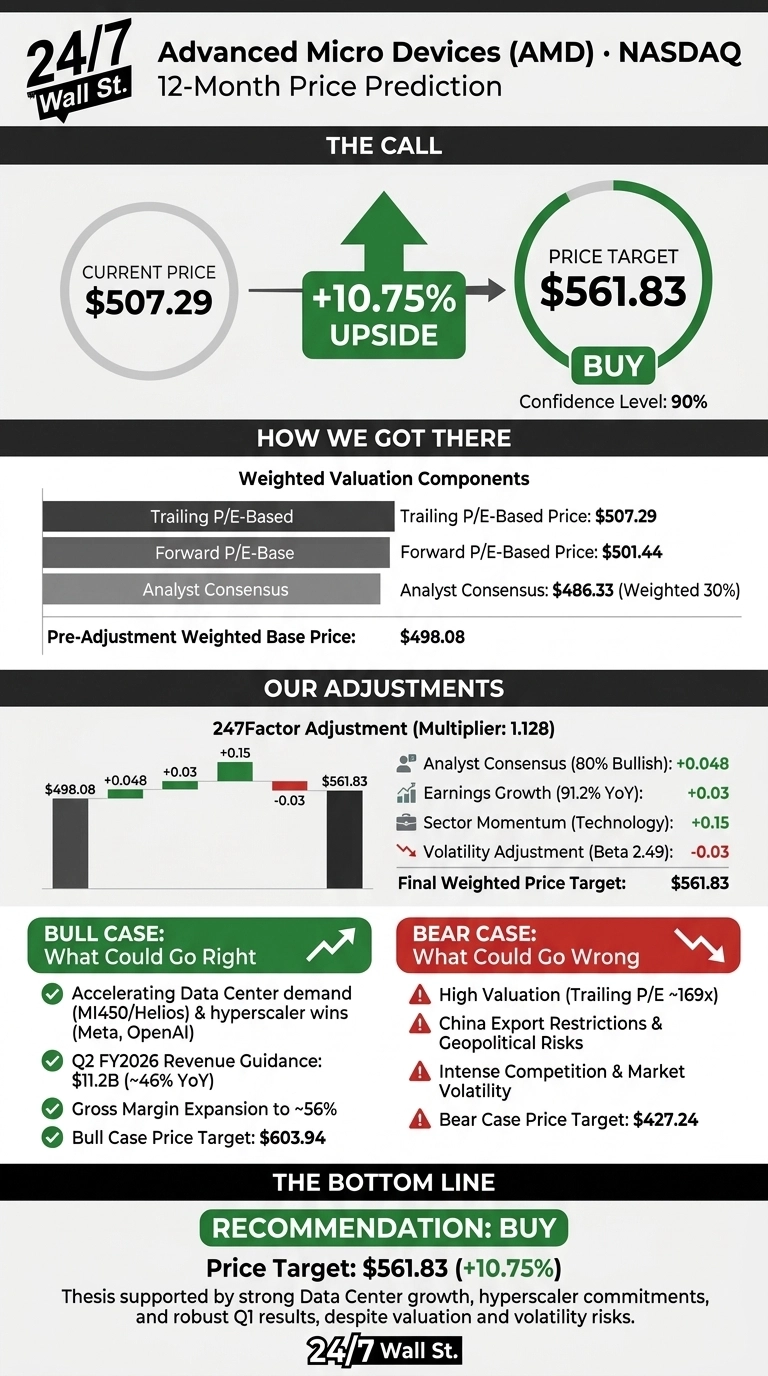

The 24/7 Wall St. price target for Advanced Micro Devices (NASDAQ:AMD | AMD Price Prediction) is $561.83 over the next 12 months. With AMD trading at $507.29 after a brutal 7.3% single-day reset on June 16, our proprietary model still points to roughly 10.75% of upside from here.

Our recommendation is buy, with a confidence level of 90%. The rally has further to run, though the easiest gains are behind us.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $507.29 |

| 24/7 Wall St. Price Target | $561.83 |

| Upside | 10.75% |

| Recommendation | BUY |

| Confidence Level | 90% |

From $214 to $507: The Rally That Refused to Quit

AMD has gained 136.87% year to date and 301.37% over the past 12 months, climbing from a 52-week low of $125.77 to within striking distance of the $558.37 high.

The catalyst was Q1 FY2026, reported May 5: revenue of $10.25 billion grew 37.85% YoY, non-GAAP EPS of $1.37 beat by 5.88%, and the Data Center segment surged 57% to $5.78 billion. Free cash flow expanded 252.96% YoY. Since the filing, AMD has rallied 47.8% against just 2.2% for the S&P 500.

The Case for $600+

Bulls have a credible path to our $603.94 bull-case target. Lisa Su told investors that “customer engagement around MI450 Series and Helios is strengthening, with leading customer forecasts exceeding our initial expectations.” Behind that statement sit the OpenAI 6-gigawatt deployment, Meta’s 6-gigawatt Instinct commitment, and Oracle’s 50,000-GPU Helios supercluster launching in Q3 2026.

Q2 guidance of $11.2 billion implies 46% YoY growth, with non-GAAP gross margin expanding to 56%. AMD’s recent MLPerf Training 6.0 results showed a 3.5X generational improvement on Llama 2-70B, narrowing the perceived gap with NVIDIA‘s (NASDAQ:NVDA) B200. Of 51 covering analysts, 41 rate AMD a buy with zero sell calls.

What Could Go Wrong

The bear case targets $427.24, a roughly 15.78% drawdown. Three risks dominate. First, valuation: AMD trades at a trailing P/E of 169 versus NVIDIA at 31, even though NVIDIA posts 65.6% operating margins compared to AMD’s 14.4%.

Second, China export restrictions cost $440 million in FY25 net charges and remain a wildcard.

Third, the prediction market composite target of $466.05 sits below the analyst consensus, and insider activity has tilted toward selling across 87 recent transactions.

The counterfactual: AMD’s elevated P/E reflects a real inflection. Operating income just grew 83%, and forward P/E compresses to 73x, normalizing as MI450 ships at scale. Citi has a buy rating with a $575 target while Bernstein raised the firm’s price target on AMD to $600 from $525 and keeps an Outperform rating on the shares.

AMD Price Prediction 2026-2030

Our 24/7 Wall St. price target of $561.83 reflects a buy rating at 90% confidence. The factor that tips the scale is the Data Center segment, growing 57% YoY with named hyperscaler commitments through 2027.

The bull thesis strengthens if MI450 ships on schedule in the back half of 2026 and Q2 hits the $11.2 billion guide. The thesis weakens if China export rules tighten further or if forward gross margin slips below 55%. At a beta of 2.49, position size matters as much as the thesis.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $540 |

| 2027 | $561.83 |

| 2030 | $732.94 |

These projections assume AMD continues converting its MI450 and EPYC Venice pipeline into revenue while protecting gross margins above the current 55% level. Significant upside or downside could result from share gains against NVIDIA in AI training workloads or a broader unwind of the AI capex cycle.