One year into Antonio Filosa’s tenure as Stellantis (NYSE: STLA | STLA Price Prediction) chief executive officer, the verdict from investors is harsh, the operational data is genuinely mixed, and the strategic bets are still loading. Its shares have lost 38.7% since Filosa formally took the helm on June 23, 2025, closing at $5.74 on June 25, 2026, versus $9.36 at his start.

24/7 Wall St. opinion: Grade C−. This is an editorial judgment. A stock price reflects the company’s trajectory but captures only part of a CEO’s impact, and 12 months is a short window for a turnaround of this scope.

The Bear Case

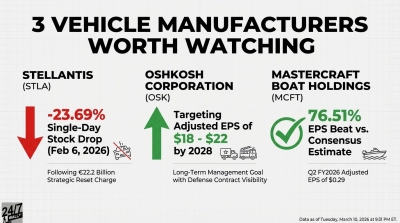

The shareholder pain is severe. The stock is down more than 48% year-to-date and about 42% over one year. Q4 2025 included $25.41 billion in unusual charges, including $9.07 billion in program cancellations and $6.58 billion in North American platform impairments. The FY 2025 net loss reached $22.33 billion, the 2026 dividend was suspended, and both S&P (BBB-) and Moody’s (Baa3) downgraded the credit.

Filosa said: “Our 2025 full year results reflect the cost of over-estimating the pace of the energy transition.” Add a 1 million-plus Jeep Wrangler/Gladiator fire-risk recall tied to 72 reported fires, a Schall Law securities-fraud class action, European registrations down 2.3% in May with share at 15.3%, and an AlphaValue/Baader downgrade citing Chinese OEMs reaching 10% European share, and the bear case practically writes itself.

The Bull Case

Filosa inherited a six-month leadership vacuum, a bloated EV roadmap, and U.S. tariff exposure. Execution is improving. Adjusted diluted Q1 2026 EPS hit $0.246 versus a $0.083 estimate, revenue reached $44.6 billion, and North America was the primary growth engine that pulled the entire global company out of the red. First-month service issues fell by more than 50% in North America.

Forward bets are credible: a $13 billion U.S. investment, the Stellantis-Wayve-Uber Level 4 robotaxi partnership, a €5 billion Italy plan through 2030, 30,000 Leapmotor vehicle sales in Italy, and a 9.5% Factorial Energy solid-state stake.

What Moves the Grade

Upward pressure comes from: positive industrial free cash flow before the 2027 target, European margin recovery from the 0.1% Q1 AOI floor, and execution on the 10% buyback authorization. Downward pressure comes from: another warranty surprise, securities-litigation escalation, or further share loss to Chinese rivals. The consensus analyst target is $9.19. Filosa has a runway, but he has not yet earned a higher mark.