Oracle’s (NYSE:ORCL | ORCL Price Prediction) stock has been through the wringer over the past year, but the long-term AI infrastructure story has only gotten more concrete. After the Q4 FY2026 earnings report on June 10, 2026, shares actually slipped, drawing attention to the gap between capital intensity and the backlog underneath.

Our 24/7 Wall St. Price Target for Oracle

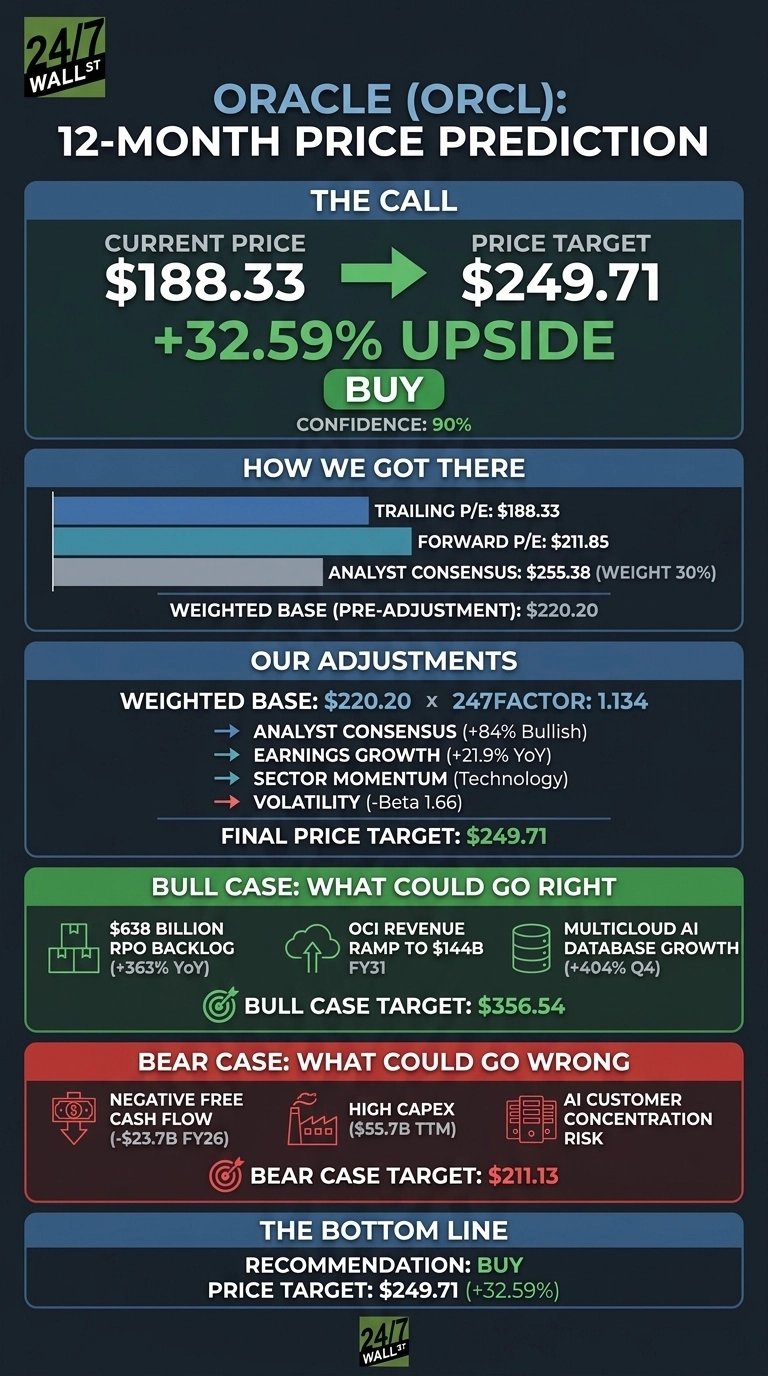

The stock trades at $188.33 as of June 16, 2026. Our 24/7 Wall St. price target for Oracle is $249.71 over the next 12 months, implying 32.59% upside. Our recommendation is buy, with confidence at 90%. The thesis rests on a record backlog, accelerating cloud mix, and a forward earnings ramp that the current multiple does not fully reflect.

| Metric | Value |

|---|---|

| Current Price | $188.33 |

| 24/7 Wall St. Price Target | $249.71 |

| Upside | 32.59% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Choppy Year Despite a Blockbuster Backlog

Oracle has been one of the more volatile mega-caps in the market. Shares are down 9.89% over the last year and 8.49% over the past week, and they sit 26% below the 52-week high of $343.01.

Q4 FY2026 revenue came in at $19.184 billion with non-GAAP EPS of $2.11. Cloud infrastructure revenue grew 93% to $5.787 billion, and Remaining Performance Obligations exploded to $638 billion, up 363% year over year. Free cash flow swung to negative $23.686 billion as capex hit $55.663 billion, which is what concerned investors.

Why Bulls See a Breakout Above $350

The bull case rests on Oracle’s RPO conversion. CFO Safra Catz has pointed to an OCI revenue ramp from $18 billion in FY2026 to $144 billion within five years. Management has confirmed an FY2027 revenue target of $90 billion with non-GAAP EPS of $8.05.

Multicloud AI Database revenue grew 404% in Q4, and Oracle Health is expected to reach double-digit growth on the new AI Cerner release. If the 247Factor compounds at the bull rate, our model points to $356.54 within 12 months, an 89.32% total return.

What Could Go Wrong

The bear case starts with the balance sheet. Total liabilities sit at $218.703 billion, and management plans to raise roughly $40 billion in FY2027 through debt and equity. Software license revenue declined 6% in Q4, and AI customer concentration is a real risk.

Bulls would counter that $75 billion of RPO is tied to prepaid or customer-supplied GPU arrangements, which softens Oracle’s capital burden materially. The bear case in our model lands at $211.13, still 12.11% above current levels.

Oracle Price Prediction 2026-2030

Our 24/7 Wall St. price target for Oracle of $249.71 reflects a buy rating at 90% confidence. The tipping factor is the $638 billion backlog, which gives unusually high revenue visibility for a mega-cap.

The setup looks constructive if Oracle converts even a fraction of RPO on schedule and OCI growth holds above 60%. I would stay on the sidelines if capex runs further past $55 billion without matching cash generation, since that would pressure the multiple regardless of bookings.

Looking further ahead, here is where our model projects Oracle could trade in the coming years, anchored to base case trajectory data.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $210.93 |

| 2027 | $257.76 |

| 2028 | $301.92 |

| 2029 | $352.42 |

| 2030 | $394.86 |

These projections assume Oracle continues converting its RPO into recognized revenue at current trajectories. Significant upside or downside could result from AI capex discipline, GPU supply, and the pace of customer cloud migrations.

Contact [email protected] for any questions or corrections.