The thesis is straightforward: SpaceX (NASDAQ:SPCX | SPCX Price Prediction) gets added to the Nasdaq-100 on July 7, and every index fund, ETF and benchmark-tracking pension on the planet has to buy it whether they like the valuation or not. That is mechanical demand against a float that has been public for 11 trading days, and it is the cleanest forced-flow catalyst the market has seen in years.

The Catalyst Is Already Priced In, but Not Enough

Nasdaq announced the inclusion after Friday’s close, calling it one of the quickest ever additions to the high-profile index following last month’s rule change. Prediction markets have caught on. Polymarket is currently pricing a 92% probability that SPCX closes the week of June 29 above $145, with the single most-favored outcome being a close above $175 at 31% implied probability. The stock is already up 6% over the past week heading into the trigger date. Funds front-running the rebalance are buying now, not on July 7.

The Revenue Story Has Quietly Doubled

The bear case rests on a stale revenue number. SpaceX did $18.7 billion in 2025 revenue, up 33% year over year, with a GAAP loss. That was the pre-xAI company. Post-merger, the AI segment has signed contracts totaling $27.8 billion in annual revenue with Anthropic, Alphabet and Reflection AI.

The Anthropic deal alone pays $1.25 billion per month for roughly 300 megawatts of Colossus compute. The Google deal adds $920 million per month for about 110,000 GPUs through 2029. Stack that on Q1 2026 sales of $4.7 billion, and the company is tracking to $38.6 billion in revenue this year. That is a hyperscaler growth profile that did not exist six weeks ago.

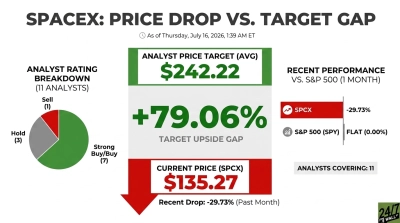

Wall Street Targets Confirm The Upside

Current price sits around $170. The consensus analyst target is $187.80, implying 11% upside before the index buying even begins. Sentiment has moved with the setup, with the composite score climbing +14.95 over the past seven days.

Defiance ETFs CIO Sylvia Jablonski put it bluntly, arguing “investors are underestimating SpaceX by viewing it solely as an aerospace company” and pointing to Starlink and AI connectivity as the underappreciated legs of the story.

The Valuation Risk, Dismissed

The pushback writes itself: The stock trades at 112 times trailing sales, which is the wrong number to anchor on. On forward revenue of $38.6 billion, the multiple compresses to roughly 54 times sales, and that figure shrinks every quarter the hyperscaler deals scale. Palantir trades at 37 times forward sales with materially slower growth. SpaceX is growing the top line at a rate that closes that gap inside of two reporting cycles.

The catalyst is dated, the buyers are forced, and the revenue trajectory has already re-rated. Investors positioning ahead of July 7 are making a straightforward call.

Contact [email protected] for any questions or corrections.