Financial expert Dave Ramsey has long argued that the questions people ask themselves are a reliable predictor of where they will end up financially. Wealthy people, he says, consistently direct their thinking toward solutions, skill-building, and long-term opportunity. Those who struggle with money tend to get trapped by questions that assign blame rather than drive action.

According to Ramsey, people who build lasting financial security ask how they can grow, what they can learn, and how they can keep moving forward even in difficult times. That outward orientation toward action and responsibility creates habits that compound over the years into real stability.

The contrast with financially stuck individuals is sharp. Ramsey points out that people mired in debt frequently ask why life is unfair or why nothing ever works out for them. Those questions, he argues, lead to discouragement and inaction. Shifting toward empowering, solution-focused questions is, in his view, the first and most important step toward breaking the cycle.

The Heavy Yoke of Debt

According to Debt.com, 1 in 3 Americans have maxed out their credit cards.

According to Experian, the average American now carries $104,755 in total consumer debt as of June 2025, spanning mortgages, credit cards, auto loans, and student loans. The national debt burden shows no signs of easing, with the federal government continuing to add roughly $1 trillion to its obligations every fiscal quarter.

The scale of the consumer credit industry is visible in the market values of its biggest players. Visa Inc. (NYSE:V | V Price Prediction) trades around $320 per share, well below its 52-week high of $375.51, while the consensus analyst price target across 38 Wall Street analysts now stands at approximately $399. Rival Mastercard (NYSE:MA) trades near $570, with analysts carrying a consensus 12-month target of roughly $647. Both companies continue to benefit directly from the growth in credit card borrowing.

That borrowing has reached historic levels. Total U.S. credit card balances hit $1.21 trillion as of Q2 2025, one of the highest totals on record and up more than 6% from the prior year. A Debt.com survey captured the pressure behind those numbers, with American respondents reporting:

- 45% have had to use credit cards to pay for staples, due to inflation-fueled higher prices.

- 9% have had a financial emergency requiring use of a credit card.

- 35% have maxed out their credit cards.

- 85% of those with maxed out credit cards blamed inflation and higher prices as the overwhelming factor in prompting card use.

- 22% were carrying credit card debt between $10,000 and $20,000.

- 5% were carrying credit card debt in excess of $30,000.

