Millions of Americans are working to put money away for retirement, with results that vary enormously from household to household. The number falling critically short is staggeringly high, putting a large share of the population at risk of a financially strained retirement that could last two decades or more.

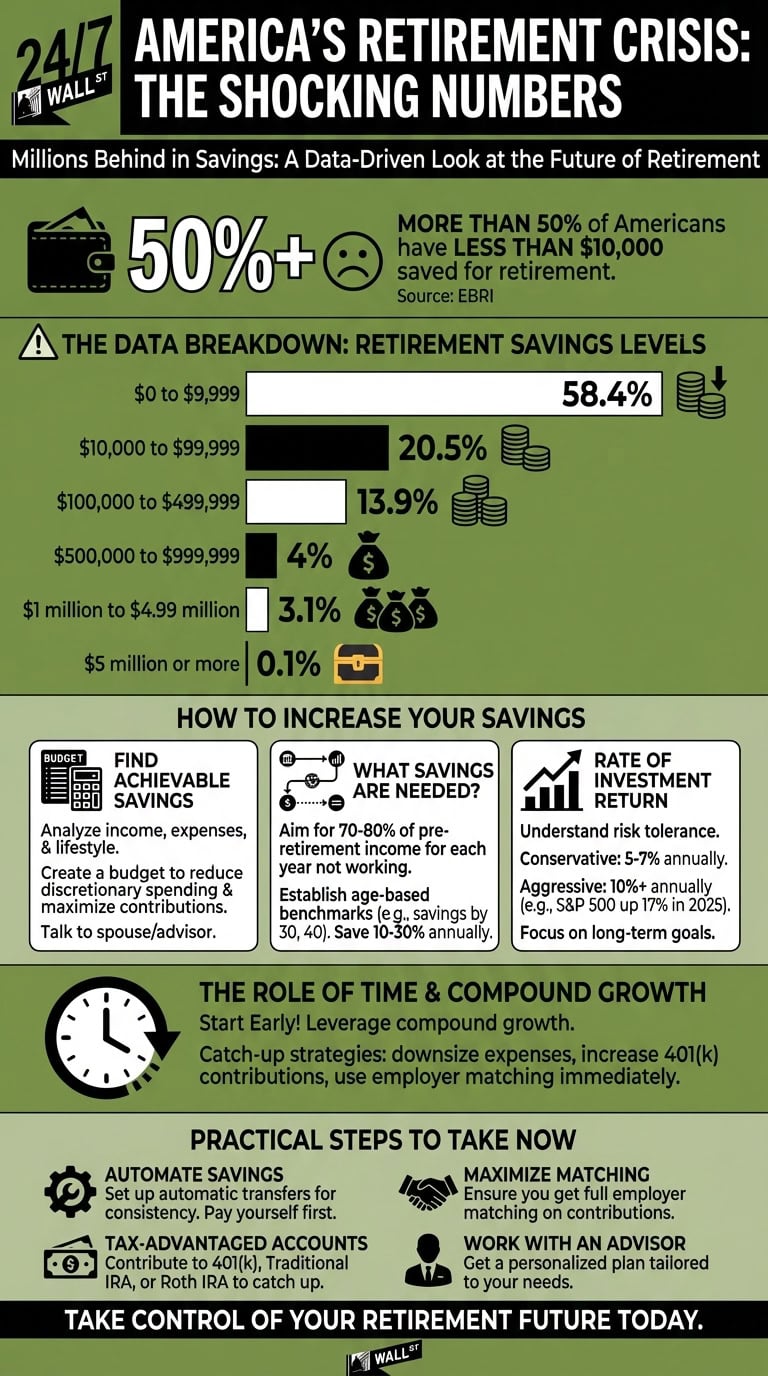

According to the Employee Benefit Research Institute, more than half of Americans have less than $10,000 saved for retirement. That figure is troubling on its own, but it grows more striking when set against the far smaller share who have actually crossed the $500,000 threshold.

The Data Breakdown

The EBRI data paints a stark portrait of where Americans actually stand, regardless of what they believe they need. The distribution of retirement account balances reveals a widening gap between those who have saved meaningfully and the majority who have not:

- $0 to $9,999: 58.4%

- $10,000 to $99,999: 20.5%

- $100,000 to $499,999: 13.9%

- $500,000 to $999,999: 4%

- $1 million to $4.99 million: 3.1%

- $5 million or more: 0.1%

Fewer than 8% of Americans have crossed the half-million-dollar mark. Nearly 4.1 million Americans were set to turn 65 in 2025 alone, which means this wave of retirees is entering a system where only a small fraction have built the kind of cushion financial planners consider adequate for a comfortable, multi-decade retirement.

The Inflation Factor: COLA and Purchasing Power

A $500,000 nest egg sounds substantial, but its real-world value is being steadily eroded by inflation. The Senior Citizens League (TSCL), a nonpartisan advocacy group, now projects the 2027 Social Security cost-of-living adjustment at 3.8%, a sharp jump from the 2.8% COLA that took effect in January 2026. That upward revision reflects a surge in energy prices tied to the conflict in Iran, which has restricted oil flow through the Strait of Hormuz and pushed CPI-W inflation to 3.9% year-over-year as of April 2026. Independent analyst Mary Johnson has put her own estimate even higher, at 4.7%, citing the likelihood that energy-driven price pressures will persist through the July-September measurement window that determines the official COLA. A higher COLA sounds like welcome news, but it signals that prices are outpacing the projections built into most retirement plans.

