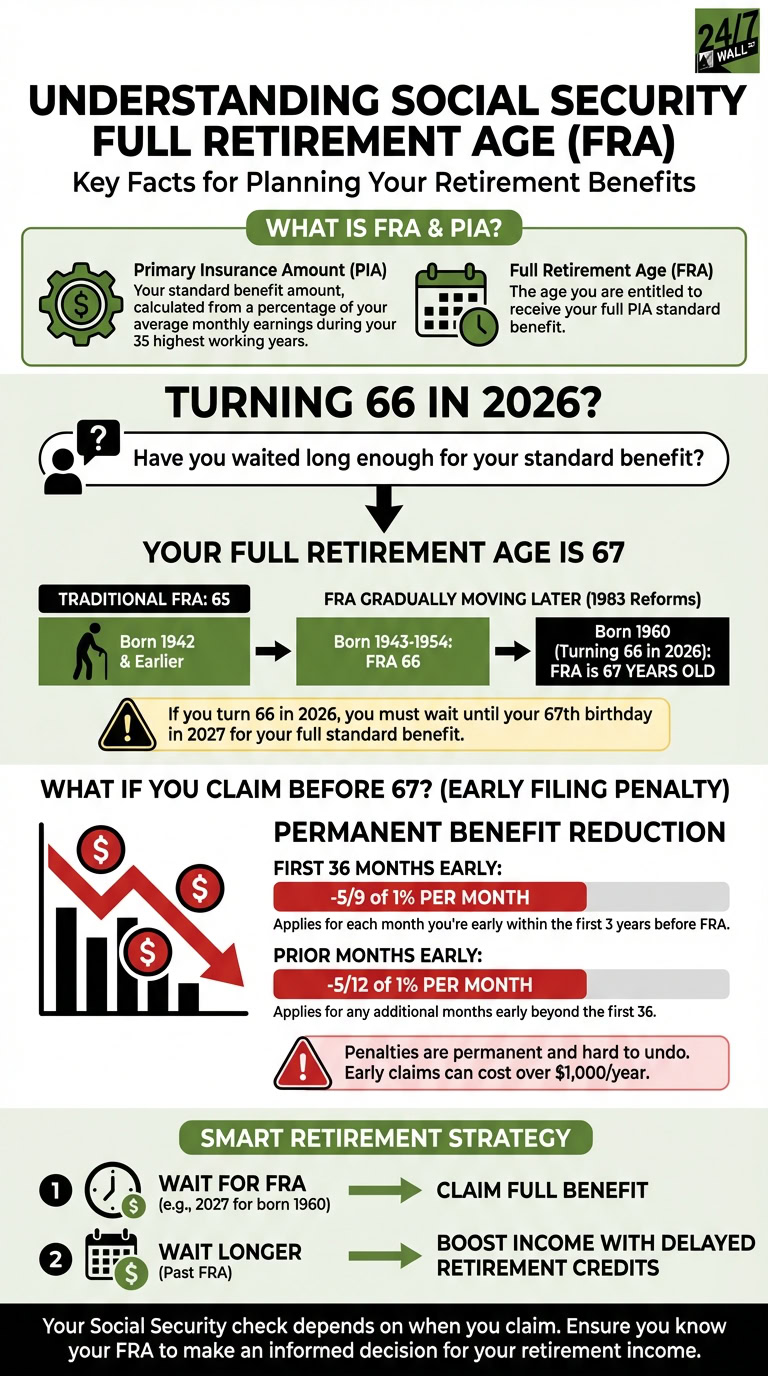

When you collect Social Security, you’re entitled to a standard benefit. This amount is called your primary insurance amount (PIA) and it’s calculated based on a percentage of your average indexed monthly earnings (AIME) during your 35 highest-earning working years.

You receive this standard benefit when you claim your first Social Security check at full retirement age (FRA). Although you become eligible to start benefits at 62, FRA falls several years after that. Traditionally, FRA was 65, but that has not been the case for quite some time.

So, if you’re turning 66 this year, have you waited long enough?

This is your full retirement age if you turn 66 in 2026

Full retirement age has gradually moved later as a result of the 1983 Social Security reforms Congress passed to stabilize the program’s finances. FRA started at 65, then shifted to 66 for people born between 1943 and 1954. For anyone born after that, FRA has continued moving back by two months for each birth year.

If you are turning 66 in 2026, you were born in 1960. For anyone born that year, full retirement age is 67. By comparison, those who turned 66 in 2025 were born in 1959, and their FRA was 66 years and 10 months, meaning the 1960 birth year marks the final step in a decades-long transition to the highest FRA currently allowed under law.

This means that turning 66 in 2026 does not entitle you to full benefits. For most people in this cohort, claiming at the standard benefit level will require waiting until their 67th birthday in 2027. The good news is that the 2026 cost-of-living adjustment of 2.8% has already lifted benefit amounts, with the average retired worker now receiving roughly $2,071 per month, according to the Social Security Administration.

What happens if you claim before 67?

Finding out you may need to delay your benefits claim longer than planned can be frustrating, but understanding the cost of an early claim matters before you make a decision you cannot easily reverse.

When you file for benefits ahead of your full retirement age, a permanent early filing penalty applies for each month you are early. For each of the first 36 months before FRA, you lose 5/9 of 1% of your benefit. For any month beyond those first 36, the reduction is 5/12 of 1%. The total penalty for someone born in 1960 who claims at 62 reaches 30%, dropping what would otherwise be a full benefit down to just 70 cents on the dollar. In concrete terms, the maximum monthly benefit at FRA in 2026 is $4,152, while the maximum for claiming at 62 falls to $2,969, a gap of more than $1,180 per month that persists for life.

Early filing penalties are permanent, and reversing an early claim is difficult. The only real option is to rescind your claim within 12 months of approval and repay every dollar of benefits received to that point.

The upside of waiting past 67

For those who can afford to delay past their FRA birthday in 2027, the reward is meaningful. Social Security awards delayed retirement credits of 8% per year for every year you hold off claiming beyond FRA, up to age 70. That means waiting until 70 instead of 67 can increase your monthly benefit by up to 24% above your PIA, a higher base that also applies to future cost-of-living adjustments.

If you are still working while you wait, keep the 2026 earnings test thresholds in mind. Before FRA, Social Security withholds $1 for every $2 you earn above $24,480 per year. In the year you reach FRA, a more generous threshold applies: $1 is withheld for every $3 earned above $65,160. Once you hit your full retirement age, the earnings test disappears entirely.

The bottom line for anyone turning 66 in 2026: your FRA is your 67th birthday in 2027. Claiming before then permanently reduces your check, while waiting until 67 or beyond locks in a higher benefit for the rest of your retirement.

Editor’s note: This article was updated to reflect the confirmed 2026 COLA of 2.8%, the current maximum monthly benefit figures at 62 ($2,969) and at full retirement age ($4,152), the 8% annual delayed retirement credit for waiting past FRA, and the 2026 earnings test thresholds of $24,480 (under FRA) and $65,160 (in the year of FRA).

Contact [email protected] for any questions or corrections.