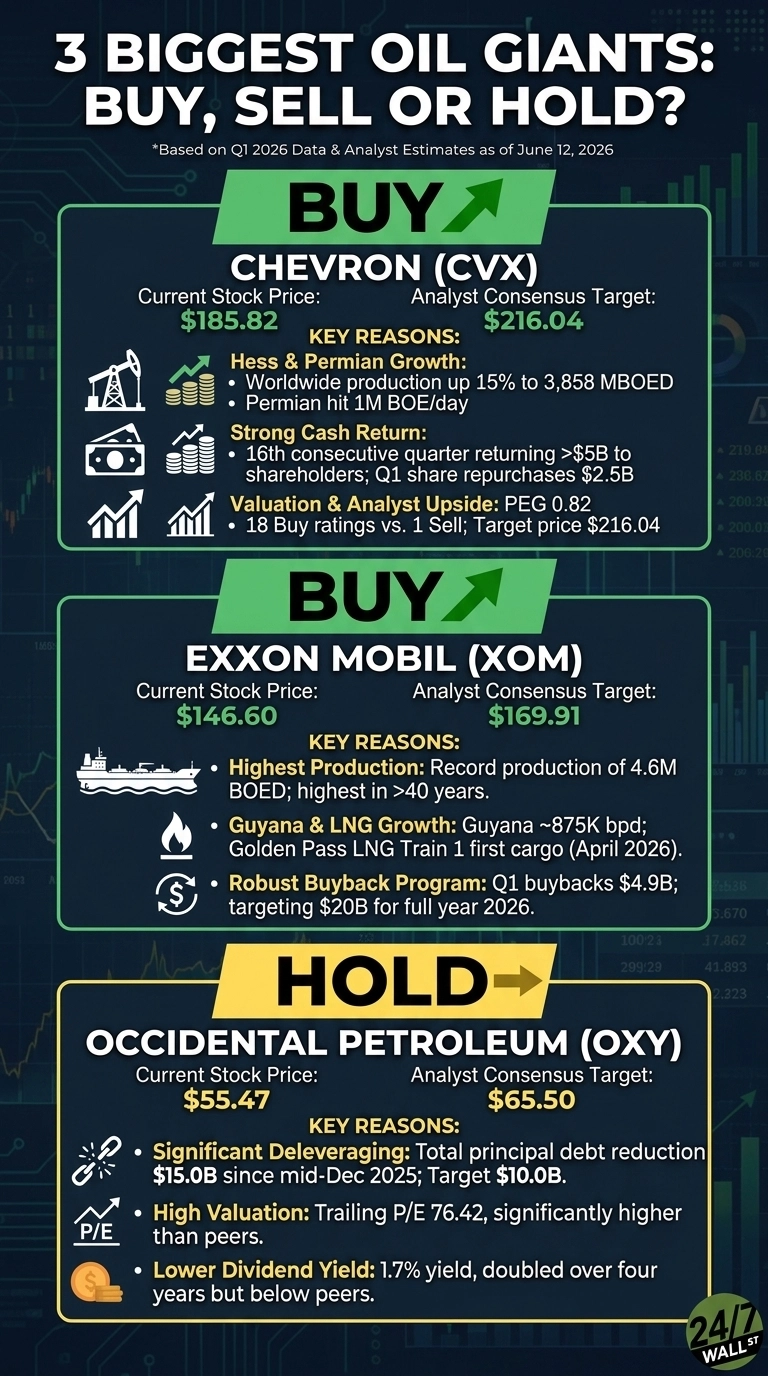

The three biggest U.S. oil majors are sending mixed signals at current prices: Chevron (NYSE:CVX | CVX Price Prediction) at $185.82 looks constructive, Exxon Mobil (NYSE:XOM) at $146.60 looks constructive, and Occidental Petroleum (NYSE:OXY) at $55.47 warrants patience. A WTI spike to $114.58/bbl in April and a still-elevated $95.00/bbl print in early June have reset the math for every barrel produced.

Brent risk premiums tied to the Strait of Hormuz disruption have the EIA modeling Brent near $106/b in May and June, easing to $89/b in 4Q26. That window is when the integrated majors print cash. The question is who turns it into per-share value.

Chevron: Constructive on Hess, Permian, and the Cash Return Engine

Chevron trades at a trailing P/E of 33 but a forward P/E of 14, with a PEG of 0.82 and a dividend yield of 3.65%. Q1 adjusted EPS hit $1.41 vs. $0.97 expected, a sixth straight beat, with worldwide production up 15% to 3,858 MBOED on the Hess deal.

The bear case is real: GAAP net income fell 37% YoY and free cash flow turned negative on timing effects. But 18 Buy ratings against 6 Holds and 1 Sell, and an analyst target of $216.04, frame meaningful upside from here.

At $185.82, the Chevron setup looks constructive. The Hess integration and a Permian asset running at 1M BOE/day give CVX volume leverage into a tight oil tape, while $3 to $4 billion in structural cost savings drop to the bottom line by year-end.

Shares are up 24.23% YTD and 33.72% over one year, comfortably ahead of the S&P 500. A 39-year dividend streak and 16 straight quarters above $5B in capital returns reward patient holders.

Exxon Mobil: Constructive on Scale, Guyana, and the LNG Pivot

Exxon trades at a trailing P/E of 26, forward P/E of 13, and a yield of 2.69%. Q1 adjusted EPS came in at $1.16 vs. $1.01 expected, underlying earnings rose to $8.77 billion, and the company is targeting $20 billion in buybacks for the year.

Advantaged assets are now 59% of production, Guyana sits near 875K bpd, and Golden Pass LNG just shipped its first cargo. Analysts split 11 Buy, 13 Hold, 1 Sell, with a target of $169.91.

At $146.60, the Exxon Mobil setup looks constructive. The bear argument centers on a 40% effective tax rate and chemical weakness, both real.

But shares are up 23.46% YTD and 38.36% over the past year, outpacing the index, on the highest production in over 40 years. Operating leverage into the EIA’s $106 Brent window plus a 43-year dividend track record is the cleanest balance sheet in the sector.

Occidental: Patience Until the Debt Target Lands

OXY is the trickiest call. Shares are up 36.18% YTD, beating both peers and the S&P 500, helped by an 80.33% Q1 EPS beat and a Berkshire-backed OxyChem sale that cut principal debt by $15 billion.

But trailing P/E sits at 76, the dividend yield is just 1.7%, and the analyst split is 8 Buy, 15 Hold, 3 Sell with a target of $65.50.

At $55.47, Occidental warrants patience. The deleveraging story is working, production at 1,426 Mboed is beating guidance, and insiders are net buyers.

The trigger to get more constructive is hitting the $10 billion principal debt target with WTI holding above $80. The trigger to turn cautious is OPEC+ adding barrels into a softening 2027 tape, where EIA sees Brent at $79/b. Until one of those breaks, patience costs less than conviction.