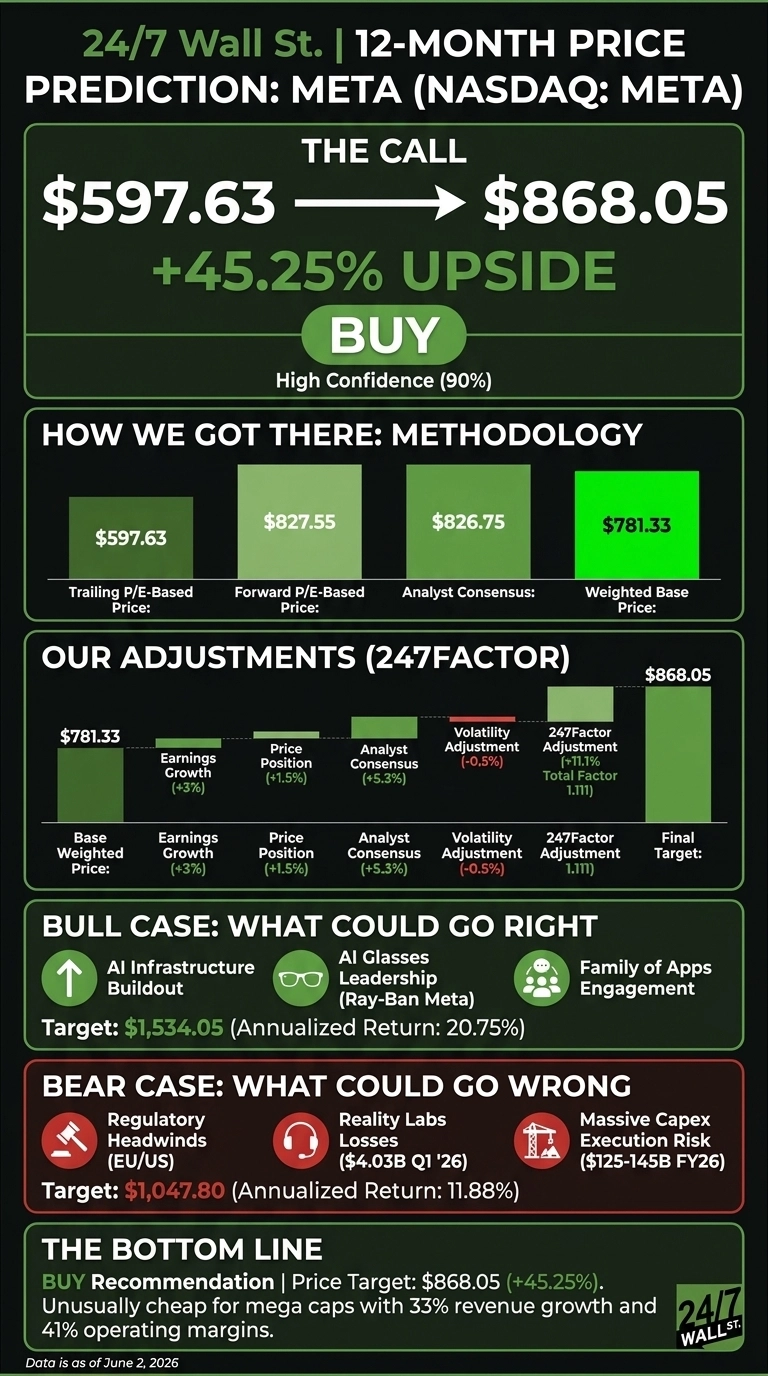

I’m leading with the number because that’s why you’re here. Meta Platforms (NASDAQ:META | META Price Prediction) closed at $597.63 on June 2, 2026, down 9.39% year to date. Our 24/7 Wall St. price target for Meta is $868.05 over the next 12 months, implying 45.25% upside. The recommendation is buy with a 90% confidence score, our highest tier.

| Metric | Value |

|---|---|

| Current Price | $597.63 |

| 24/7 Wall St. Price Target | $868.05 |

| Upside | 45.25% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Rough Six Months Has Created the Setup

Meta has been one of the more punished mega caps in 2026. The stock is down 2.4% on the week, 1.83% on the month, and sits 10.65% below its year-ago level, well off the 52-week high of $794.38.

Q1 2026 revenue came in at $56.31 billion, up 33.1% year over year, with EPS of $10.44 against $6.66 consensus. Ad impressions rose 19% and average price per ad climbed 12%.

The market spooked on capex. Full-year 2026 capital expenditures were raised to $125 to $145 billion, up from prior guidance of $115 to $135 billion. On June 2, Meta received an analyst upgrade, and Rosenblatt has a Buy rating with a Street-high $1,015 target.

The Case for $1,000 and Higher

Bulls point to Family of Apps daily active people hitting 3.56 billion, advertising revenue growth of 33%, and Meta Superintelligence Labs releasing its first model. The Street is overwhelmingly long.

Of 63 covering analysts, 56 have Buy ratings, 7 Hold, and zero Sell. Royal Bank of Canada reiterated Outperform with an $810 target, while Rosenblatt sits at $1,015. If 2027 EPS growth accelerates on AI-driven ad targeting and Reality Labs losses stabilize as CFO Susan Li suggested at the 2026 annual meeting, the bull-case scenario points to roughly $900 to $1,015.

The Risks Worth Watching

The bear case starts with capex. Spending $125 to $145 billion in a single year, on top of $72.22 billion in 2025, represents real execution risk. Reality Labs lost $4.03 billion in Q1 alone. Youth-related litigation trials in 2026 and EU enforcement add tail risk.

Reddit retail sentiment is bearish at 25, and Polymarket’s June 2026 contract puts only a 16.5% probability on Meta touching the $700 level this month. Bulls counter that depressed free cash flow reflects deliberate front-loading of AI infrastructure that should compound returns for years. A bear case where ad pricing rolls over and capex weighs on margins points toward the 52-week low of $520.26.

Meta Price Prediction 2026 to 2030

The 24/7 Wall St. price target stands as cited above, the recommendation is buy, and confidence is 90%. A forward P/E of 20 on a business growing revenue 33% with 41% operating margins is unusually cheap for mega caps.

The bull thesis holds if ad pricing remains firm and Meta’s AI capex flows through to monetization. The bear thesis gains traction if 10-year yields push toward 5% and force multiple compression across mega-cap tech.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $868 |

| 2030 | $1,678 |

These projections assume Meta executes on its AI infrastructure plan and Reality Labs losses stabilize. Significant upside or downside could result from regulatory action in the EU or a major AI product breakthrough from Meta Superintelligence Labs.

Contact [email protected] for any questions or corrections.