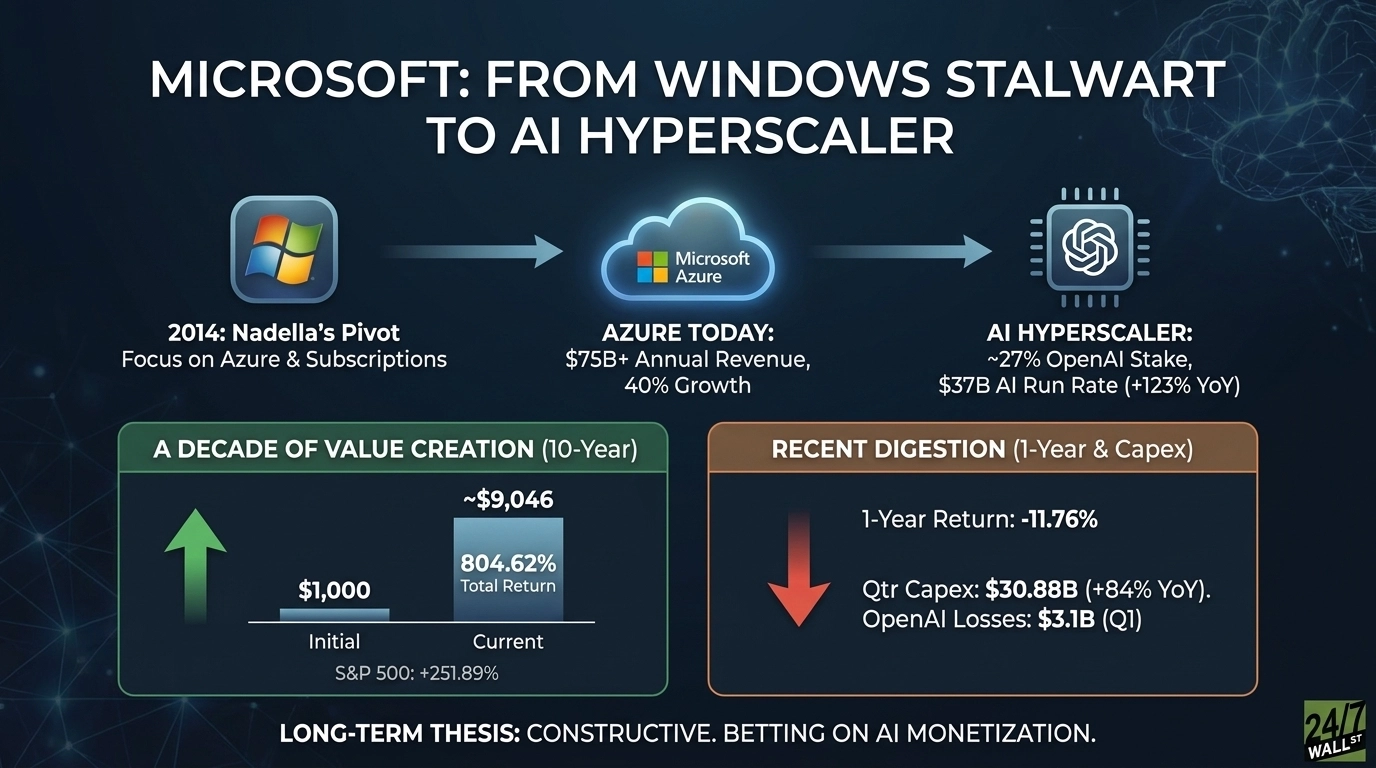

A decade ago, Microsoft (NASDAQ:MSFT | MSFT Price Prediction) was still living down its “lost decade.” Satya Nadella had taken the CEO seat in 2014 and was quietly rewiring the company around Azure, subscriptions, and partnerships the old Microsoft would have shunned. Ten years later, Azure is the second-largest cloud platform, Microsoft Cloud cleared $54.5 billion in a single quarter, and a roughly 27% stake in OpenAI put it at the center of the generative AI boom.

The Copilot rollout embedded AI across Office, GitHub, and Dynamics. The restructured OpenAI deal extended Microsoft’s IP rights through 2032 and locked in $250 billion of incremental Azure commitments. AI revenue is now running at a $37 billion annualized run rate, up 123% year over year.

Your $1,000 Turned Into Roughly $9,000

1-Year Return

- Initial Investment: $1,000

- Current Value: ~$882

- Total Return: -11.76%

- S&P 500 (same period): ~$1,234 (+23.38%)

5-Year Return

- Initial Investment: $1,000

- Current Value: ~$1,692

- Total Return: 69.2%

- Annualized Return: ~11.1%

- S&P 500 (same period): ~$1,753 (+75.32%)

10-Year Return

- Initial Investment: $1,000

- Current Value: ~$9,046

- Total Return: 804.62%

- Annualized Return: ~24.6%

- S&P 500 (same period): ~$3,519 (+251.89%)

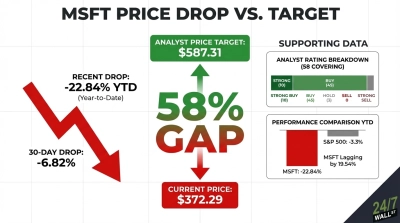

The 10-year picture is the headline. Microsoft tripled the S&P 500’s return, driven by Azure scaling past $75 billion in annual revenue and operating margins holding above 46%. Dividends helped, with the quarterly payout growing from $0.36 in 2016 to $0.91 today.

The recent year tells a different story. Shares are down 14.48% year to date and gave back 10.59% just last week, as investors started asking hard questions about the $30.88 billion quarterly capex bill and OpenAI losses.

The Bull And Bear Case From Here

The bull case rests on whether the $627 billion commercial RPO backlog converts into the revenue the bulls expect. That number nearly doubled year over year, Azure is still growing 40%, and a forward P/E of 21x on a business compounding earnings in the 20s is not demanding.

The bear case is that the capex cycle outruns AI monetization. CapEx is up 84% year over year, OpenAI losses hit $3.1 billion in Q1, and the exclusivity moat on Azure has loosened.

My read: constructive. The 10-year track record was built on Nadella making the right bet before consensus caught up, and the current drawdown looks more like indigestion than a broken thesis. The setup looks more like a digestion phase than a structural break.

Contact [email protected] for any questions or corrections.