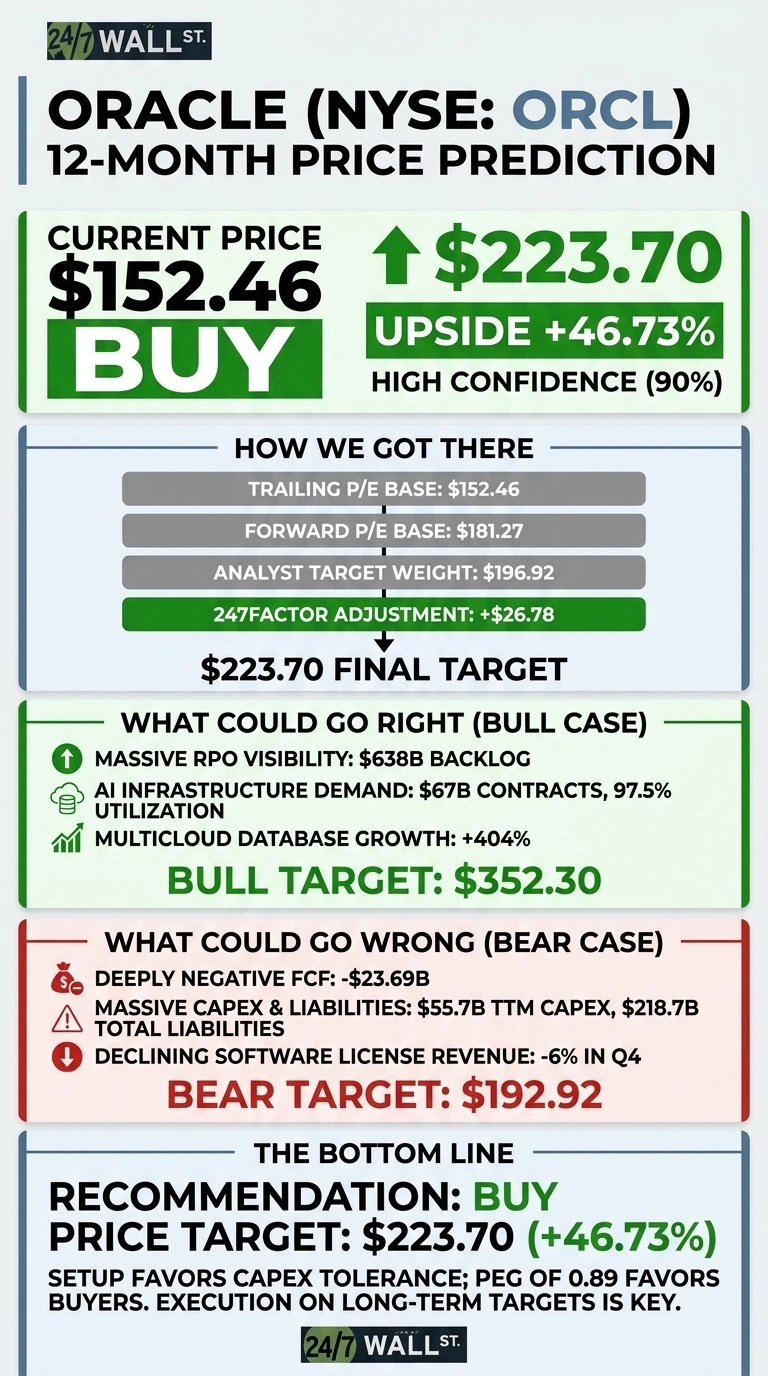

Oracle (NYSE:ORCL | ORCL Price Prediction) has been one of the most punished mega-cap AI stories of 2026, sliding from a $303.62 peak in October to $152.46 today. Our 24/7 Wall St. price target for Oracle is $223.70, implying 46.73% upside over the next 12 months. The recommendation is buy with high confidence (90%).

| Metric | Value |

|---|---|

| Current Price | $152.46 |

| 24/7 Wall St. Price Target | $223.70 |

| Upside | 46.73% |

| Recommendation | BUY |

| Confidence Level | 90% |

How a $303 Stock Became a $152 Stock in Nine Months

Oracle is down 17.27% over the past week, 21.03% in a month, and 31.8% from its September 2025 high.

Q4 FY2026, reported June 10, 2026, delivered $19.184 billion in revenue and $2.11 in non-GAAP EPS, both above estimates. Cloud Infrastructure grew 93% YoY to $5.787 billion, and remaining performance obligations reached $638 billion, up 363% YoY.

Shares closed down 8.53% on the earnings report as investors focused on -$23.686 billion free cash flow and planned $40 billion capital raise. CFO Hilary Maxson bought 224,441 shares at $185.35 on May 5. Seven directors followed with coordinated reinvestment on May 31.

The Case for $300+: Why Bulls See a Breakout

The bull case rests on RPO conversion. CFO Maxson told investors the $638 billion backlog provides “exceptional visibility,” with 12% recognizable in the next 12 months and another 34% in 13 to 36 months.

Cloud Infrastructure chief Clay Magouyrk noted Oracle signed “$67 billion in AI infrastructure contracts this quarter” with global GPU utilization at 97.5%. Multicloud database grew 404% in Q4.

Of 43 analysts covering Oracle, 30 rate it Buy and 6 Strong Buy, with a consensus target of $252.64. Our bull case projects $352.30 within 12 months if RPO converts ahead of schedule and OCI margins hold in the 30% to 40% range Magouyrk targeted.

What Could Go Wrong

Trailing CapEx of $55.663 billion drove free cash flow to -$23.686 billion, and FY2027 net cash CapEx is guided to around $70 billion. Total liabilities sit at $218.703 billion. Software license revenue shrank 6% in Q4.

Much of that spend is offset by $75 billion in customer-supplied or prepaid GPU contracts, which Magouyrk said carry no margin degradation. Reddit sentiment dipped to 32 (bearish) on June 25, though activity remained low. A bear case downside target sits at $192.92, still above today’s price.

Oracle Price Prediction 2026-2030

The setup at $152.46 favors investors who can stomach Oracle’s CapEx-driven volatility and trust that the $638 billion RPO converts on schedule. Caution is warranted for those who expect AI infrastructure demand to roll over before FY2028 or worry that the $40 billion capital raise pressures the stock further.

Shares trading at 19x forward earnings against 20.6% revenue growth and a PEG of 0.89 favor buyers. Our 24/7 Wall St. price target of $223.70 reflects that conviction.

Extending the 24/7 Wall St. model forward, here is where Oracle could trade assuming current cloud growth trajectories and capital plans hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $223.70 |

| 2030 | $439 |

These projections assume Oracle executes on long-term targets of 31% revenue CAGR and 28% EPS CAGR through FY2030. Material upside or downside could come from AI infrastructure demand shifts or GPU sourcing constraints.