Synopsys (NASDAQ:SNPS | SNPS Price Prediction) is one of the most strategically positioned software franchises in the AI-era semiconductor stack, and the recent pullback has reset the setup for investors evaluating the name.

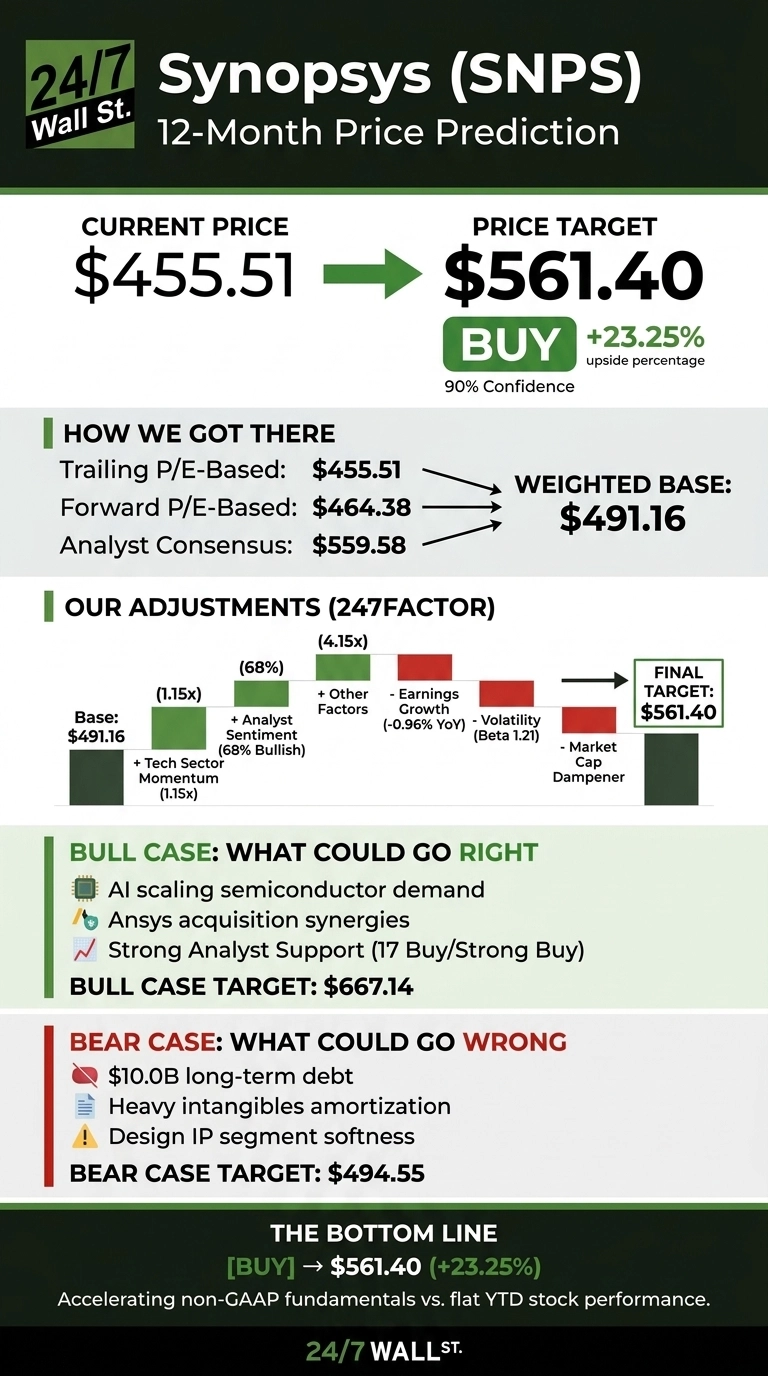

The 24/7 Wall St. price target for Synopsys is $561.40, implying 23.25% upside from $455.51. Our model classifies SNPS as a high-conviction setup, with 90% confidence in the target.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $455.51 |

| 24/7 Wall St. Price Target | $561.40 |

| Upside | 23.25% |

| Recommendation | BUY |

| Confidence | 90% |

A Strong Quarter Met With a Sleepy Stock

SNPS is down 7.77% over the past month and 3.03% year to date, trading 14% below its 52-week high of $651.73 and well off the low of $376.18.

The cooldown followed a strong Q2 FY26 print on May 27, 2026: revenue of $2.276B, up 42% YoY, with non-GAAP EPS of $3.35 beating estimates by 5.96%. Design Automation operating margin expanded to 43.3% from 40.9% a year earlier. Management raised FY26 guidance to $9.625B to $9.705B in revenue and $14.72 to $14.80 in non-GAAP EPS.

The Case for $667 and Beyond

Bulls have a clean thesis. CEO Sassine Ghazi said on the Q2 call that “AI is scaling semiconductor demand, architectural diversity and complexity of chips and the systems they power, driving demand across our portfolio.”

Synopsys sits at the choke point for every advanced-node design, and the $35 billion Ansys acquisition that closed July 17, 2025 extends that moat into multi-physics simulation.

Q1 FY26 revenue grew 65.4% YoY, and the backlog stood at $11.4B exiting FY25. Of 25 analysts, 17 rate the stock Buy or Strong Buy against just one Strong Sell. Our bull case scenario puts SNPS at $667.14 within 12 months, a 46.46% return, if Ansys synergies accelerate and the September 30 Investor Day reveals raised long-term targets.

The Risks Worth Watching

The bear case starts with the balance sheet. SNPS carries roughly $10B in long-term debt and $403.6M in quarterly intangibles amortization, which crushed GAAP net income to $17.1M in Q2.

Bulls will counter that this is purely a non-cash artifact of purchase accounting and that non-GAAP EPS and free cash flow of $2B tell the real story. Design IP remains soft, with management divesting Processor IP Solutions, and export controls into China remain an overhang.

Year-over-year quarterly earnings growth of -0.96% trimmed our factor by 0.03. The bear scenario lands the stock at $494.55 over the next year, still 8.57% above today.

Synopsys Price Prediction 2026-2030

The 24/7 Wall St. price target of $561.40 reflects a high-confidence buy. The tipping factor is the disconnect between accelerating non-GAAP fundamentals and a stock that has gone nowhere YTD.

The bull case rests on AI-driven design complexity remaining a multi-year tailwind and Ansys synergies landing as guided. The bear case strengthens if the trailing P/E of 104 matters more than the forward P/E of 31, or if China export controls tighten further.

Looking further out, here is where our model projects SNPS could trade, assuming current growth and margin trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $561.40 |

| 2027 | $666.63 |

| 2028 | $710.01 |

| 2029 | $805.26 |

| 2030 | $849.44 |

These projections assume Synopsys keeps executing on Ansys integration and AI design demand stays robust. Significant upside or downside could come from China export policy, EDA pricing power, or the pace of advanced-node design starts.

Contact [email protected] for any questions or corrections.