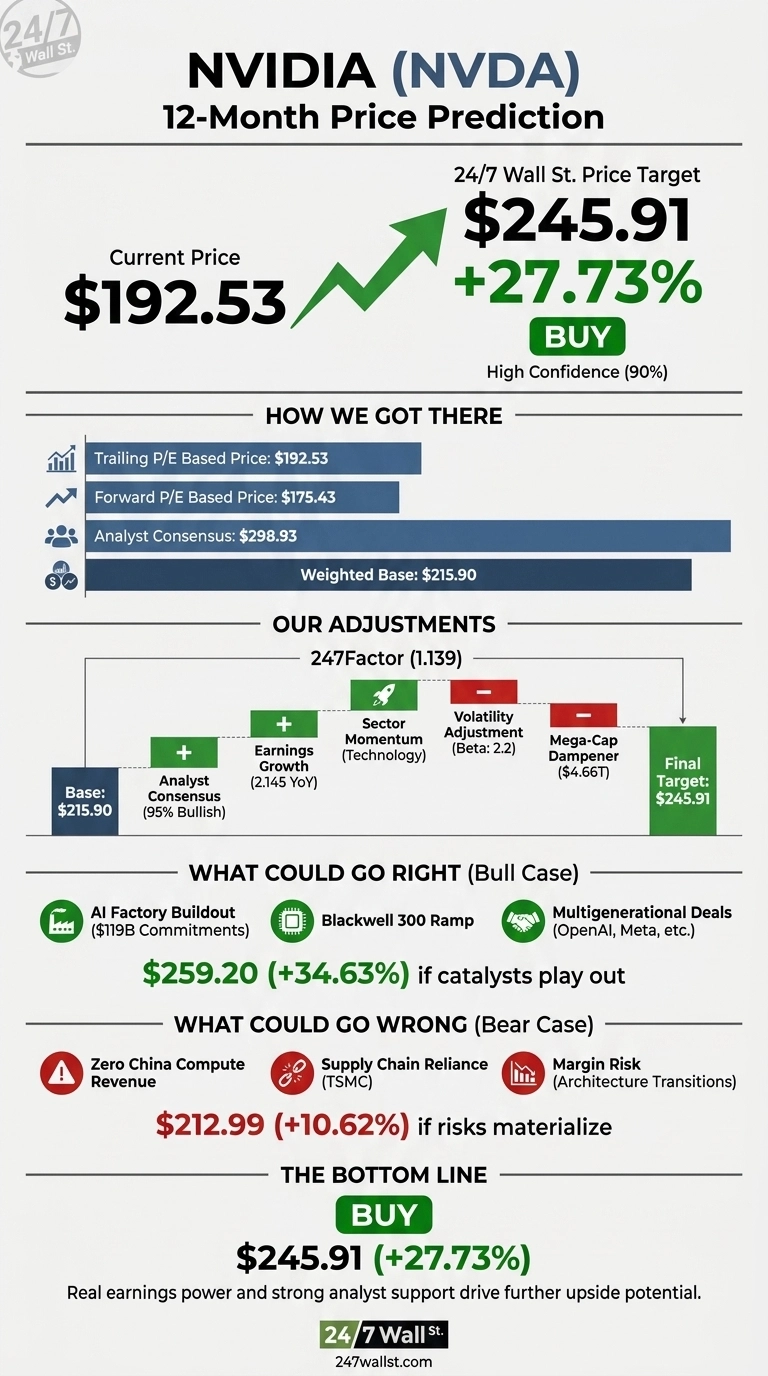

NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) stock has cooled off this summer, but the 24/7 Wall St. price target says the pullback looks like a setup for further upside. Shares closed at $192.53 on June 26, 2026, down 8.62% on the week, even as Wall Street remains overwhelmingly bullish. Nvidia is the most-owned megacap in the AI build, and our model thinks the recent dip widens the runway for further upside.

Our 24/7 Wall St. price target for NVIDIA is $245.91 over the next 12 months, implying 27.73% upside. The recommendation is buy, with a confidence score of 90%, which we consider high.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $192.53 |

| 24/7 Wall St. Price Target | $245.91 |

| Upside | 27.73% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Summer Wobble Inside a Bigger Uptrend

NVIDIA is up 24.36% over the past year and 3.36% year to date, but the last month has been ugly, with shares off 9.34%. The stock sits 27% below its 52-week high of $236.26 and well above the $151.29 low.

Fundamentals have not cracked. Q1 FY2027 revenue hit $81.615 billion, up 85.23% year over year, with non-GAAP EPS of $1.87 beating expectations. Data Center revenue reached $75.246 billion, up 92%, with networking revenue tripling at 199% growth. Q2 guidance came in at $91 billion. NVIDIA also launched the BioNeMo Agent Toolkit for life sciences, extending the platform beyond pure compute.

Why Bulls See a Breakout Toward $300

The bull case rests on Blackwell. CEO Jensen Huang called the AI factory buildout “the largest infrastructure expansion in human history”, and NVIDIA has locked in $119 billion in supply commitments. Multigenerational deals with OpenAI (10GW), Anthropic (1GW), Meta, Microsoft, Google Cloud, and Oracle anchor demand into the Vera Rubin platform.

Of 61 covering analysts, 58 rate NVDA Buy or Strong Buy versus just 1 Sell. The Street consensus target is $298.93. If Blackwell 300 ramps at 75% gross margins and Q2 results come in near guidance, the bull scenario points to $259.20, a 34.63% one-year return.

The Risks Worth Watching

The bear case starts with concentration. The model assumes zero China Data Center compute revenue, and further export tightening hits sentiment more than numbers. Supply-chain reliance on TSMC, a planned cash tax jump in Q2, and gross margin risk during architecture transitions are real. Retail conviction is wobbling, with Reddit traffic this month flagging AI stock losses and Chinese model parity on Huawei silicon.

Insider selling has picked up, with 9 recent transactions net selling. Bulls counter that these are routine 10b5-1 trims against $20 billion in Q1 buybacks and a fresh $80 billion repurchase authorization. The bear scenario still produces $212.99, a 10.62% gain.

NVIDIA Price Prediction 2026-2030

At $192.53, the 24/7 Wall St. price target of $245.91 leans on real earnings power rather than relying on multiple expansion, and even the bear case is positive. Key signals to monitor: whether Q2 prints above the $91 billion guide, whether gross margins hold above 73%, and whether export rules expand beyond H20. The current pullback is worth watching closely.

Looking further out, here is where the 24/7 Wall St. price target model projects NVDA could trade, assuming current growth trajectories hold and the AI capex cycle extends through the Vera Rubin generation.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $245.91 |

| 2027 | $285.00 |

| 2028 | $320.00 |

| 2029 | $355.00 |

| 2030 | $391.74 |

These projections assume NVIDIA holds platform leadership through Vera Rubin and hyperscaler capex grows in line with current commitments. A China policy reversal would be meaningful upside, while a credible domestic Chinese alternative or hyperscaler in-house silicon shift would compress the trajectory.

Contact [email protected] for any questions or corrections.