Figma (NYSE:FIG) has whipsawed from post-listing euphoria into a brutal reset. After a punishing drawdown, the setup is more interesting than the recent price action suggests. Our analysis points to meaningful upside from current levels, driven by 46% top-line growth, a rebuilt valuation, and consensus quietly settled around a target well above the current price.

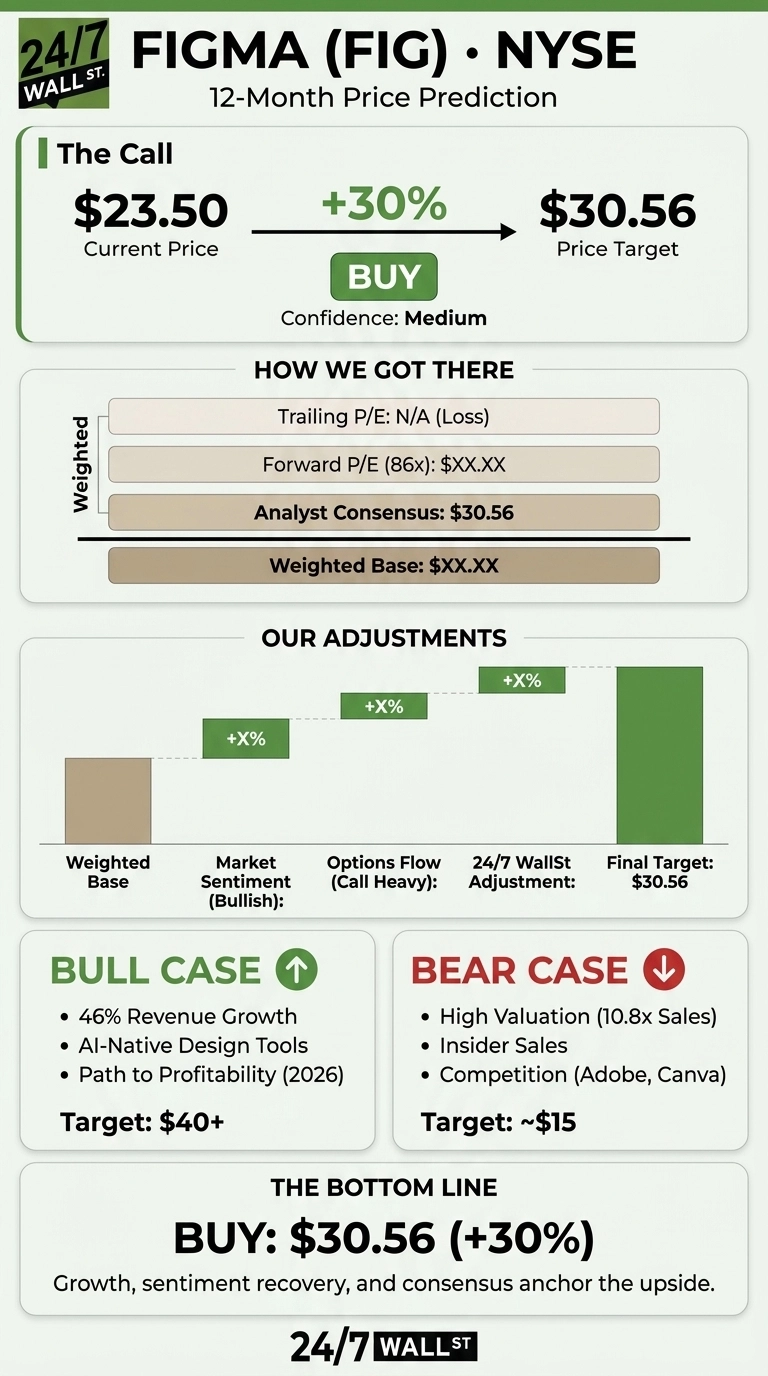

The 24/7 Wall St. price target for Figma is $30.56 over the next 12 months, implying 30.04% upside from the recent close of $23.50. Our recommendation is buy, with medium confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $23.50 |

| 24/7 Wall St. Price Target | $30.56 |

| Upside | 30.04% |

| Recommendation | BUY |

| Confidence Level | Medium (approximately 60%) |

From a $50 Billion Wipeout to a Cautious Comeback

Figma is down 79.65% over the past year and 37.12% year to date, having collapsed from a 52-week high of $142.92 to a low of $16.60. Shares are up 26.96% in the past month and 8.44% in the past week.

The turn is grounded in fundamentals. Q1 2026 revenue hit $333.44 million, growing 46% year over year, with a GAAP net loss of $142.4 million largely from stock-based compensation. CEO Dylan Field sold 174,430 shares on May 29, 2026 under a pre-arranged 10b5-1 plan. The next earnings report lands August 5, 2026.

Why Bulls See a Path to $40+

The bull case rests on hypergrowth, category dominance, and AI leverage. Revenue growing 46% nearly doubles what mature design software peers deliver. J.P. Morgan and RBC hold $28 price targets, while Piper Sandler projects profitability by year-end 2026.

If Figma monetizes AI-native design tools and paid subscribers expand, a bull scenario multiple of 13x forward sales supports $40 or higher.

The Risks Worth Watching

Figma trades at 10.76x sales while losing money, and its EV/EBITDA of 441x is not a real multiple. Insider sales from the CEO, CFO, CRO, and CTO between May and June signal capped near-term enthusiasm.

Bulls counter that these were pre-arranged 10b5-1 sales, and stock-based comp drove the GAAP loss. A downside scenario with multiple compression to 6x sales points to roughly $15.

How Figma Compares to Adobe and Autodesk

Adobe (NASDAQ:ADBE | ADBE Price Prediction) is the direct incumbent in creative software. Adobe posted Q2 FY26 revenue of $6.62 billion growing 13% with non-GAAP EPS of $5.96, and trades at roughly 3.4x forward sales. Figma grows more than three times faster but at three times the sales multiple, making our target reasonable rather than aggressive.

Autodesk (NASDAQ:ADSK) is the design-and-make comparable. Autodesk posted Q1 FY27 revenue of $1.93 billion up 18.4% at roughly 5.4x forward sales. Figma’s premium over Autodesk is justified by the growth gap but leaves less room for execution error.

| Company | Revenue Growth | P/S (approx.) |

|---|---|---|

| Figma | 46% | 10.76x |

| Adobe | 13% | 3.4x |

| Autodesk | 18% | 5.4x |

Figma Price Prediction 2026-2030

The 24/7 Wall St. price target of $30.56 implies buy with medium confidence. Growth, sentiment recovery, and consensus anchor the upside.

I’d be a buyer if the August 5 earnings report confirms revenue growth staying above 40% and paid subscriber momentum continues. I’d stay on the sidelines if Figma guides down or gross margin compresses. The risk-reward tilts constructive.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $30.56 |

| 2027 | $38.00 |

| 2028 | $46.00 |

| 2029 | $54.00 |

| 2030 | $62.00 |

These projections assume Figma sustains 25% to 35% annual revenue growth and reaches GAAP profitability by 2027. Significant upside or downside could result from AI-driven design disruption or aggressive competition from Adobe and Canva.

Contact [email protected] for any questions or corrections.