Microsoft (NASDAQ:MSFT | MSFT Price Prediction) has been one of the most divisive mega-caps of 2026. Shares are down sharply year to date, yet the company just posted its fourth straight earnings beat and an AI business growing faster than almost anything in the S&P 500. The question: can Microsoft push through $600 before year-end?

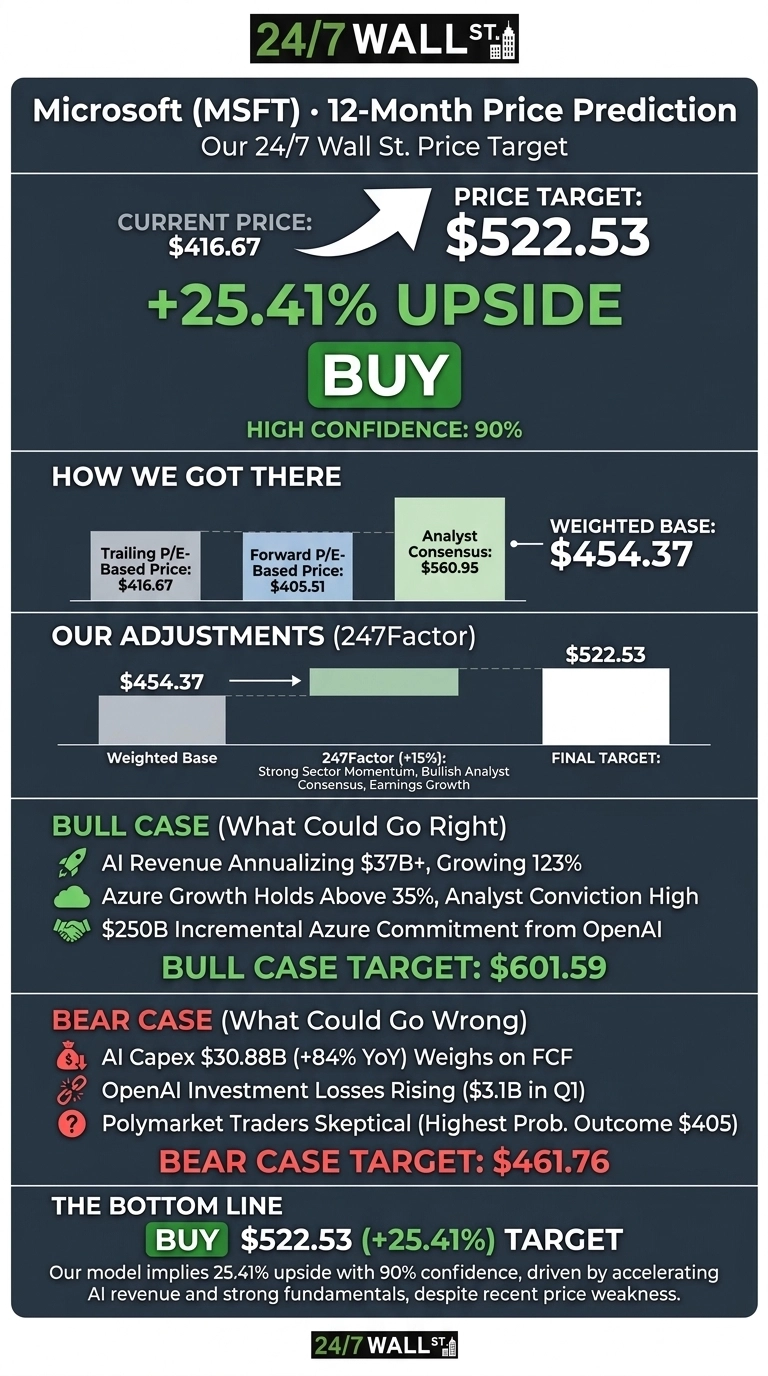

Our 24/7 Wall St. price target for Microsoft is $522.53 over the next 12 months, implying 25.41% upside from the current $416.67. Our recommendation is buy, with a confidence level of 90%. A run to $600 within 12 months sits in our bull case at $601.59, though our base case sits lower.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $416.67 |

| 24/7 Wall St. Price Target | $522.53 |

| Upside | 25.41% |

| Recommendation | BUY |

| Confidence | 90% |

A Painful Year-to-Date for a Best-in-Class Business

Microsoft is down 13.46% year to date and 7.46% over the past week, pulling back from a 52-week high of $551.05 to a February low of $396.86. In Q3 FY2026, reported on April 29, 2026, Microsoft delivered EPS of $4.27 on revenue of $82.89 billion, up 18.3% year over year, beating expectations on both lines.

Azure grew 40%, and CEO Satya Nadella told investors, “Our AI business surpassed an annual revenue run rate of $37 billion, up 123% year-over-year.” Commercial remaining performance obligations reached $627 billion, providing years of forward visibility. The disconnect between fundamentals and price is the entire setup for our thesis.

The Case for $600 and Beyond

Our bull case takes Microsoft to $601.59 within 12 months, a 44.38% total return. AI revenue is annualizing at $37 billion and growing 123%. Goldman Sachs projects $5.3 trillion in Big Tech AI infrastructure spending from 2025 to 2030, with Microsoft positioned as a primary beneficiary. The restructured OpenAI partnership locked in a $250 billion incremental Azure commitment and extended IP rights through 2032.

Analyst conviction is unusually one-sided. Of 55 rated analysts, 52 carry Buy or Strong Buy ratings, with zero Sells and a consensus target of $560.95. If Azure growth holds above 35% and operating leverage continues to widen, the multiple re-rates and $600 comes into play.

What Could Go Wrong

The bear case rests on AI return-on-investment skepticism. Capital expenditures hit $30.88 billion in Q3 FY2026 alone, up 84% year over year, and OpenAI investment losses ran $3.1 billion in Q1. Polymarket traders see almost no probability mass above $500 for the June 2026 window, with $405 as the highest-probability outcome at 77.5%. Our bear case lands at $461.76, still modestly positive.

Bulls argue heavy capex reflects multi-year demand backed by a $627 billion backlog. Net income still grew 23% last quarter despite the buildout.

Microsoft Price Prediction 2026-2030

The 24/7 Wall St. price target of $522.53 reflects a high-conviction buy with 90% confidence. The factor tipping the scale is accelerating AI revenue combined with a beaten-down share price trading well below its 200-day average of $457.29.

The bull thesis strengthens if Azure growth holds at or above 35% in the next print, and weakens if capex outpaces revenue growth and free cash flow compresses further.

Here is where our model projects Microsoft could trade in the coming years, assuming current AI monetization and Azure trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $522.53 |

| 2027 | $595 |

| 2028 | $680 |

| 2029 | $745 |

| 2030 | $810.59 |

These projections assume Microsoft continues executing on its AI strategy and Azure compounds at a high-teens to low-twenties rate. Meaningful upside or downside could come from AGI-related breakthroughs, OpenAI’s evolving relationship with Azure, or a broader unwind of AI capex enthusiasm.

Contact [email protected] for any questions or corrections.