Financial advice radio host Dave Ramsey typically fields calls about specific personal situations, but one broader theme surfaces repeatedly on his show: the mindset gap that separates wealthy people from those who struggle financially.

According to Ramsey, the question a rich person asks when presented with a purchase is simply: “How much?” A poor person, by contrast, asks: “How much is the down payment?” The distinction sounds minor, but the financial consequences are compounding and severe.

Wealthy people weigh the full price and whether they can pay it outright. People living paycheck to paycheck anchor their decision to the entry cost alone, ignoring the interest rate, the risk of job loss, and every unexpected expense that could derail repayment. The total bill, once interest is added, often dwarfs the original sticker price by a significant margin.

The Heavy Yoke of Debt

According to Debt.com, 1 in 3 Americans have maxed out their credit cards.

Consumer Debt by the Numbers

The scale of American indebtedness gives Ramsey’s warning real urgency. According to Experian’s 2025 Consumer Credit Review, the average American carried $105,444 in total debt as of September 2025, spanning mortgages, auto loans, student loans, and credit cards. The Federal Reserve Bank of New York’s Q1 2026 Quarterly Report on Household Debt and Credit put total U.S. household debt at $18.8 trillion, a figure that has climbed roughly $4.6 trillion since the end of 2019. Credit card balances fell a seasonal $25 billion in Q1 2026 to stand at $1.25 trillion, down from the record $1.28 trillion set in Q4 2025. Even so, that Q1 2026 balance still represents a 5.9% jump from a year earlier, a reminder that the seasonal dip masked persistent long-run growth. Average interest rates on cards accruing balances reached 22.15% in Q2 2026, according to the Federal Reserve’s G.19 report, meaning the cost of carrying debt has rarely been higher.

