Oracle (NYSE:ORCL | ORCL Price Prediction) just posted one of the strongest cloud quarters in software history. Infrastructure revenue grew 93% year over year to $5.79 billion, and remaining performance obligations hit $638 billion. Yet shares trade at $148.53, down 23.33% YTD. Market cap sits at $427.8 billion. Can this stock reach $400 a share and push Oracle past a $1 trillion market cap by 2030?

The Real Reason Oracle Is Down 23% This Year

Capital intensity. Oracle spent $55.66 billion on capital expenditures in FY2026 to build AI infrastructure, generating free cash flow of negative $23.69 billion. Total liabilities climbed to $218.7 billion, and management plans to raise roughly $40 billion in debt and equity in FY2027.

Investors are nervous. Shares fell 19.4% over the past week and 22.22% over the past month, taking ORCL from $190.96 to current levels. A beta of 1.655 makes the unwind worse than the market. The bear case: Oracle is borrowing heavily to chase AI workloads, and any slip in cloud margins detonates the model.

Wall Street Sees 70% Upside. Our Model Sees More

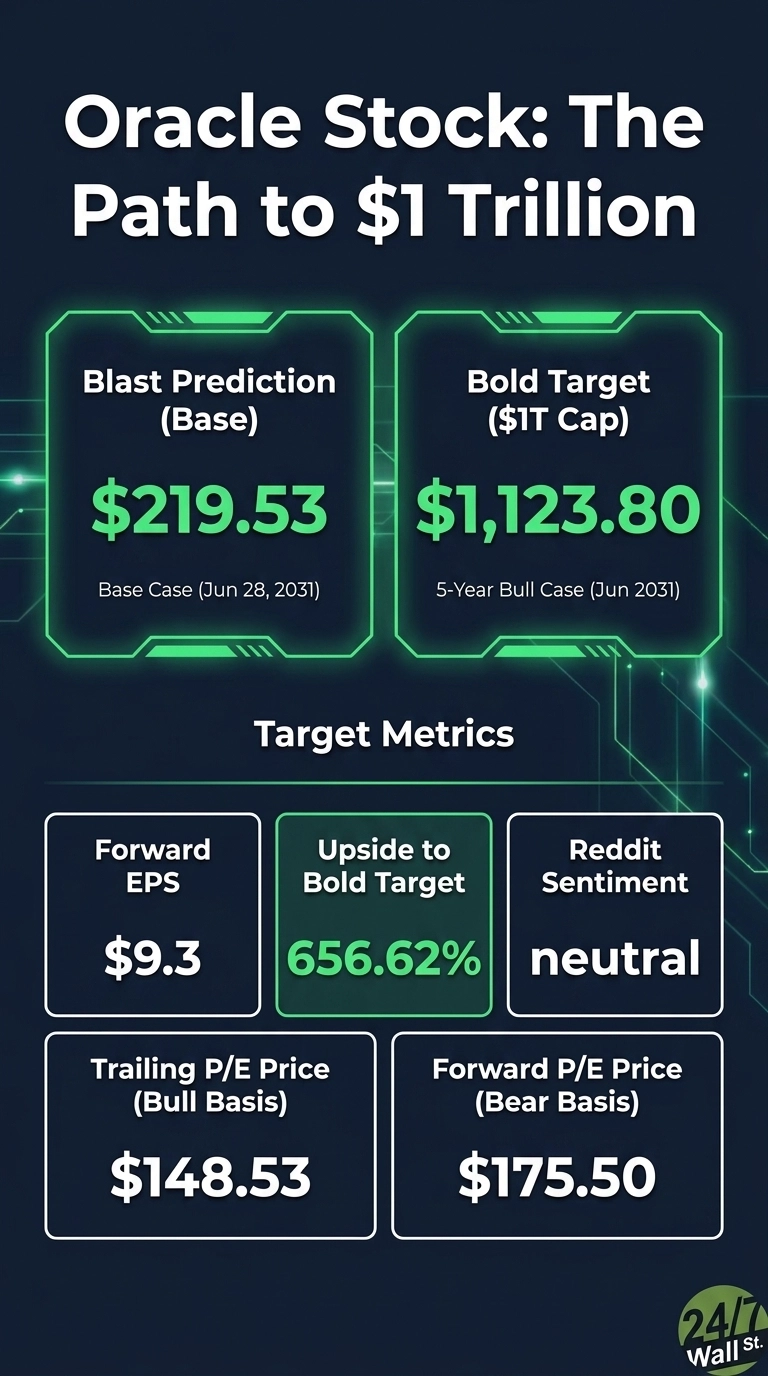

Wall Street’s consensus target is $252.64, with 6 Strong Buy, 30 Buy, 6 Hold, and 1 Sell ratings. Our base case lands at $219.53, implying 47.8% upside with 90% confidence. The bull scenario reaches $351.63. The bear scenario still gets to $190.

Analysts appear to be modeling the next twelve months, not the booked backlog. With 84% bullish analyst sentiment and 21.9% YoY earnings growth, $252 looks conservative once OCI scales toward the FY2030 plan.

The Path to $400 Per Share

Reaching $400 from $148.53 requires a gain of 169.3%. With forward EPS of $9.30, a price of $400 implies a forward P/E of 43. Our base case of $219.53 already implies 19x, meaning the bold target requires 24x of additional multiple expansion.

That sounds extreme until you stack the forward EPS curve. Oracle guided FY2027 non-GAAP EPS to $8.05 on $90 billion in revenue, with OCI scaling to $144 billion by FY2030. If those targets land, a 43x multiple today becomes far lower tomorrow.

CEO Clay Magouyrk noted “It is unprecedented to scale a capital-intensive business so quickly while also increasing profitability.” Multicloud database revenue jumped 531% year over year, and AI infrastructure rose 243%. Our model’s 1.136 adjustment factor reflects that. The primary risk is execution slippage on the $55B annual CapEx commitment.

Where Oracle Trades Today vs Its Earnings Power

At $148.53, Oracle trades at roughly 16x forward EPS of $9.30. That is cheap for a software company growing cloud revenue above 50% with a half-trillion-dollar backlog. The 52-week range of $134.57 to $343.01 shows how violently this name moves.

The 10-year return of 340.64% demonstrates the long-term compounding is real. Buyers at today’s multiple are paying a hardware price for a generational software asset.

Is $400 Realistic? Here’s My Verdict

Reaching $400 from $148.53 demands a 169.3% gain. That is a stretch goal, not a base case.

For it to land by 2030, three things need to go right: OCI revenue must hit the $144 billion FY2030 target, AI infrastructure gross margins must keep climbing past the 32% already delivered, and the $638 billion RPO backlog must convert without major customer concentration breaks. What derails it is a sharp pullback in AI capex by hyperscalers or enterprises. We’ve outlined the blueprint for how Oracle could reach $400 in 2030.

Contact [email protected] for any questions or corrections.