Meta Platforms (NASDAQ:META | META Price Prediction) has slid hard in 2026, and that selloff has opened up a setup the model rates as one of the most attractive in mega-cap tech.

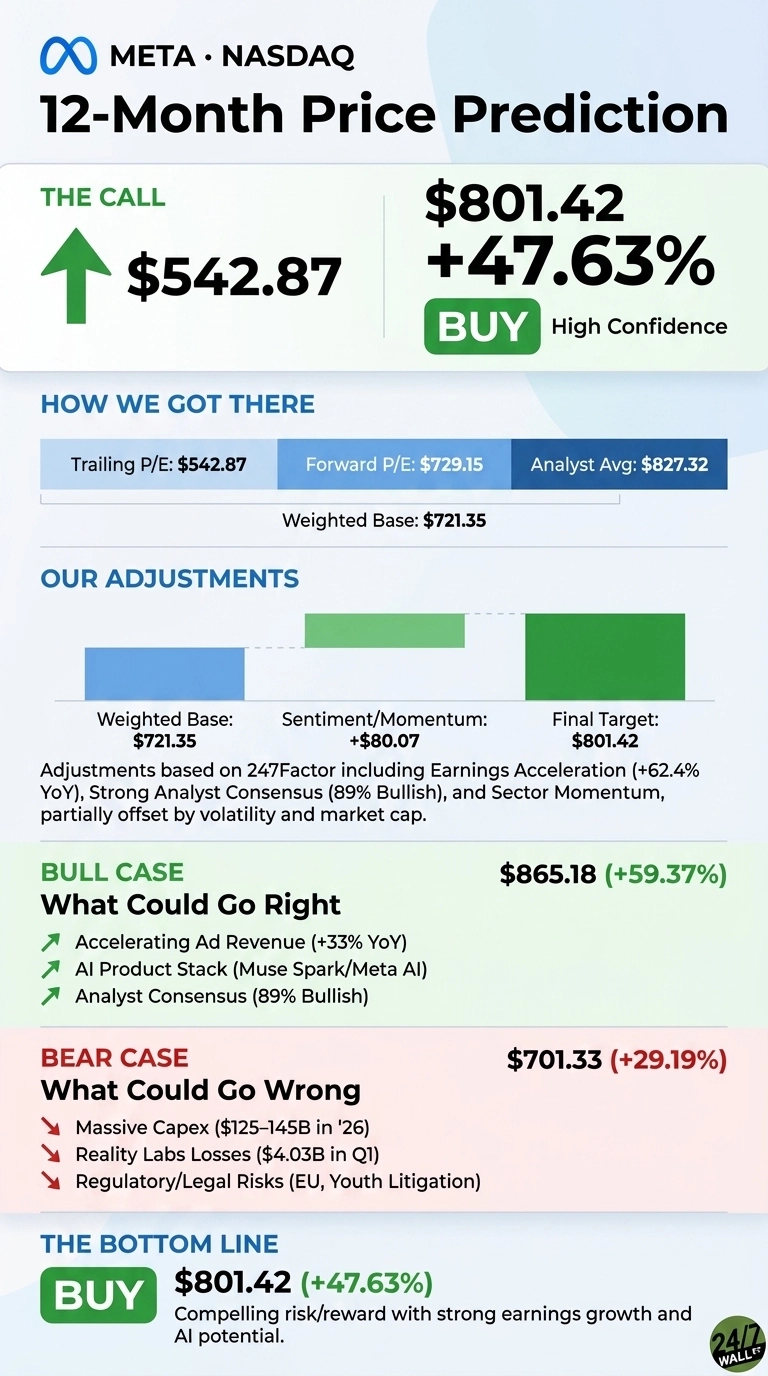

Our 24/7 Wall St. price target for Meta is $801.42 over the next 12 months, implying 47.63% upside from $542.87. The recommendation is a buy with high confidence at 0.9 on our 0 to 1 scale, driven by accelerating ad revenue, an expanding AI product stack, and a forward P/E that now sits in the mid-teens.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $542.87 |

| 24/7 Wall St. Price Target | $801.42 |

| Upside | 47.63% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Brutal 2026 Has Reset Expectations

Meta has been one of the year’s worst-performing megacaps. Shares are down 17.62% year to date, 11.27% over the past month, and 23.15% over the past year, sitting just above the $519.78 52-week low and well off the $793.65 high.

The selling has come despite a Q1 2026 report that posted $56.31 billion in revenue, up 33.08% YoY, with EPS of $10.44 against a $6.66 consensus. The bear narrative on Reddit is summed up by a viral r/wallstreetbets post titled “Satya and Zuckerberg are incinerating capital,” a reaction to the raised $125 to $145 billion 2026 capex range.

The Case for $865 and Higher

Bulls have a clean thesis. Advertising is reaccelerating, with Q1 ad impressions up 19% YoY and price per ad up 12%. CFO Susan Li flagged that Instagram ranking changes drove a “10% lift in Reels time spent”, and the value optimization suite’s revenue run rate is “over $20 billion, more than doubling year over year.”

Mark Zuckerberg called Q1 a “milestone quarter” on the back of Muse Spark, the first model from Meta Superintelligence Labs. With 57 buy ratings against zero sells and a Street target of $827.32, our bull case scenario points to $865.18, or 59.37% upside.

What Could Go Wrong

The bear case starts with capex. Meta raised 2026 capital expenditures to $125 to $145 billion, on top of $72.22 billion spent in 2025. Reality Labs continues to bleed, with a Q1 operating loss of $4.03 billion against only $402 million in revenue, and EU regulatory pressure plus 2026 youth-litigation trials remain unresolved.

It should be noted, however, that the Q1 EPS optically benefited from a $3.13 per share tax benefit. Stripping it out, underlying EPS of $7.31 still beat consensus, and management argues the capex is funding inference capacity that will monetize. Our bear scenario lands at $701.33, still 29.19% above the current price.

Meta Price Prediction 2026 to 2030

Stripping it down: Meta trades at a forward P/E of 18, generates a 41% operating margin, and is growing ad revenue at 33%. That combination at a discounted multiple is rare. The 24/7 Wall St. price target stays at $801.42 with a buy rating and high confidence.

The bull thesis hinges on management holding operating margins above 38% while the capex cycle peaks. The bear thesis centers on EU regulation or AI ROIC skepticism compressing the multiple further. The risk/reward at $542 is too asymmetric to ignore.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $801 |

| 2027 | $960 |

| 2028 | $1,150 |

| 2029 | $1,360 |

| 2030 | $1,589 |

These projections assume Meta continues converting AI infrastructure spend into ad pricing power and agent monetization. Material downside could come from regulatory rulings on EU ads or a sustained Reality Labs drag.