SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction) has been one of 2026’s most punished fintechs, with shares down 34.57% year to date even as the underlying business posted record numbers.

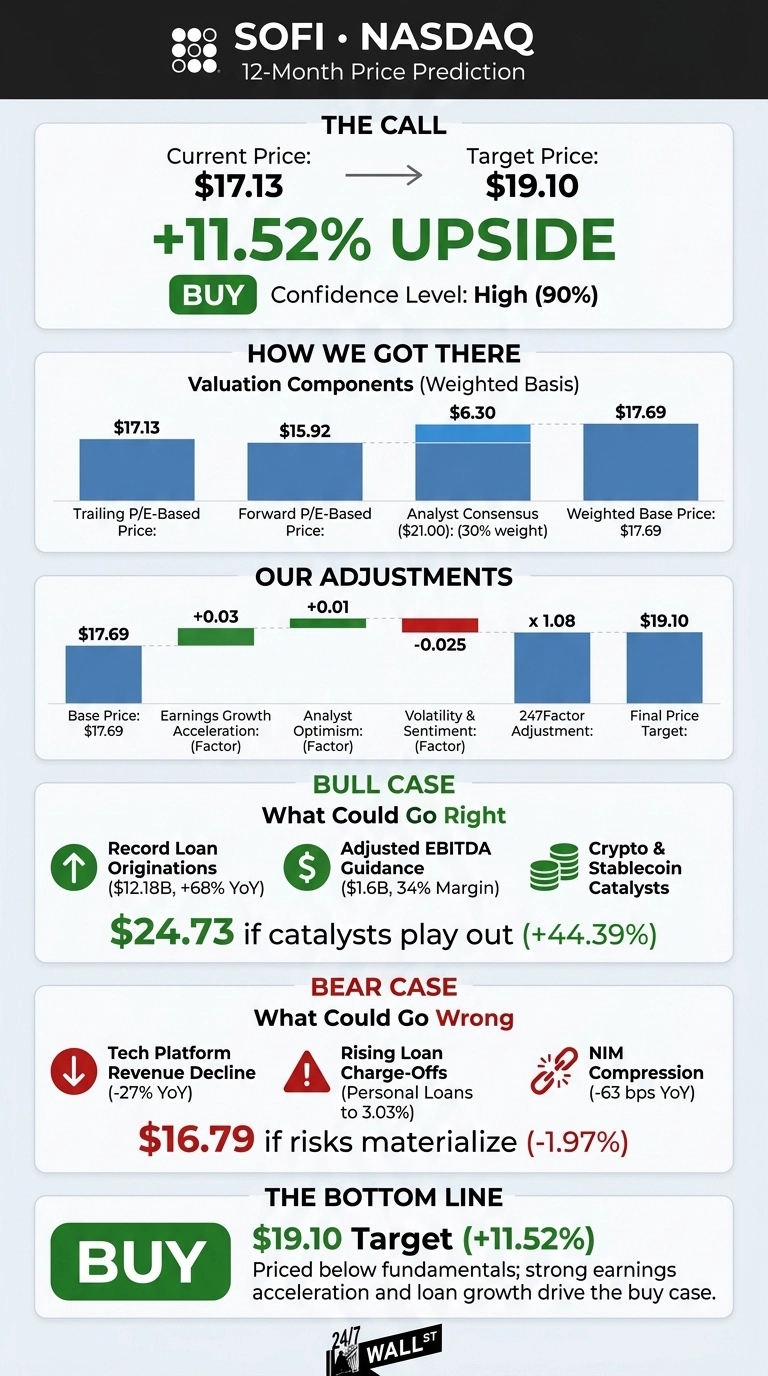

After running the financials through our proprietary model, I think the selloff has overshot the fundamentals. Our 24/7 Wall St. price target for SoFi is $19.10, implying 11.52% upside from the $17.13 close. The recommendation is buy, with high confidence at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $17.13 |

| 24/7 Wall St. Price Target | $19.10 |

| Upside | 11.52% |

| Recommendation | BUY |

| Confidence Level | 90% |

From $27 to $17: A Brutal First Half for SoFi

SoFi entered 2026 near $26.44 and slid as low as $14.23 on its 52-week low before stabilizing. Shares are up 9.74% over the past month and 21.58% over the past year, but still sit 36% below the $32.73 high. The disconnect with fundamentals is striking.

Q1 2026 revenue of $1.10 billion beat estimates by 4.87%, EPS of $0.12 matched, and GAAP net income jumped 134.45% YoY to $166.73 million. Loan originations hit a record $12.18 billion, up 68% YoY, and deposits reached $40.24 billion.

The Case for $24+

The bull thesis writes itself if you trust management’s guidance. SoFi has guided 2026 adjusted revenue to $4.655 billion (about 30% growth) with adjusted EBITDA near $1.6 billion at a 34% margin, plus a medium-term framework calling for 30%+ revenue CAGR and 38% to 42% adjusted EPS CAGR through 2028.

Catalysts are stacking up: the SoFiUSD stablecoin with Mastercard settlement, crypto trading rollout, Big Business Banking, and a Loan Platform Business that added $3.6 billion in new commitments last quarter.

Anthony Noto said the strategy is “delivering a winning combination of growth and returns”. Our bull case price is $24.73, a 44.39% return, achievable if the multiple rerates on Financial Services revenue growth (currently +41% YoY).

What Could Go Wrong

Bears point to real issues. The Technology Platform segment fell 27% YoY after a large client departure, enabled accounts dropped 16% YoY, and net interest margin compressed by 63 basis points. Credit metrics are softening too, with personal loan charge-offs ticking up to 3.03%.

That said, bulls would argue the Technology Platform weakness reflects one client exit rather than structural decline, and NIM compression is partly the cost of growing low-yield deposits aggressively, which funds over 90% of liabilities.

The Reddit crowd is split, with sentiment swinging from 72 (bullish) in mid-May to 22 (bearish) by month-end. Our bear case lands at $16.79, a modest 1.97% decline.

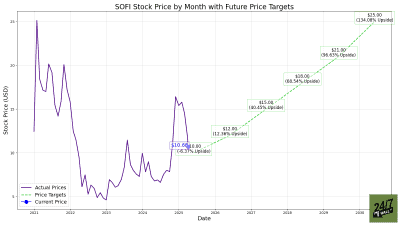

SoFi Price Prediction 2026-2030

The 24/7 Wall St. price target of $19.10 with a buy rating reflects my view that the YTD selloff has detached price from a fundamentally accelerating business.

The tipping factor is the loan-origination machine running at $12.18 billion per quarter against a stock trading at a forward P/E of 29x. I’d be a buyer here if Q2 2026 confirms 30%+ revenue growth and stable credit metrics. I’d stay on the sidelines if charge-offs jump above 3.5% or the Technology Platform loses another anchor client.

Looking further ahead, here is where our model projects SoFi could trade in coming years, assuming current growth trajectories and credit conditions hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $19.10 |

| 2027 | $21.50 |

| 2028 | $23.00 |

| 2029 | $24.20 |

| 2030 | $25.14 |

These projections assume SoFi executes on its 30%+ revenue CAGR guide. Significant upside could come from stablecoin or crypto monetization, while downside risk centers on credit deterioration or a deeper Technology Platform reset.

Contact [email protected] for any questions or corrections.