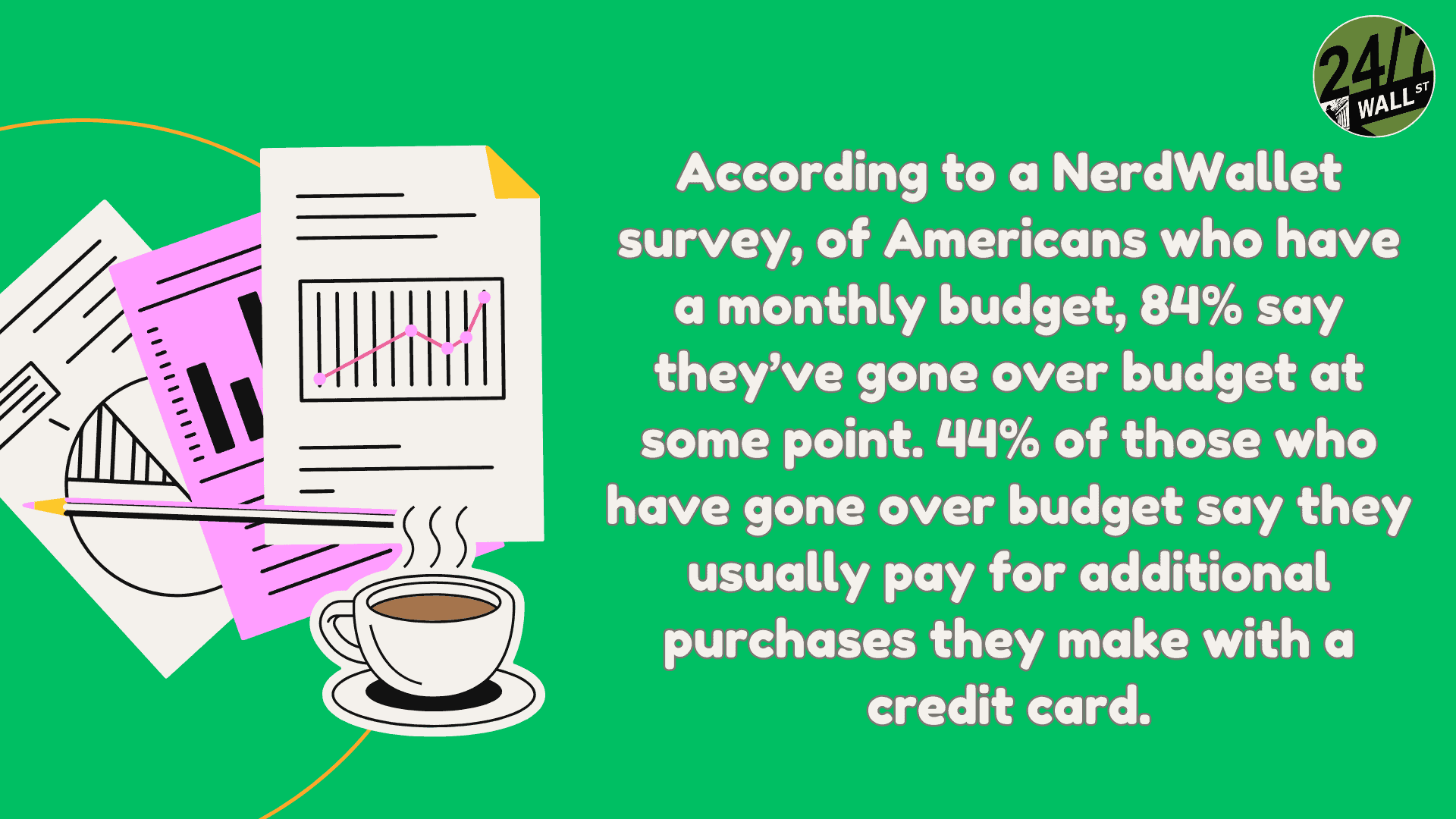

The Credit Card Survival Gap

A March 2026 survey by Debt.com paints a stark picture of how dependent many households have become on revolving credit. More than half of U.S. adults (55%) now use credit cards as their primary financial lifeline for basic necessities such as groceries, rent, and utilities. The emergency dependence figure is even more alarming: 61% of respondents said they would have to rely on a credit card to cover a sudden financial emergency, the highest share in three years. Among those who have already maxed out at least one card (46% of respondents), eight in ten say they would still turn to credit in a crisis.

The survey also found that 57% of respondents carrying larger balances than the previous year cited persistent inflation as the primary driver. Nearly three in ten (29%) are now carrying credit card debt of $10,000 or more, up sharply from 23% in 2025. Those figures illustrate a worsening cycle: inflation pushes spending onto credit, high interest rates stall payoff, and balances compound into long-term debt burdens that take years to escape.

The Credit Industry Behind the Numbers

The businesses that profit from this behavior remain among the most valuable in the world. Visa (NYSE:V | V Price Prediction) and Mastercard (NYSE:MA) together process trillions of dollars in transactions annually, and their revenue grows every time a consumer swipes instead of pays cash. That dynamic makes the debt cycle self-reinforcing: the more Americans borrow, the more the payment networks earn, and the more infrastructure exists to make borrowing frictionless and fast.

Modernizing the Trap: Buy Now, Pay Later

Ramsey’s original warning targeted the financing desk at a car lot or appliance store, but the same psychological trap has migrated online. Buy Now, Pay Later (BNPL) apps have restructured the down-payment mindset for everyday e-commerce. According to a J.D. Power survey, 37% of U.S. consumers used a BNPL service in the 90 days ending in 2025, up five percentage points year over year. Monthly per-user BNPL spending rose roughly 21% between June 2024 and June 2025, according to Empower research. The psychological mechanics mirror what Ramsey describes: by stripping out the immediate friction of spending real money, these platforms encourage consumers to budget around micro-payments rather than total cost. And the risk is growing. About 41% of BNPL users reported making at least one late payment in the past year, according to LendingTree data, reinforcing exactly the habit Ramsey warns against.

The Generational Debt Divide

The debt burden does not fall evenly across generations. Experian data shows that Generation X carries the nation’s heaviest non-mortgage debt load, with credit card balances running at least 24% higher than millennials’ and 35% higher than baby boomers’. Gen X carries an average credit card balance of $9,600, compared to $6,961 for millennials and $6,795 for baby boomers, per Experian’s 2025 consumer debt study. Millennials face a different squeeze: they carry the largest average mortgage balance of any generation at approximately $320,000, the result of buying or refinancing homes when rates were at multi-decade highs. Gen Z enters adulthood with the lowest average debt overall, but that picture is shifting quickly as student loan and auto loan balances climb.

Enjoying our content? Click the Follow button above to see more from us.

Ramsey’s core message comes down to one simple rule: do not buy something you cannot afford outright. In a world saturated by targeted advertising across social media, streaming, email, and every digital surface, that discipline is harder to maintain than at any prior point in history.

Completely abandoning credit lines is impractical for most households, particularly given lingering inflation pressures and emergency costs that regularly exceed savings balances. Even so, people working to build wealth can take concrete steps to escape the payment-plan trap:

- Apply a cash-friction rule. If you cannot comfortably pay for an item twice over in cash today, you cannot afford it on a payment plan. This rule forces a full-cost calculation rather than a monthly-payment calculation.

- Stop using credit cards for daily consumables. Using cash or debit for groceries and everyday staples creates immediate feedback on spending, preventing the slow accumulation of high-interest balances on routine purchases.

- Convert variable-rate balances into fixed-rate debt. With credit card APRs exceeding 22%, rolling revolving balances into a fixed-rate personal consolidation loan removes the compounding risk and sets a defined payoff timeline.

Editor’s note: This update corrects the Experian average consumer debt figure to $105,444 as of September 2025 (from the full-year Experian 2025 Consumer Credit Review), adjusts the millennial average mortgage balance to approximately $320,000 per Experian June 2025 data, adds the finding that Q1 2026 credit card balances remain 5.9% above a year earlier despite the seasonal decline, incorporates Q2 2026 average credit card APR data (22.15% for interest-accruing accounts) from the Federal Reserve G.19 report, and adds the statistic that 41% of BNPL users made at least one late payment in the past year per LendingTree data.

Contact [email protected] for any questions or corrections.