Amazon (NASDAQ:AMZN | AMZN Price Prediction) trades at $237.50 after a 10.33% pullback over the last month. With AWS reaccelerating, advertising compounding, and custom silicon scaling fast, I see the recent weakness as a setup for upside.

Our 24/7 Wall St. price target for Amazon is $322.05 over the next 12 months, implying 35.6% upside. Our recommendation is buy, with a confidence level of 90%, which I would describe as high conviction.

| Metric | Value |

|---|---|

| Current Price | $237.50 |

| 24/7 Wall St. Price Target | $322.05 |

| Upside | 35.6% |

| Recommendation | BUY |

| Confidence Level | 90% |

AWS Reaccelerates While the Stock Drifts

Amazon is up 2.89% year to date and 10.56% over one year, but the stock has cooled, with shares trading 12% below the 52-week high of $278.56.

In Q1 2026, Amazon posted EPS of $2.78 against a $1.73 consensus, a 60.69% beat, on revenue of $181.52 billion (up 16.6% YoY). AWS grew 28%, the fastest pace in 15 quarters, and the custom chips business crossed a $20 billion run rate growing triple digits. CEO Andy Jassy said “we’re in the middle of some of the biggest inflections of our lifetime.”

The Case for $368 and Beyond

Our bull case lands at $368.11, roughly 55% upside. OpenAI committed to roughly 2 GW of Trainium capacity starting 2027, Anthropic is securing up to 5 GW, and Project Rainier already has 500,000+ Trainium2 chips deployed.

Advertising crossed $70 billion in trailing revenue at +24% growth, Rufus AI is used by 300M+ customers and adding nearly $12 billion in incremental annualized sales, and Amazon Leo is signing names like Delta. Of the analysts covering AMZN, 62 are buyers and only 4 are holds.

What Could Go Wrong

The bear case lands at $278.36, still positive but barely. Capex of roughly $200 billion planned for 2026 has crushed near-term free cash flow, which fell 65.95% in full year 2025 to $11.19 billion.

AWS operating margin compressed from 39.5% to 37.7%, long-term debt has climbed to $119.1 billion, and Q1’s headline net income of $30.25 billion was lifted by a $16.80 billion Anthropic mark, which will not recur.

Polymarket traders currently put only 19% odds on AMZN closing June above $250. It should be noted that bulls would argue this capex is exactly the investment that locked in OpenAI, Anthropic, and Meta commitments. Tariff uncertainty and recession risk remain the wild cards.

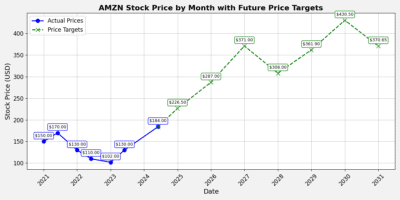

Amazon Price Prediction 2026-2030

The 24/7 Wall St. price target is $322.05, the recommendation is buy, and confidence is 90%. The tipping factor is AWS reacceleration coinciding with a stock that has pulled back 10.33% in a month. The setup looks constructive if AWS holds 25%+ growth into Q2 and the chips run rate keeps compounding.

The thesis weakens if 2026 free cash flow stays compressed into 2027 with no margin recovery in sight. For now, the risk-reward skews favorably for Amazon shares.

Looking further out, here is where our model projects Amazon could trade, assuming current growth trajectories and capex returns materialize.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $322 |

| 2027 | $380 |

| 2028 | $440 |

| 2029 | $500 |

| 2030 | $560 |

These projections assume Amazon converts AI infrastructure investment into durable AWS margin and that advertising, chips, and Leo scale as guided. Significant upside or downside could come from tariff policy, the trajectory of OpenAI and Anthropic compute spend, and whether 2026 capex delivers the ROIC management is promising.

Contact [email protected] for any questions or corrections.