Tesla (NASDAQ: TSLA | TSLA Price Prediction) and BYD (OTC: BYDDF) sit on opposite sides of the global EV map. Tesla’s Q1 2026 report delivered a margin rebound and another lift in AI subscriptions.

BYD, the Shenzhen volume leader, is being repositioned by Beijing’s anti-involution campaign aimed at consolidating EV winners. Both names have slid this year, making the matchup worth a fresh look in June.

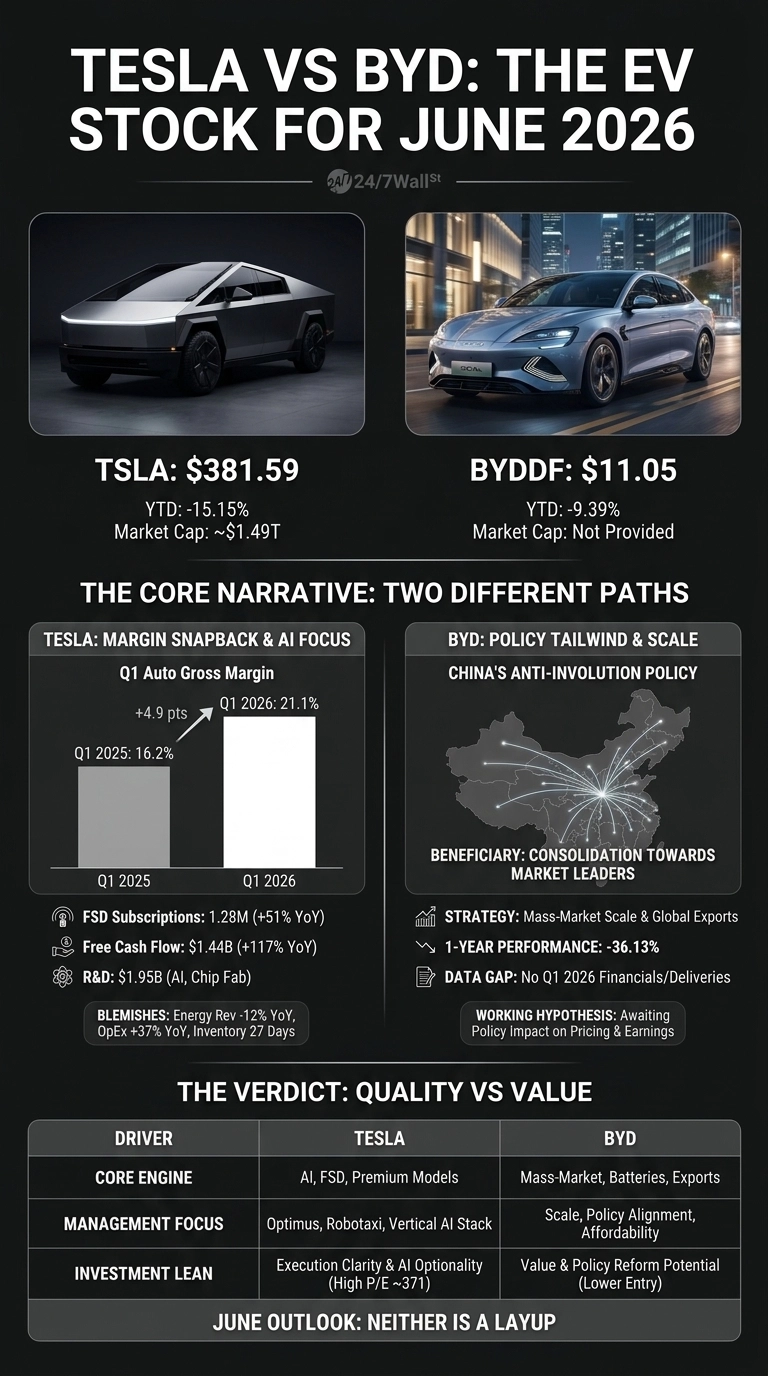

Tesla’s Margin Snapback Meets BYD’s Policy Tailwind

Tesla reported Q1 2026 revenue of $22.387 billion, up 15.78% year over year, with non-GAAP EPS of $0.41 beating consensus by 14.14%. Automotive gross margin expanded to 21.1% from 16.2% a year ago, helped by lower material costs, higher average selling prices, and a one-time warranty and tariff benefit.

Free cash flow jumped 117.47% to $1.444 billion, and cash sits at $44.743 billion. FSD active subscriptions hit 1.28 million, up 51%, turning software into a real recurring line.

The quarter had blemishes. Energy storage revenue fell 12% YoY, operating expenses jumped 37% on AI spending and the CEO equity award, and global inventory crept to 27 days from 22. Deliveries grew just 6%, so unit demand remains middling.

| Business Driver | Tesla | BYD |

| Q1 Auto Gross Margin | 21.1% | Not disclosed in available data |

| Core Growth Engine | FSD, premium models, AI hardware | Mass-market EVs, PHEVs, batteries |

| Management Focus | Optimus, Cybercab, robotaxi rollout | Scale, exports, policy alignment |

BYD enters the second half of 2026 positioned differently. Morningstar’s 2026 outlook names BYD as a likely beneficiary of China’s anti-involution policies, which shift capacity toward the largest and most profitable EV players. BYD shares are down 36.13% over the last 12 months, signaling investors are not yet convinced policy support translates into earnings.

Vertical Stack Versus Vertical Scale

Tesla is funding a full vertical AI stack: FSD v14.3 cut inference latency by 20%, the AI5 chip taped out in April, and a SpaceX-partnered semiconductor fab is going up at Gigafactory Texas.

Cybercab, Tesla Semi, and Megapack 3 are all penciled for volume production this year. R&D climbed to $1.95 billion, a hefty bill for an automaker, modest for an AI platform. BYD owns the cell, pack, powertrain, and assembly line at the lowest cost in the industry.

Tesla chases margin through software. BYD chases share through affordability and a widening export footprint into Europe, LATAM, and Southeast Asia. Beijing’s intervention may let BYD convert that scale into pricing power.

What I Want to See Next

For Tesla, Q2 deliveries are the next swing factor. Polymarket traders assign the highest probability, 35.8%, to a 450,000 to 475,000 vehicle range, with a California robotaxi launch priced at just 4% by June 30. I will watch whether FSD subscriptions keep compounding and whether the energy storage dip was a single-quarter blip.

For BYD, the read is whether policy reform lifts realized prices and whether export volumes keep climbing. Without fresh H1 results, I treat the BYD thesis as a working hypothesis rather than a confirmed setup.

Why I Lean Tesla on Quality, BYD on Value

Tesla offers the cleaner, freshly confirmed quarter. Margin recovery, surging FSD attach, and an AI optionality stack hard to replicate argue for the Austin name. A trailing P/E near 371 on a $1.49 trillion market cap leaves little margin for error, especially with shares down 15.15% YTD and down 9.94% in the past week.

If you believe Chinese policy reform rewards the dominant EV maker, BYD at $11.05 after that drawdown offers more interesting risk-reward. I lean Tesla for execution clarity, though a pullback closer to its 52-week low of $288.77 would offer a more favorable entry profile. In June, neither looks like a layup.

Contact [email protected] for any questions or corrections.