Few large-cap software names have fallen as far, as fast, as Adobe (NASDAQ:ADBE | ADBE Price Prediction) over the past year. The stock has gone from a creative-software bellwether to a value puzzle, with the market pricing in AI disruption while management keeps raising guidance. That gap is where our model sees opportunity.

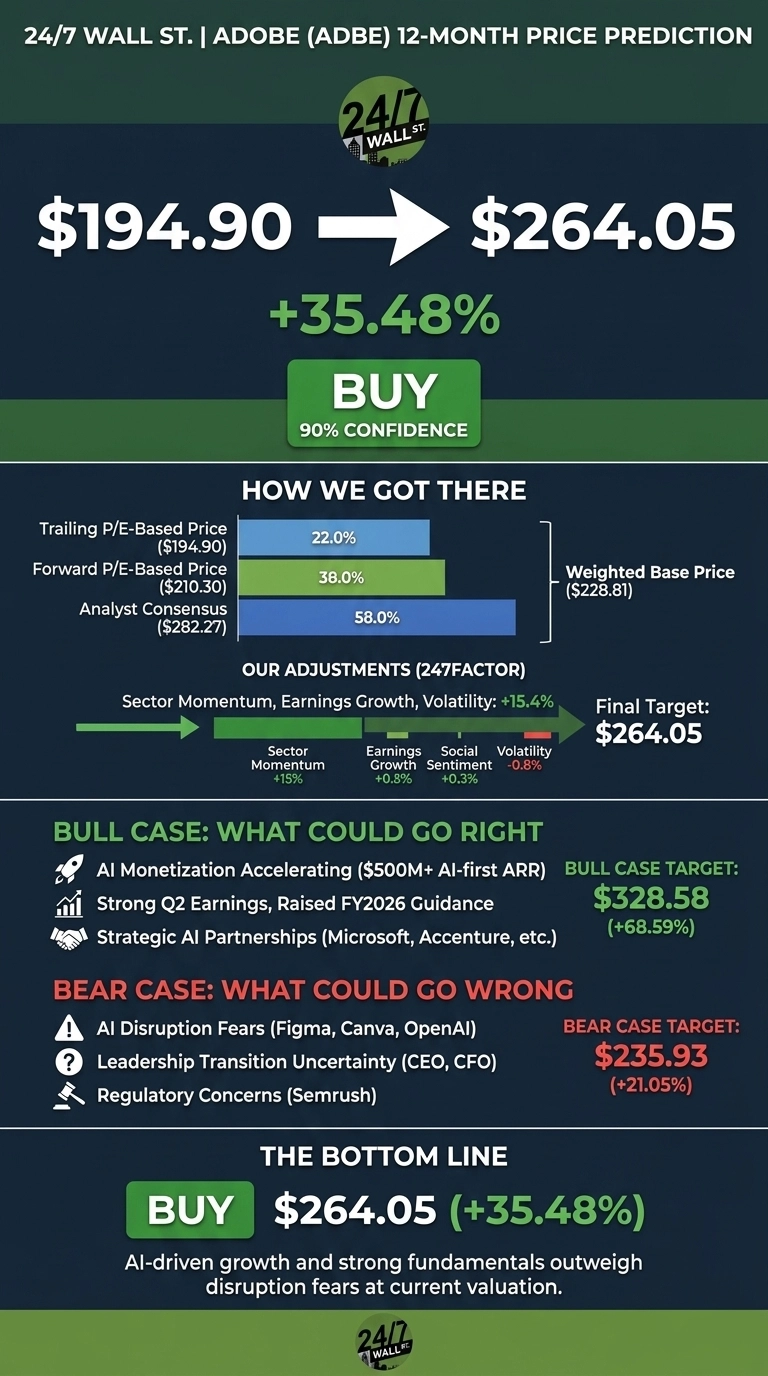

Adobe trades at $194.90 as of June 22, 2026. Our 24/7 Wall St. price target for Adobe is $264.05 over the next 12 months, implying 35.48% upside. Our recommendation is buy, with confidence of 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $194.90 |

| 24/7 Wall St. Price Target | $264.05 |

| Upside | 35.48% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Year of Pain Meets a Beat-and-Raise Quarter

ADBE has fallen 44.31% year to date and 48.29% over the past year, with shares trading 28% below the 52-week high of $392.58 and just above the $190.12 low.

Yet the fundamentals remain intact. Q2 FY2026 delivered record revenue of $6.62 billion, up 13% year over year, with non-GAAP EPS of $5.96 marking the fifth consecutive beat. AI-first ARR tripled to exceed $500 million, and management raised FY2026 revenue guidance to $26.50B–$26.60B.

The selling pressure comes from elsewhere. Citi cut its price target to $228 from $264 on June 20, citing a roughly $500 million implied reduction to organic ARR as Adobe pivots toward freemium acquisition. Sector-wide AI subscription fears, the CFO transition (Dan Durn departed June 15, 2026), and CEO succession have compounded the de-rating.

The Case for $328 and Above

Bulls point to AI monetization that is accelerating, not stalling. AI-first ARR moved from a $250M target in Q3 FY2025 to $500M+ by Q2 FY2026. The CX Enterprise Coworker launch and Cannes Lions partnerships with Accenture, Omnicom, WPP, Anthropic, and Microsoft reposition Adobe as agentic infrastructure rather than disruption target.

Operating cash flow hit $2.17 billion in Q2, funding $2.111 billion in buybacks. Our bull case price target is $328.58, a 68.59% return. The Reddit thesis put it bluntly: “Wall Street thinks AI is coming for Adobe’s lunch. I think Adobe already put it behind a paywall and called it dinner.”

What Could Go Wrong

The bear case is real. Freedom Broker downgraded ADBE to Hold from Buy, calling Adobe’s growth “acquired rather than organic” and pointing to a “show-me phase.” Generative AI competitors (Figma, Canva, OpenAI) threaten the creative workflow moat, and the 132 recent insider transactions have skewed net selling.

Q2 GAAP EPS of $4.25 reflected a $70M goodwill impairment and $30M litigation accrual, although those are non-recurring items and non-GAAP EPS still beat. Our bear case target is $235.93, still a 21.05% return from here.

Adobe Price Prediction 2026-2030

At an implied forward P/E near 8x, ADBE is pricing in significant AI disruption that the numbers do not yet show. Our 24/7 Wall St. price target of $264.05 implies 35.48% upside, with 90% confidence and a buy call.

The Q2 beat-and-raise tips the scale. The setup looks constructive if Q3 ARR growth holds at the guided trajectory. The thesis weakens if Adobe walks back its FY2026 ARR growth target of 10.2% on the next earnings report.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $231.09 |

| 2027 | $285.23 |

| 2028 | $355.18 |

| 2029 | $396.75 |

| 2030 | $445.34 |

These projections assume Adobe continues converting AI-first ARR into durable subscription revenue. Significant upside or downside could result from regulatory resolution on Semrush, new leadership execution, or a faster-than-expected shift in creative software economics.