Meta Platforms (NASDAQ:META | META Price Prediction) is spending like an infrastructure company and being valued like a growth company. With full-year 2026 capex guidance raised to $125 to $145 billion to build out AI data centers, the question is whether shareholders get paid back for that bet.

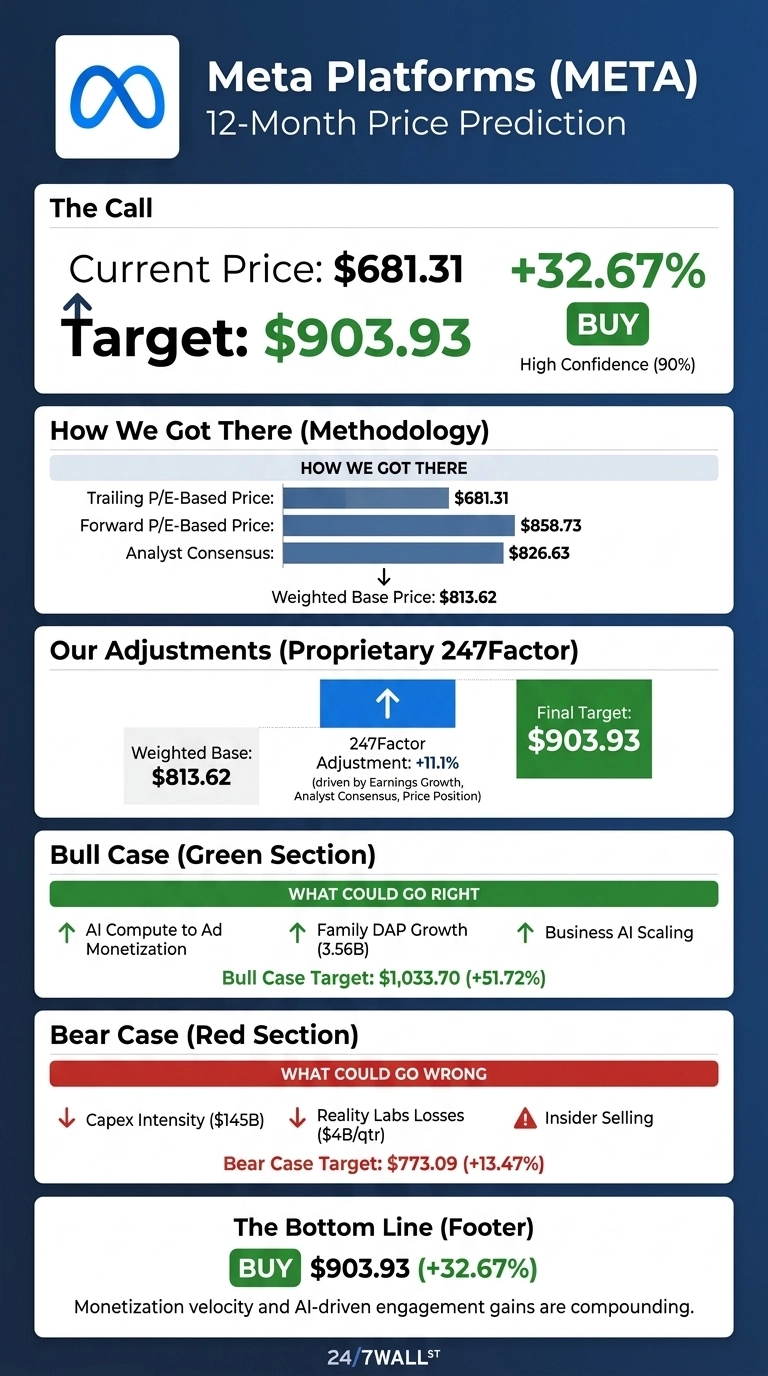

Our proprietary model says yes. The 24/7 Wall St. price target for Meta is $903.93, implying 32.67% upside from $681.31. Our recommendation is buy with high confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $681.31 |

| 24/7 Wall St. Price Target | $903.93 |

| Upside | 32.67% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Choppy Six Months, Then a Sharp Bid Back

Meta has been a rollercoaster. Shares are up 12.96% in the past week and 14.8% over the past month, but only 3.39% year to date and down 3.78% over the past year. The stock sits 4% below its 52-week high of $793.65 after bouncing off a 52-week low of $519.78.

Q1 2026 was a blowout: EPS of $10.44 beat expectations of $6.66 on revenue of $56.31 billion, up 33.08% YoY. Ad impressions rose 19% and average price per ad rose 12%. The stock initially sold off to $608.75 a day after the earnings report as investors digested the raised capex line.

Why Bulls See a Breakout Ahead

The bull case rests on Meta’s ability to convert AI compute into ad monetization. Family daily active people reached 3.56 billion, and Susan Li noted a 10% lift in Reels time spent on Instagram after Q1 ranking upgrades. Business AI conversations are running at more than 10 million weekly, up from 1 million at the start of the year.

Mark Zuckerberg said Meta is “on track to deliver personal superintelligence to billions of people.” Our bull scenario points to $1,033.70, a 51.72% return if Muse Spark and business agents scale on schedule.

What Could Go Wrong

The bear case starts with capex intensity. Q1 capex hit $19 billion, up 46.8%, and Reality Labs still bled $4.03 billion. Insider activity is not encouraging: COO Javier Olivan has been selling weekly, with CFO Susan Li disposing of 9,195 shares on May 18, 2026 around $604 to $611.

Bulls counter that these dispositions are largely scheduled RSU vestings rather than discretionary sales, and that the $8.03 billion tax benefit boosting Q1 EPS is a real cash item tied to CAMT R&D guidance. Our bear scenario lands at $773.09, a 13.47% return. Watch items include EU DMA pressure and 2026 youth-litigation trials.

How Meta Compares to Alphabet and Pinterest

Alphabet (NASDAQ:GOOGL) is the cleanest comp because both are AI hyperscalers funding data-center builds from ad cash flow. Alphabet’s 2026 capex guide of $175 to $185 billion dwarfs Meta’s plan, and Google Cloud posted $20.03 billion in Q1 revenue, up 63% YoY. Alphabet trades near a similar forward multiple with a diversified cloud engine Meta lacks, making Meta’s forward P/E of 21x look reasonable rather than rich.

Pinterest (NYSE:PINS) offers a smaller-scale ad-platform contrast. Pinterest grew Q1 2026 revenue 17.8% to $1.01 billion with 631 million MAUs. Meta’s 33% ad revenue growth at vastly larger scale, plus 41.44% operating margins, makes our $903.93 target look conservative against the peer set.

Meta Price Prediction 2026-2030

The 24/7 Wall St. price target of $903.93 with 90% confidence lines up with 57 buy ratings against zero sells. The tipping factor is monetization velocity: ad pricing plus AI-driven engagement gains are already compounding.

The setup looks constructive if Q2 2026 revenue lands at the top of the $58 to $61 billion guide. The thesis weakens if capex creeps past $145 billion without a matching lift in operating income.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $903.93 |

| 2027 | $1,050 |

| 2028 | $1,210 |

| 2029 | $1,370 |

| 2030 | $1,522.85 |

These projections assume Meta scales ad revenue faster than data-center depreciation and Reality Labs losses stabilize. Meaningful upside or downside could come from AI regulation shifts or a Muse family model breakthrough.

Contact [email protected] for any questions or corrections.