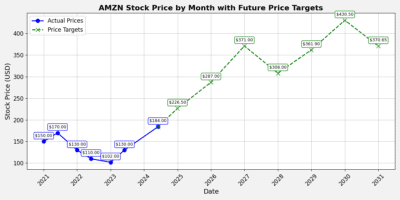

David Tepper’s Appaloosa Management trimmed NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) by roughly 13% of shares and cut AMD (NASDAQ:AMD) by roughly 32% of shares while nearly doubling its Amazon position, adding about 2.14 million shares (an increase of roughly 98%) during the quarter ended March 31, 2026. The disclosure landed in the 13F filed May 15, 2026, and the math of the rebalance is what matters: Amazon became Appaloosa’s single largest disclosed holding at roughly 15% of the portfolio. This is point-in-time data; it tells you how Tepper was positioned at quarter-end, not what he owns this morning.

The featured AI play is Amazon (NASDAQ:AMZN), and the AI angle is AWS. Tepper rotated capital out of two semiconductor names that have screamed higher into the hyperscaler that those chips sell into. AMD is up roughly 151% year to date through June 18, 2026, and NVIDIA has gained roughly 13% YTD after a multi-year run. Amazon, by contrast, is up about 6% YTD. The trim-and-rotate looks like classic Tepper: take profits in the crowded trade, shift dollars to the cheaper way to own the same theme.

The Thesis: AWS Is Reaccelerating

The underlying data supports the rotation. AWS revenue grew 28% YoY in Q1 2026 to $37.59 billion, the fastest pace in 15 quarters, with a 38% operating margin. The growth ladder is striking: 17% in Q2 2025, 20% in Q3, 24% in Q4, then 28% in Q1 2026. That is the signature of durable enterprise AI demand, not a one-quarter spike.

Amazon is also building the picks-and-shovels in-house. The custom chips business (Trainium, Graviton, Nitro) crossed a $20 billion revenue run rate with triple-digit YoY growth, and Amazon has locked in landmark commitments: roughly 2 GW of Trainium capacity for OpenAI starting in 2027 and up to 5 GW for Anthropic. CEO Andy Jassy framed it bluntly: “AWS is growing 28% (our fastest growth in 15 quarters) on a very large base, our chips business topped a $20 billion revenue run rate (growing triple digits year-over-year).”

Valuation is the kicker. Amazon trades around 34x earnings versus AMD’s stretched 202x. Q1 also delivered EPS of $2.78 against a $1.73 estimate, a 61% beat, with Q2 2026 guidance of $194 to $199 billion in revenue.

Should Retail Follow?

For a retirement-focused investor, the appeal is the diversified earnings base behind the AI exposure. Advertising revenue is running above $70 billion TTM and growing 24%, retail unit growth is healthy, and AWS provides the hyperscaler optionality. The risk worth respecting: planned 2026 capex of roughly $200 billion has crushed near-term free cash flow, and Q1 net income was lifted by $16.8 billion in non-recurring Anthropic investment gains. Polymarket traders are positioned consistent with the spending plan: an 87% implied probability that 2026 capex exceeds $200 billion.

The takeaway: Tepper’s rotation is worth studying, not blindly copying. Owning the customer of the AI buildout at 34x earnings, with a reaccelerating cloud franchise and a homegrown silicon business, is a defensible way to keep AI exposure without paying the chip-cycle premium. For a long-duration portfolio, Amazon at current levels lines up with the thesis. Keep an eye on the stock as AWS growth and capex digestion unfold over the next two quarters.