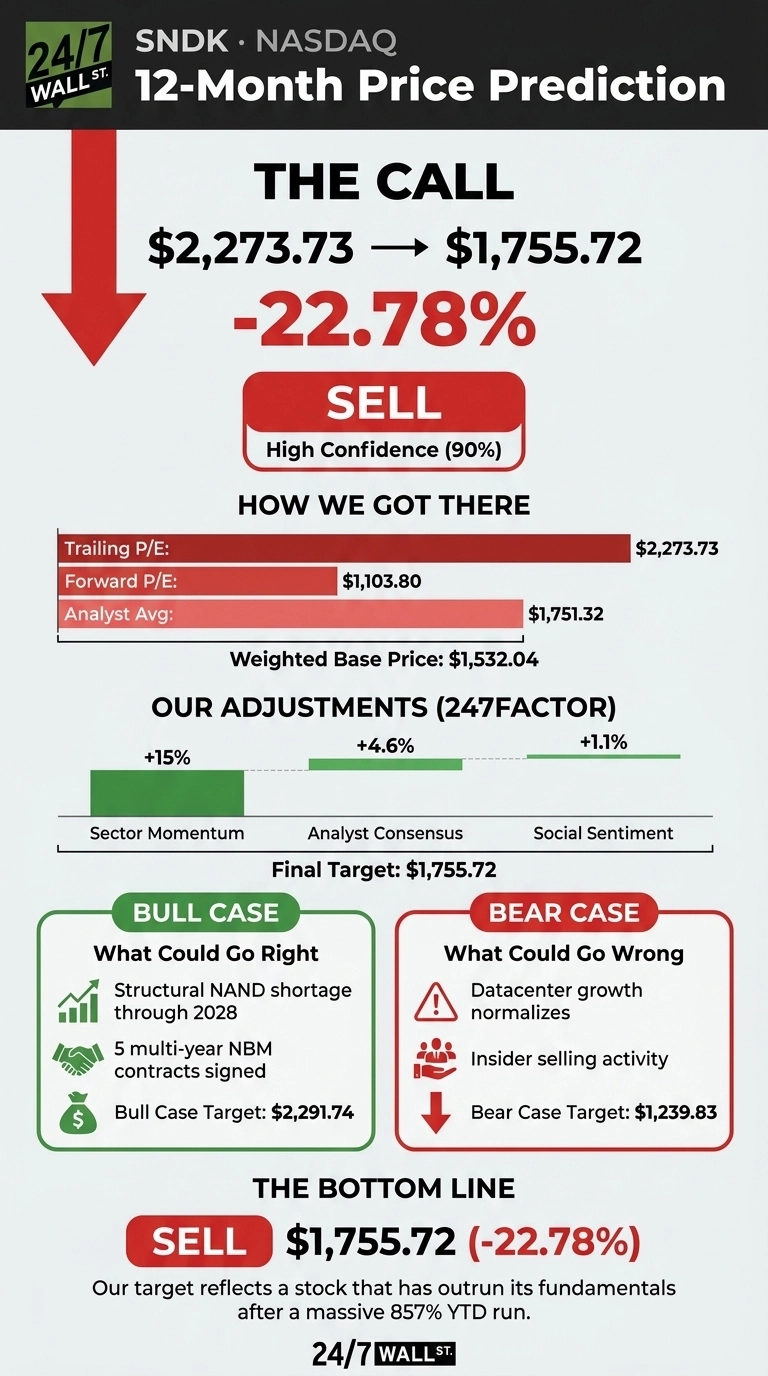

Our 24/7 Wall St. price target for SanDisk (NASDAQ:SNDK | SNDK Price Prediction) is $1,755.72, which sits roughly 22.78% below where the stock trades today.

After a 857.84% year-to-date run, the NAND maker has lapped almost every analyst on the Street, and our proprietary model now signals that risk and reward have inverted. Our recommendation is sell, with high confidence at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $2,273.73 |

| 24/7 Wall St. Price Target | $1,755.72 |

| Upside/Downside | -22.78% |

| Recommendation | SELL |

| Confidence Level | 90% |

Why We Could Be Wrong

Before going further, I should flag that SanDisk has been one of the most divisive stocks in the market. Real upside could come from a structural NAND shortage that Goldman Sachs projects through 2028, or from the company’s five signed multi-year New Business Model contracts that lock in pricing. Treat our 24/7 Wall St. price target as one datapoint among many. A full bull case appears below.

From $41 to $2,273 in Ten Months

SanDisk filed its Q4 FY25 results on August 14, 2025 at $41.55 a share. It now trades at $2,273.73, up 53.77% in the past month alone and 4,781.34% over the past year.

Q3 FY26 was the catalyst: revenue of $5.95 billion grew 251% year over year, EPS of $23.41 beat consensus by 59.67%, and gross margin expanded to 78.4% from 22.5% a year earlier. Datacenter revenue surged 645% year over year.

The stock is now 20% off its $2,191.69 high after retail enthusiasm cooled from very bullish Reddit sentiment scores of 82 to 85 in mid-June to neutral readings this week.

The Case for $2,200 and Higher

Mizuho lifted its target to $2,200 with an Outperform rating, and Bank of America’s Wamsi Mohan raised his target to $2,100 from $1,550, citing memory pricing strength through 2027. Bulls point to Q4 FY26 guidance for revenue of $7.75 billion to $8.25 billion and non-GAAP EPS of $30 to $33.

Zero long-term debt, a freshly authorized buyback, and CEO David Goeckeler’s framing of a “fundamental inflection point” support a bull case where SanDisk holds near current levels. Our model’s bull scenario lands at $2,291.74.

What Could Go Wrong

The bear scenario is sobering. Our model’s bear case projects $1,239.83, a 45.47% decline. Morningstar carries a $1,000 fair value with a 2-star rating, warning of bubble conditions. Monthly RSI hit 99.14, and insider activity has tilted heavily toward sales, including CTO Alper Ilkbahar selling 2,000 shares around $1,755 on June 1.

Bulls would counter that 645% datacenter growth and 78% gross margins reflect genuine operating leverage, and that NBM contracts dampen the historical NAND cycle. Still, Q1 FY26 datacenter revenue declined 10% year over year during qualification, a reminder that this segment is lumpy.

Hold the Gains, Trim the Risk

My read is that the 24/7 Wall St. price target of $1,755.72 reflects a stock that has outrun even its own outstanding fundamentals. Shares would look more constructive near the $1,751 analyst consensus with margins holding above 75%.

The risk-reward stays challenging while the stock trades north of $2,000 with insiders distributing. The recommendation is sell at high confidence.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $1,755.72 |

| 2027 | $1,680 |

| 2028 | $1,590 |

| 2029 | $1,520 |

| 2030 | $1,478.93 |

These projections assume the NAND cycle normalizes by 2028 and that NBM contracts deliver only partial insulation. Significant upside could result from sustained AI infrastructure demand outpacing supply, while downside risk centers on a memory glut and renewed Kioxia dependency stress.