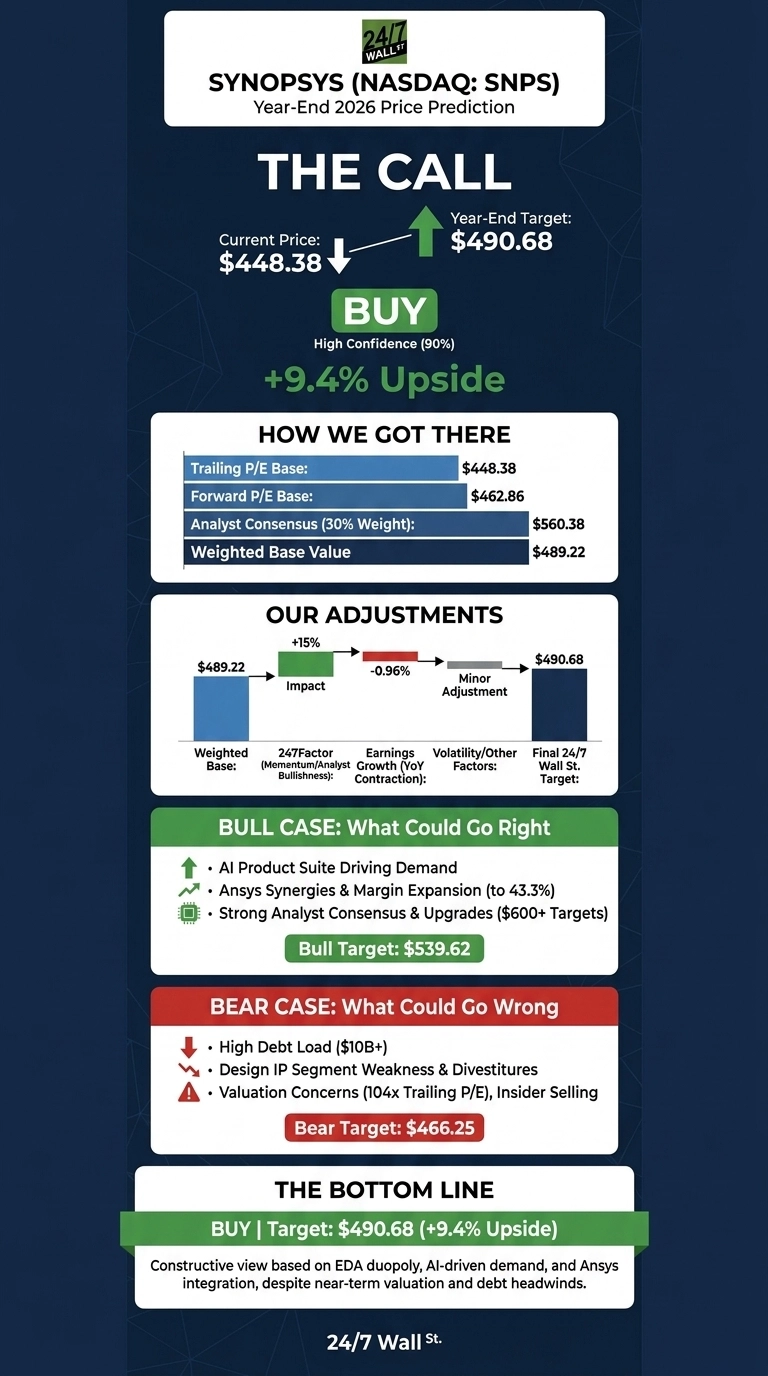

Synopsys (NASDAQ:SNPS | SNPS Price Prediction) has spent 2026 stuck in the penalty box. The stock trades at $448.38, down 10.76% over the past month and 4.54% year to date, even as the chip design software duopoly remains the most strategically vital toll booth in semiconductors.

Our 24/7 Wall St. price target for Synopsys is $490.68 by year-end 2026, implying mid-single-digit upside from here. Our research view leans constructive with high conviction.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $448.38 |

| 24/7 Wall St. Price Target (Year-End 2026) | $490.68 |

| Implied Upside | ~9.4% |

| Research View | Constructive |

| Confidence Level | 90% |

Why the Stock Has Drifted Lower

The narrative on Synopsys is mixed, and the price action reflects it. Shares sit 31.20% below the 52-week high of $651.73 set after the Ansys close, with a 52-week low of $376.18.

The Q2 FY2026 report on May 27, 2026 was strong: revenue of $2.276 billion grew 42% YoY, non-GAAP EPS of $3.35 beat consensus by 5.96%, and management raised full-year guidance to a midpoint of $9.665 billion in revenue and $14.76 in non-GAAP EPS.

The pressure is coming from a $10 billion long-term debt load, $403.6 million in quarterly amortization compressing GAAP profit, and a CFO $1.53 million Rule 10b5-1 sale on June 12, 2026.

The Case for $540 and Higher

The bull case rests on Synopsys’s structural moat. CEO Sassine Ghazi said at the Mizuho Technology Conference that “no modern chips can be designed without the company’s technology.” Stifel reiterated Buy with a $600 price target on June 11, and Citi raised its target to $610 on the same day, citing the Q2 beat and IP recovery.

Analyst consensus sits at $560.38 with 17 Buy ratings, 7 Holds, and just 1 Strong Sell. Our bull scenario points to a year-end $539.62, driven by the new AI Product Suite, the Murata Ansys partnership, and Design Automation margins expanding to 43.3%.

What Could Push Shares to $466

The bear case centers on integration risk and Design IP. The segment generated $454.2 million in Q2, and the Processor IP Solutions divestiture removes roughly $40M from FY26 guidance.

Bulls would counter that the $234.2 million in H1 restructuring charges are non-recurring and that reallocating IP resources to AI-driven markets should drive sequential recovery in H2. Still, a trailing P/E of 104, shareholder lawsuits tied to Design IP disclosures, and a Morgan Stanley flag on growth deceleration justify caution. Our bear scenario sees year-end $466.25.

Synopsys Price Prediction 2026-2030

The 24/7 Wall St. price target is $490.68 by year-end 2026, with a 90% confidence read on a constructive view. The factor that tips the scale is the EDA duopoly with Cadence, which gives Synopsys pricing power inside every AI chip program on the planet.

The setup looks constructive here as long as Design Automation margins keep expanding and the September 30 Investor Day delivers credible long-term targets. The thesis weakens if Design IP fails to recover in H2 or if the Entity List headwind broadens.

Looking further ahead, here is where our model projects Synopsys could trade, assuming Ansys synergies compound and AI-driven EDA demand holds.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $490.68 |

| 2027 | $559.18 |

| 2028 | $645 |

| 2029 | $745 |

| 2030 | $860 |

These projections assume Synopsys keeps executing on the silicon-to-systems platform. Significant upside or downside could come from AI capex normalization or further export control escalation.

Contact [email protected] for any questions or corrections.