The last 30 years have seen tremendous innovations, discoveries, creations, and strides made in medicine, technology, finance, and communications. The Baby Boomer generation has endured 4 major wars, the creation of satellites and space travel, the only foreign terrorist attack to kill thousands of Americans on US soil, social upheaval, and an ever-changing cultural society. They have also seen the creation of television, the internet, mobile phones, cancer drugs, prosthetics, and all other types of wonders that were only considered science fiction during the post-WWII era when many Baby Boomers spent their childhoods and adolescence.

As we near the start of the 21st Century’s second quarter, we can assess how assumptions and attitudes have had to change. A number of long-held beliefs that have been debunked, such as the safety of tobacco smoking and the food pyramid advocating a heavier carbohydrate ratio over protein to reduce obesity, have forced millions to revise their lifestyle health habits. This has led other industries to re-examine and alter their own policies and practices accordingly.

Old Dogs and New Tricks For Retirement

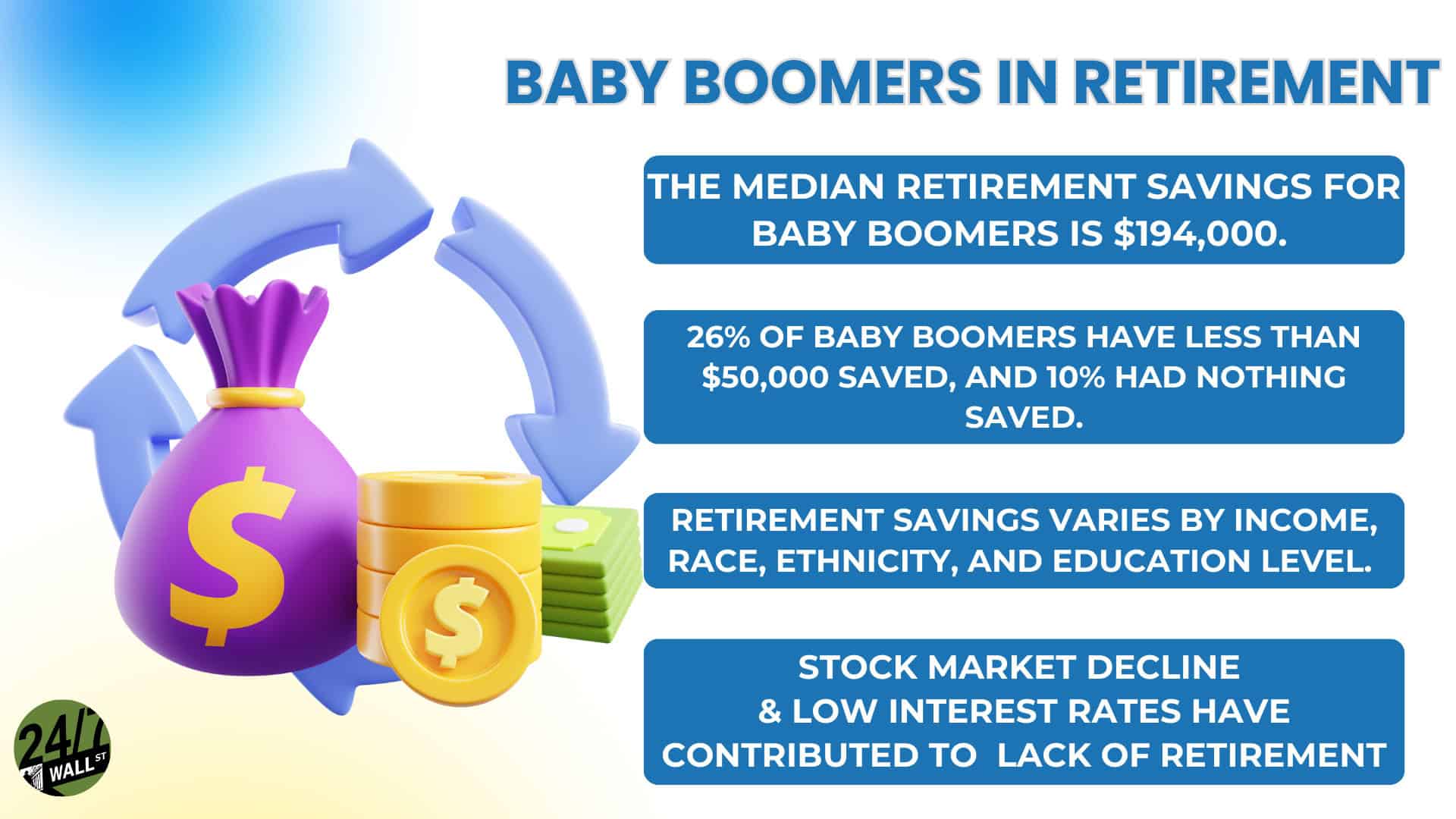

Baby Boomers whose retirement savings are being managed under assumptions developed during the Reagan, Bush or even Clinton administration years may find themseves in a shortfall in the modern era, due to inflation, longer lifespans, and government agency insolvency.

