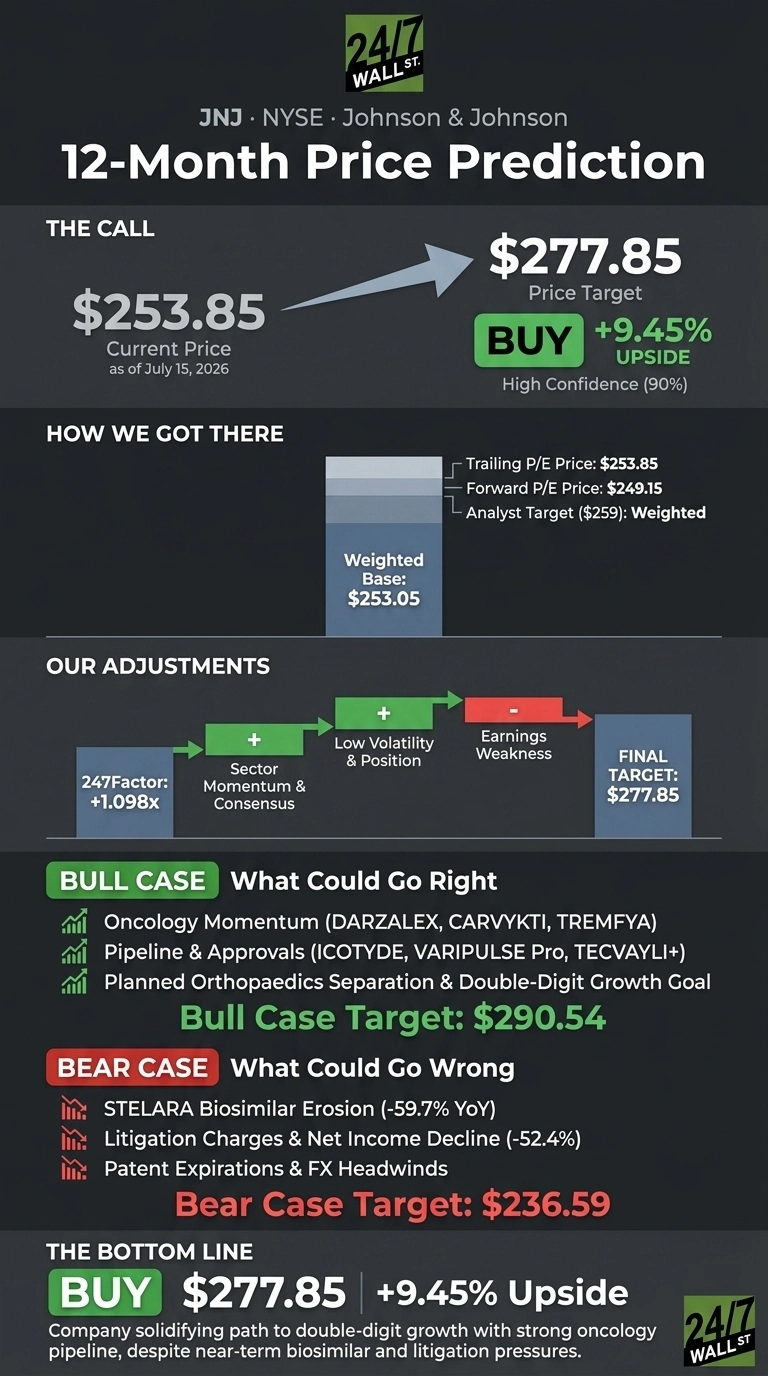

Johnson & Johnson (NYSE:JNJ | JNJ Price Prediction) is up 24.03% year to date and 65.92% over the past year, riding oncology strength and a raised full-year outlook. Our proprietary model sees room to run.

Our 24/7 Wall St. price target for JNJ is $277.85, implying 9.45% upside from the current $253.85. The recommendation is buy with 90% confidence, high by our standards for a mega-cap.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $253.85 |

| 24/7 Wall St. Price Target | $277.85 |

| Upside | 9.45% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Year of Accelerated Growth Is Playing Out

JNJ delivered Q1 2026 revenue of $24.06 billion, up 9.9% year over year, with adjusted EPS of $2.70 beating the $2.6773 consensus. Q2 2026 reinforced the trajectory with reported sales of $25.3 billion (up 6.6%) and adjusted EPS of $2.90, prompting another guidance raise.

Management now targets full-year revenue of $100.30 billion to $101.30 billion and adjusted EPS of $11.45 to $11.65. The stock traded as low as $155.89 in the past 52 weeks and now sits just below its $269.43 high after a 5.01% pullback in the last week.

Why Bulls See a Breakout Above $290

Oncology remains the engine. DARZALEX grew 22.5% to $3.96 billion in Q1, TREMFYA surged 68.3%, CARVYKTI jumped 62.1%, and RYBREVANT/LAZCLUZE climbed 82.7%. Recent approvals for ICOTYDE, VARIPULSE Pro, and TECVAYLI plus DARZALEX FASPRO extend the runway.

Management committed to double-digit growth by decade’s end, and the planned Orthopaedics separation could unlock a valuation re-rating. Our bull case price target over the next 12 months is $290.54, a 14.45% total return.

What Could Go Wrong

STELARA collapsed 59.7% to $656 million as biosimilar competition intensified, and litigation charges of $330 million weighed on GAAP net income, which fell 52.4%.

Bulls view the decline as optics driven by TREMFYA absorbing STELARA share, with the litigation charge running as a non-recurring item. Our bear case target is $236.59, a 6.8% drawdown if patent cliffs bite harder than expected.

How JNJ Compares to Merck and Pfizer

Merck (NYSE:MRK) is the closest oncology-driven comp given KEYTRUDA’s dominance. Merck guides 2026 non-GAAP EPS of $8.93-$9.03 on revenue of $64.3B-$64.8B, but a $0.37 Cidara acquisition charge muddies the trailing picture. JNJ’s diversified MedTech plus Innovative Medicine mix looks cleaner, supporting our target’s forward P/E of roughly 23.

Pfizer (NYSE:PFE) trades at a trailing P/E of just 14 with a dividend yield near 6%, versus JNJ’s 30 P/E and 2.01% yield. Pfizer looks statistically cheaper, but the discount reflects post-COVID revenue erosion and patent-cliff risk. JNJ’s premium is earned, and our target leaves room versus the sell-side consensus of $259.

I’d Buy It Here

The 24/7 Wall St. price target of $277.85 with 90% confidence and a buy rating reflects a company hitting on innovation while paying investors to wait through a 64th consecutive dividend increase.

I’d be a buyer if the December 8 Enterprise Business Review confirms the double-digit growth path. I’d stay sidelined if litigation charges reaccelerate or if the Orthopaedics separation gets delayed.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $277.85 |

| 2027 | $298.00 |

| 2028 | $318.00 |

| 2029 | $337.00 |

| 2030 | $356.79 |

These projections assume JNJ executes on its path toward double-digit growth by decade’s end. Significant upside or downside could result from oncology pipeline outcomes or the Orthopaedics separation.

Contact [email protected] for any questions or corrections.