Microsoft (NASDAQ:MSFT | MSFT Price Prediction) has underperformed in 2026, down 18.2% year to date even as the company posted a 123% YoY jump in AI run-rate revenue. That dislocation is the entire reason our model lands where it does.

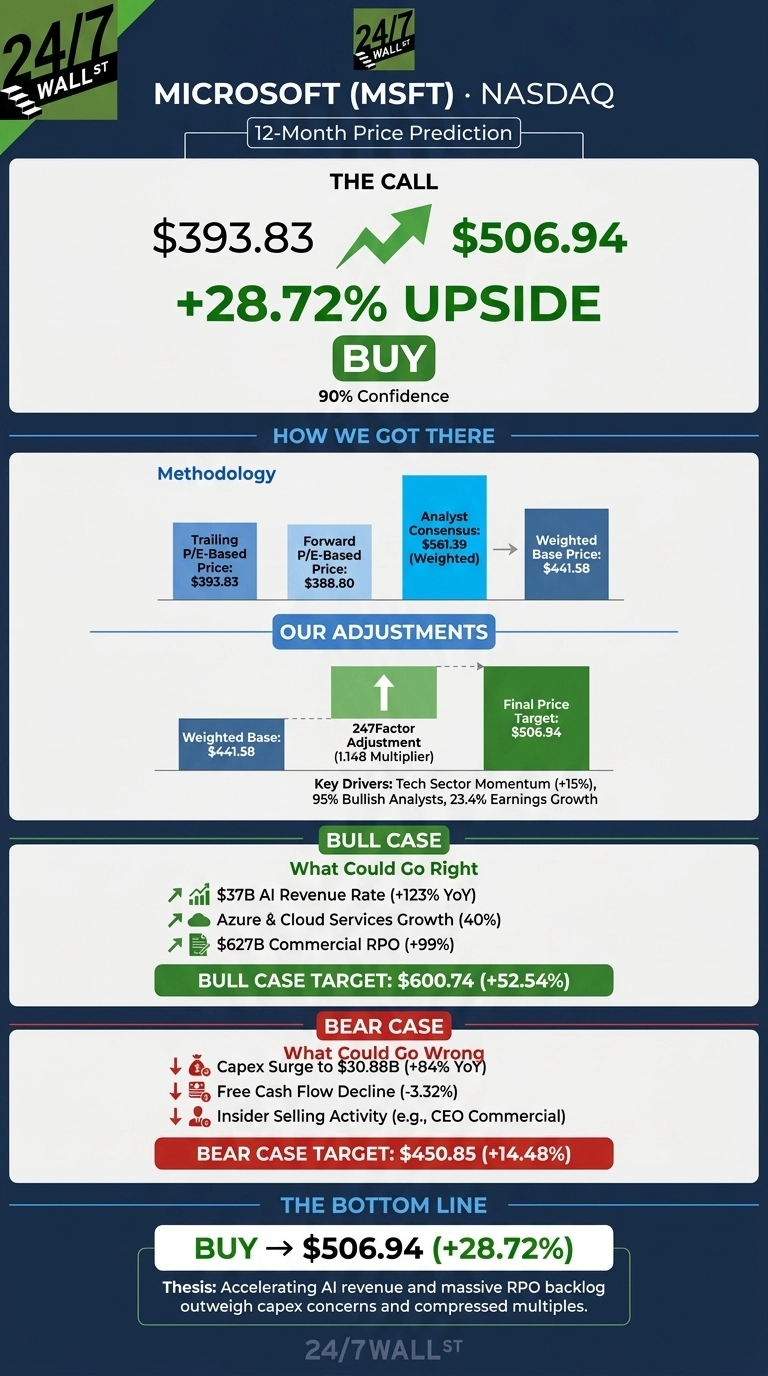

Our 24/7 Wall St. price target for Microsoft is $506.94, implying 28.72% upside from $393.83. Our recommendation is buy with a confidence score of 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $393.83 |

| 24/7 Wall St. Price Target | $506.94 |

| Upside | 28.72% |

| Recommendation | BUY |

| Confidence Level | 90% |

A $124 Slide That Doesn’t Match the Fundamentals

Microsoft entered 2026 near $481 and has slid to $393.83, including a 6.45% drop in the past month. Shares sit roughly 29% below the 52-week high of $551.05, with the 200-day moving average at $453.20.

Yet the April 29 earnings report was excellent. Q3 FY2026 revenue rose 18.3% to $82.89 billion, EPS reached $4.27, beating expectations by 4.9%, Azure grew 40%, and commercial RPO swelled to $627 billion.

CEO Satya Nadella noted the “AI business surpassed an annual revenue run rate of $37 billion, up 123% year-over-year.” The selloff reflects capex anxiety rather than any execution issue.

The Case for $600 and Higher

Our bull-case scenario points to $600.74 within 12 months, a 52.54% return. The $37 billion AI run rate is growing 123% YoY, and commercial RPO of $627 billion provides forward revenue visibility most peers lack.

Microsoft 365 Copilot has 15 million paid seats with daily active users up 10x year over year, and GitHub Copilot subscribers reached 4.7 million, up 75%. Foundry runs at a $2 billion run rate with 31,000 customers.

Wall Street consensus sits at $561.39, with 52 Buy ratings against 3 Holds and zero Sells. If capex worries fade and Azure stays at 40%, $600 is the next stop.

What Could Go Wrong

Our bear scenario lands at $450.85, still positive but muted. The risk is capex. Q3 capex of $30.88 billion was up 84%, FY2025 free cash flow declined 3.32% despite record operating cash flow, and OpenAI investment losses jumped to $3.1 billion in Q1 FY2026.

Insider activity tilted bearish, with Microsoft Commercial CEO Judson Althoff selling 15,500 shares at $460.99 on June 1. Polymarket traders give a combined Anthropic plus OpenAI a 61% probability of exceeding Microsoft’s valuation by year-end.

Bulls counter that capex is contracted: CFO Amy Hood noted GPU capacity for largest customers is “contracted for the entire useful life of the GPU.” The investment is backed by contracted demand.

Microsoft Price Prediction 2026-2030

The 24/7 Wall St. price target is $506.94, our recommendation is buy, and confidence is 90%. Revenue, EPS, AI run rate, and RPO are accelerating while the multiple compressed to a forward P/E near 21.

The bull thesis holds if enterprise AI demand stays on its current trajectory through FY2027. The thesis weakens if Azure growth falls below 30% and capex climbs without commensurate RPO conversion.

Extending the model on current growth and margin trajectories:

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $455 |

| 2027 | $507 |

| 2028 | $595 |

| 2029 | $695 |

| 2030 | $790 |

These projections assume Microsoft continues converting RPO at current rates and Azure growth normalizes to the high 20s by 2028. Upside could come from agentic AI monetization across Microsoft 365; downside risk centers on capex returns failing to materialize.

Contact [email protected] for any questions or corrections.