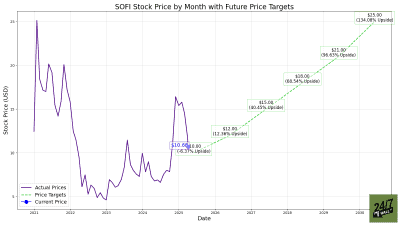

SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction) is trading around $18 as of July 7, 2026, still down 31.3% year-to-date after a brutal spring. The catalyst for the drawdown: a March 2026 Muddy Waters report alleging accounting misstatements and undisclosed charge-off rates. Yet shares have rallied 12.2% over the past month, raising the question of whether the stock has bottomed.

The Fundamentals Never Broke

The bear thesis was that credit was cracking beneath the surface. The Q1 2026 earnings report, filed April 29, 2026, argued otherwise. Revenue hit $1.10 billion, beating consensus by 4.9%, with EPS of $0.12 matching estimates for the fourth straight quarter. GAAP net income of $166.73 million rose 134.5% year over year, and loan originations set a record at $12.18 billion.

CEO Anthony Noto said, “We had an excellent Q1 delivering another quarter of durable growth and strong returns, fueled by our relentless focus on innovation and brand building.”

What Sparked the Bounce

Recovery catalysts have stacked up quickly. On June 23, 2026, SoFi acquired Composer Securities and launched Composer by SoFi, an AI-powered investing platform. Noto argued, “As AI becomes a foundational part of investing, Composer by SoFi strengthens our ability to deliver powerful investing tools through an experience that is simple, intuitive, and accessible.” Days later, the company rolled out small business loans up to $250,000 with 24-hour funding.

Smart money has been leaning in. Cathie Wood’s ARK made four consecutive purchases, including over 200,000 shares (around $3.62 million) on June 30, 2026. Jim Cramer reiterated an “I Continue to Believe It’s Time to Buy” stance on June 23, 2026. For investors weighing how to play post-selloff setups, 24/7 Wall Street’s Breakout Buyers Rulebook covers the framework.

The Bear Case Hasn’t Vanished

The Muddy Waters overhang lingers. Signal Law Group followed up on June 27, 2026, with a Securities Disclosure Risk bulletin. Credit metrics are drifting: personal loan charge-offs rose to 3.0% from 2.8% sequentially, student loan charge-offs to 0.7% from 0.5%, and average asset yields fell 63 basis points. The Technology Platform segment shrank 27% after a large client departure.

Wall Street is unconvinced. The consensus rating is Hold, with an average target of $20.90. The forward P/E of 30x relative to 2026 guidance of approximately $0.60 in adjusted EPS leaves little room for error.

Verdict: Off the Lows, Not Yet Confirmed

Shares have clearly recovered from the $16.03 low in early June, and the operational story continues to support the bulls. Whether $18 holds as a durable base depends on the July 29, 2026, Q2 earnings call, where analysts expect revenue of $1.1 billion and EPS of $0.11. Investors should monitor the stock and, more importantly, the charge-off trajectory.

Contact [email protected] for any questions or corrections.