Solutions

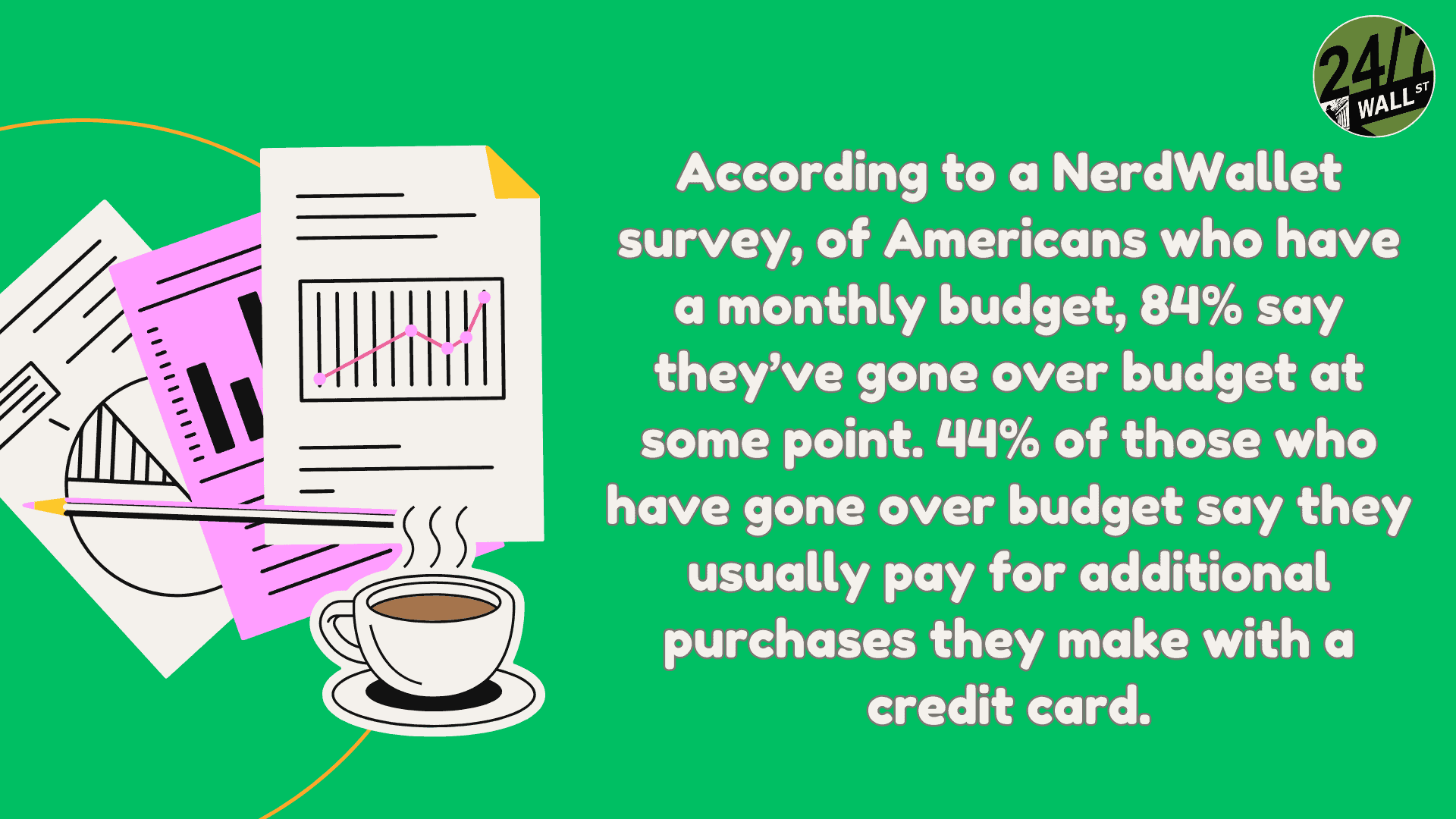

Ramsey’s core principle is straightforward: if you cannot pay for it, do not buy it. Putting that advice into practice has become harder as relentless digital marketing reaches people through social media, email, streaming, and print around the clock. The friction between Ramsey’s philosophy and the modern spending environment has never been greater.

Given ongoing economic uncertainty and the need to maintain a financial cushion for emergencies, canceling credit cards outright is rarely practical. There are, however, concrete steps that anyone working to reduce debt can take:

- Make a weekly budget and start saving. Even setting aside a small amount each week, once current expenses are covered, builds a meaningful habit and a growing cushion. A written weekly budget also clarifies the difference between spending on needs versus wants, giving an honest picture of where cash is actually going so that lifestyle adjustments become easier to see and act on.

- Eliminate the habitual use of credit cards. Switching to cash and debit cards makes it immediately obvious how closely a budget is being followed. Buying a $10 meal on a high-interest card and carrying a balance can easily double the real cost of that purchase over time, depending on how long the debt lingers and at what rate.

- Look for debt consolidation options. Locking in a lower interest rate and using it to consolidate high-rate balances can turn an unmanageable pile of revolving debt into a single, structured monthly payment. The goal is to accelerate paying down the principal, rather than endlessly servicing interest.

Editor’s note: This article was updated to reflect current average American consumer debt of $104,755 per Experian (June 2025), total U.S. credit card balances of $1.21 trillion as of Q2 2025 per Federal Reserve Bank of New York data, and revised Visa and Mastercard share prices and analyst consensus price targets as of June 2026.

Contact [email protected] for any questions or corrections.