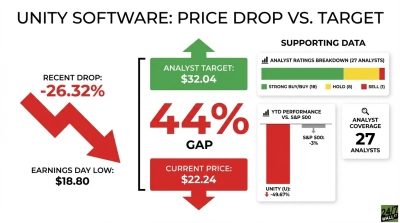

Unity Software (NYSE:U | U Price Prediction) occupies a curious intersection: a strategic asset with a depressed valuation. Shares closed most recently at $30.68, down 30.5% year to date, giving the company a market cap of roughly $13.4 billion. Yet the underlying business is accelerating: Q1 2026 revenue reached $508.24 million, up 16.8% year over year, and Vector, the AI ad engine, was 80% larger than a year ago.

CEO Matt Bromberg was blunt on the Q1 call: “There is no company in the world better positioned to win in this marketplace than we are.” CFO Jarrod Yahes added that “there is a high threshold as we evaluate M&A opportunities.” Unity has signaled discipline on M&A, yet the assets, the Unity 6 engine, Unity Runtime behavioral data, Vector, and roughly 70% mobile game creation market share, make it a magnet for larger platforms.

4. Apple: The Longest Shot

Apple (NASDAQ:AAPL), at a $317.31 share price and a $4.7 trillion market cap, has the cash. Vision Pro needs 3D content. But Apple prefers acqui-hires (i.e., buying a business primarily to recruit its talented employees), not $13 billion platform deals, and Unity’s ad business would clash with Apple’s privacy stance. Despite a strategic fit, cultural and regulatory friction dwarfs any strategic fit.

3. Microsoft: Regulatory Baggage

Microsoft (NASDAQ:MSFT) has the financial firepower ($2.9 trillion market cap, 46.3% operating margin) and gaming rationale via Xbox. Satya Nadella’s $37 billion AI run rate gives him ad-tech logic too. Post-Activision antitrust scrutiny makes another mega gaming deal a slog.

2. Sony: The Natural Fit

Sony (NYSE:SONY) is the intuitive buyer: PlayStation runs on developers who overwhelmingly use Unity. At a $20.68 share price, Sony has a $121.4 billion market cap, and its ¥500 billion buyback signals capital discipline. The obstacle is that swallowing a $13 billion U.S. software firm would be outside Sony’s typical M&A comfort zone.

1. Nvidia: The Strongest Case

Nvidia (NASDAQ:NVDA) fits best. Omniverse, Isaac GR00T, and DRIVE Hyperion all need a real-time 3D engine and developer network. Nvidia’s $4.9 trillion market cap and 63% profit margin mean Unity represents a rounding error on Nvidia’s balance sheet. Jensen Huang says, “Agentic AI has arrived,” and Unity Runtime’s behavioral data would supercharge simulation and robotics training. Antitrust risk is lower than Microsoft’s, and the industrial logic is highest. (For readers tracking this theme, 24/7 Wall St.’s Next Nvidia Playbook report frames the broader compute-plus-content stack.)

Where Private Equity Fits

A Thoma Bravo-style buyer could absorb Unity’s $403.9 million FY25 free cash flow and compress margins. But $2.15 billion in cash combined with a $2.24 billion convertible note stack complicates LBO math. PE ranks below Nvidia and Sony, roughly level with Microsoft, and ahead of Apple.

Contact [email protected] for any questions or corrections.