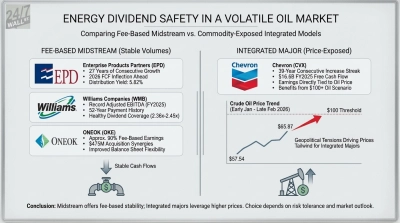

Energy markets have been anything but calm this spring. WTI crude swung from a 12-month low of $55.44 in December 2025 to a peak of $114.58 on April 7, 2026, before settling around $95 per barrel in early June. Henry Hub natural gas briefly spiked to $30.72/MMBtu on January 23, 2026 during a winter weather event before normalizing back into the $2.60 to $3.35 range.

That kind of whipsaw is exactly why fee-based midstream operators look attractive right now. They get paid on volumes, not barrels’ worth. With the EIA forecasting U.S. marketed natural gas production climbing to 121.8 Bcf/d in 2026 and 126.8 Bcf/d in 2027 and LNG exports averaging 17.0 Bcf/d this year, throughput growth is structural.

Three midstream names stand out for investors who want to collect distributions while that volume story plays out.

Energy Transfer

Energy Transfer (NYSE:ET | ET Price Prediction) trades at $19.04 with a market cap around $65.6 billion. The quarterly distribution rose to 33 cents per unit for the May payment, putting the annualized rate at $1.35 and the trailing yield near 7%. Units have returned more than 15% year to date on top of that payout.

The bull case is operational momentum. Q1 2026 adjusted EBITDA rose 20% year over year to $4.94 billion, distributable cash flow climbed to $2.70 billion versus $2.31 billion, and management raised FY2026 adjusted EBITDA guidance to $18.2 billion to $18.6 billion. NGL exports were up 19%, terminal volumes up 19%, and crude transport up 8%. Growth CapEx of $5.5 billion to $5.9 billion funds Mustang Draw I (June 2026 in-service), the Springerville Lateral for AI/data center demand and a Bayou Bridge expansion. The stock’s forward P/E sits at 12.

The caveat: ET is an MLP, so unitholders receive a K-1 tax form rather than a 1099. Interest expense also climbed to $947 million from $809 million a year earlier and Q1 EPS of $0.35 missed the $0.38 consensus.

ONEOK

ONEOK (NYSE:OKE) is the C-corp option in the group, which matters for IRAs and tax-sensitive accounts. Shares trade at $91.11, up nearly 23% year to date, with a yield near 5% on the $1.07 quarterly dividend (annualized $4.28) raised in January. The dividend has stepped up from 99 cents in 2024 to $1.03 in 2025 to $1.07 in 2026.

Roughly 90% of 2025 earnings were fee-based, insulating ONEOK from commodity swings. FY2025 adjusted EBITDA grew 18% to $8.02 billion, and 2026 guidance calls for adjusted EBITDA of $7.9 billion to $8.3 billion and diluted EPS of $5.04 to $5.87. CEO Pierce Norton flagged the company “delivered another year of double-digit earnings growth in 2025.” The Eiger Express Pipeline expansion to 3.7 Bcf/d is fully subscribed, and management has a $2 billion buyback authorization alongside $150 million of incremental EnLink/Medallion synergies expected this year.

The caveat: 2026 guidance assumes WTI in the $55 to $60 range, and management has flagged moderating producer activity. CapEx is also stepping up to $2.7 billion to $3.2 billion.

Enterprise Products Partners

Enterprise Products Partners (NYSE:EPD) is the pedigree pick. The quarterly distribution moved to 55 cents per unit in Q1 2026, the 27th consecutive year of distribution growth, putting the annualized payout at $2.20 and the yield near 6% at the current $37.87 price. Units are up nearly 17% over the past year.

Q1 2026 set 12 new operational records, including NGL fractionation up 16% year over year to 1.9 MMBPD and marine terminal volumes of 2.3 MMBPD. Adjusted EBITDA rose 10% to $2.69 billion, and DCF reached $2.7 billion (including a $600 million Bahia final payment from ExxonMobil). Enterprise has $5.3 billion of major growth projects under construction, just announced two new 300 MMcf/d Permian processing plants for 2027, and has used 31% of its $5.0 billion buyback program. Forward P/E is 13.

The caveat: Q1 revenue fell 7% year over year on weaker NGL prices (57 cents per gallon versus 67 cents), and EPD also issues a K-1.

What to watch next

The setup into the back half of 2026 favors operators that get paid on flow. EIA expects Brent to fade to $89 per barrel in Q4 2026 and $79 in 2027 as Middle East supply normalizes, which would pressure pure commodity names while leaving fee-based midstream cash flows largely intact. The catalysts to track are Mustang Draw I starting up at Energy Transfer, Eiger Express ramp at ONEOK, and the Permian plant build-out at Enterprise. The distributions keep arriving while those projects move from capex to cash flow.

Contact [email protected] for any questions or corrections.