The deeper problem is structural. The CPI-W measures prices for urban wage earners rather than retirees, so it understates the health care and housing costs that dominate a senior’s budget. According to TSCL’s 2026 Loss of Buying Power report, Social Security benefits have lost 13.7% of their purchasing power since 2010. That erosion shows up directly in monthly income: the average check for all beneficiaries was $1,933 in April 2026, while retired workers specifically averaged $2,026. Meanwhile, TSCL’s 2026 Senior Survey found that 44% of retirees now depend on Social Security for all their income, up from 39% in 2025, a sign that other income sources are failing to keep pace. Diversified income strategies, including equities and annuities, are essential tools for protecting a portfolio’s real purchasing power over a long retirement.

Legislative Relief: The Social Security Fairness Act

Public sector workers received significant financial relief when the Social Security Fairness Act was signed into law on January 5, 2025. The legislation repealed the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO), two rules that had reduced Social Security benefits for millions of teachers, police officers, firefighters, and other government employees whose jobs were not covered by Social Security. By July 2025, the Social Security Administration had already completed sending over 3.1 million payments totaling $17 billion to eligible beneficiaries, five months ahead of schedule.

The practical effect for affected public servants is a meaningful boost in monthly income, cash flow that can be redirected into retirement savings. The repeal is retroactive to January 2024, so many recipients have also collected lump-sum payments covering prior reductions. Beyond the federal change, a growing number of states are phasing out their own taxes on Social Security income, which can further increase effective take-home pay in retirement.

What Role Does Time Play? Leveraging Super Catch-Ups

Starting early remains the most reliable path to a strong retirement balance, but the SECURE 2.0 Act created a powerful tool for those who are starting later. Workers aged 60 to 63 can now take advantage of super catch-up contributions, an enhanced limit that exceeds the standard age-50-plus catch-up. For 2026, the super catch-up stands at $11,250, which replaces (rather than stacks on top of) the standard $8,000 catch-up for that age group. Added to the base deferral limit of $24,500, eligible savers can put up to $35,750 per year into an employer-sponsored 401(k) before counting any employer matching contributions.

To illustrate the impact: a late starter who reaches age 60 with $250,000 saved and maximizes these contributions over a four-year window at a 7% average annual return could add roughly $163,000 in principal and compounded growth, closing nearly a third of the remaining gap to a half-million-dollar balance. The window is narrow, expiring when the participant turns 64, so confirming that your employer’s plan has adopted the super catch-up provision is an important first step. The IRS confirmed in Notice 2025-67 that the $11,250 super catch-up limit applies for 2026.

The Mandatory Roth Catch-Up Rule

High earners who want to use these enhanced limits face a new wrinkle under SECURE 2.0. Beginning January 1, 2026, workers whose FICA wages from their current employer exceeded $150,000 in the prior year must route all catch-up contributions into a Roth account rather than a traditional, pre-tax account. This applies to all catch-up contributions, including the super catch-up for those aged 60 to 63.

Paying taxes upfront on catch-up contributions reduces take-home pay in the short term, but the trade-off is tax-free growth and tax-free qualified distributions in retirement. For high earners who expect to remain in elevated tax brackets throughout their later years, that structural benefit can more than offset the immediate cost. One important caveat: if an employer’s plan does not currently offer a Roth option, the plan will need to add one before high-earning participants can make any catch-up contributions at all under the new rules.

Rate of Investment Return and Portfolio Volatility

The return assumptions built into a retirement plan matter enormously over a multi-decade horizon. A conservative 5% to 7% annual return is a reasonable baseline for a diversified portfolio, while more aggressive savers who concentrate in equities often target 10%. In the current market environment, with AI-driven technology stocks commanding elevated valuations, the higher end of that range is achievable but comes with meaningful volatility risk.

As balances approach the $500,000 mark, the nature of risk shifts in an important way. A poorly timed market correction at the start of retirement can permanently impair a portfolio, because withdrawals lock in losses before the portfolio has time to recover. Financial planners call this sequence-of-returns risk, and it is one reason why gradually shifting to a more conservative allocation in the five years before retirement is standard advice for anyone who cannot afford a deep early drawdown.

Practical Steps You Can Take

Automating contributions remains the simplest way to build consistency. Payroll deferrals remove the temptation to spend first and save later, and automatic increases tied to raises can push savings rates higher without requiring active decisions year after year. Beyond 401(k)s and IRAs, the tax treatment of withdrawals deserves careful attention. As state-level Social Security taxation continues to evolve, coordinating Roth conversions with a qualified advisor can lower the effective tax rate on retirement income and preserve more of that hard-earned balance for actual living expenses rather than tax bills.

Editor’s note: The 2027 COLA forecast was updated from 3.9% to 3.8%, reflecting TSCL’s revised June 2026 estimate, with independent analyst Mary Johnson’s higher 4.7% projection added for context. The buying power loss figure in the body was corrected from “nearly 14%” to 13.7% to match TSCL’s 2026 Loss of Buying Power report, and new TSCL data showing that 44% of retirees now depend entirely on Social Security income (up from 39% in 2025) and the April 2026 average monthly benefit of $2,026 for retired workers were added to the inflation section.

Contact [email protected] for any questions or corrections.