There are several retirement shibboleths that far too many Baby Boomers on the edge of retirement still believe, much to their own detriment. Inflation, market volatility, taxes, and a panoply of other factors have changed both the playing field and the rulebook, but many Boomers and their advisors still haven’t read it.

Old Dogs:

Here are a few former principles that are no longer valid in today’s economic climate.

- The “Guardrails” Withdrawal Strategy – The traditional 4% rule, predicated on 1980s growth, has been largely superseded by the Guardrails approach. Current 2026 data suggests a safe starting withdrawal rate of approximately 3.9%, with the flexibility to adjust spending by 5-10% during significant market downturns to preserve portfolio longevity over 40-year horizons.

- The Age Calculation For Stock/Bond Portfolio Holdings – Another obsolete financial management practice was to subtract one’s age from 100 to determine the percentage of stocks vs. bonds. Again, this was a ratio predicated on the notion that the financial environment during the Reagan era would not change. Modern strategies favor a more aggressive equity tilt or dynamic allocation to combat the effects of modern inflation.

- Social Security Legislative Updates – While solvency concerns remain, the 2025/2026 implementation of the Social Security Fairness Act has significantly altered the landscape. This legislation eliminated the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO), providing benefit relief to millions of retirees who were previously penalized by these rules.

- Retirees Must Be Completely Debt Free Before Retirement – while carrying as little debt as possible is an optimal goal, manageable debt should not be paid off with tax-deferred retirement money for a number of reasons that may involve reduced portfolio appreciation rates, tax penalties, and other downsides.

New Tricks:

There are a number of contemporary strategies that can be deployed to address the current and constantly shifting economic landscape that has some built-in flexibility for adjustments as warranted.

- 2026 HSA and Medicare Realities – For the 2026 tax year, HSA contribution limits have risen to $4,400 for individuals and $8,750 for families, plus catch-up provisions. This is critical as Medicare Part B premiums reached $202.90/month in 2026, often outpacing annual Social Security COLA increases.

- Fixed Index Annuities (FIAs) and RILAs – As the need for guaranteed income grows, FIAs and Registered Index-Linked Annuities (RILAs) with “Dual Direction” segments have gained popularity. These tools allow for growth tied to market indices while providing a safety valve against market decreases, with some 2026 configurations even allowing for positive returns during minor market dips.

- Broad Market and Small-Cap Diversification – Over-reliance on the “Magnificent 7” tech stocks has given way to a 2026 pivot toward broader indices. Diversifying into Small-Cap U.S. stocks (S&P 600) and emerging markets (MSCI EAFE) is currently favored as these sectors frequently outperform top-heavy indices in the current economic cycle.

- Inflation Hedges and $36 Trillion Debt – The national debt exceeding $36 trillion remains a persistent inflation threat. Portfolios are increasingly incorporating direct holdings in commodities like oil, food, and precious metals mining, alongside REITs to capture rental income streams without the burdens of direct property management.

- 2026 Contribution Maximization – Retirees should leverage the 2026 “Super Catch-up” for ages 60–63, which allows for a total contribution cap of $35,750 in workplace plans. Attention should also be paid to maximizing Roth conversions to allow for tax-free growth and withdrawals.

- Tax Planning and RMDs When withdrawal time comes, it is important to try to stay in as low a tax bracket as possible to minimize tax bites. Current rules generally require Minimum Distributions (RMDs) to begin at age 73 or 75 depending on birth year, making early planning for tax-deferred accounts essential.

- Other Retirement Income: If the retiree has passive income from real estate rental properties or other holdings that are listed under Form 1099, making a business out of a hobby can generate additional tax deductions, which are often pooled together under 1099, unless large enough to require itemization. If the new business can create a profit in 2 out of 5 years, the IRS will continue to allow it.

Editor’s Note: This article has been updated to include 2026 IRS contribution limits for HSAs and retirement accounts, current Medicare Part B premium costs, and the impact of the Social Security Fairness Act regarding WEP and GPO provisions. The financial strategies section now features contemporary research on the “Guardrails” withdrawal method and a shift in diversification focus toward small-cap and emerging market indices.

Contact [email protected] for any questions or corrections.