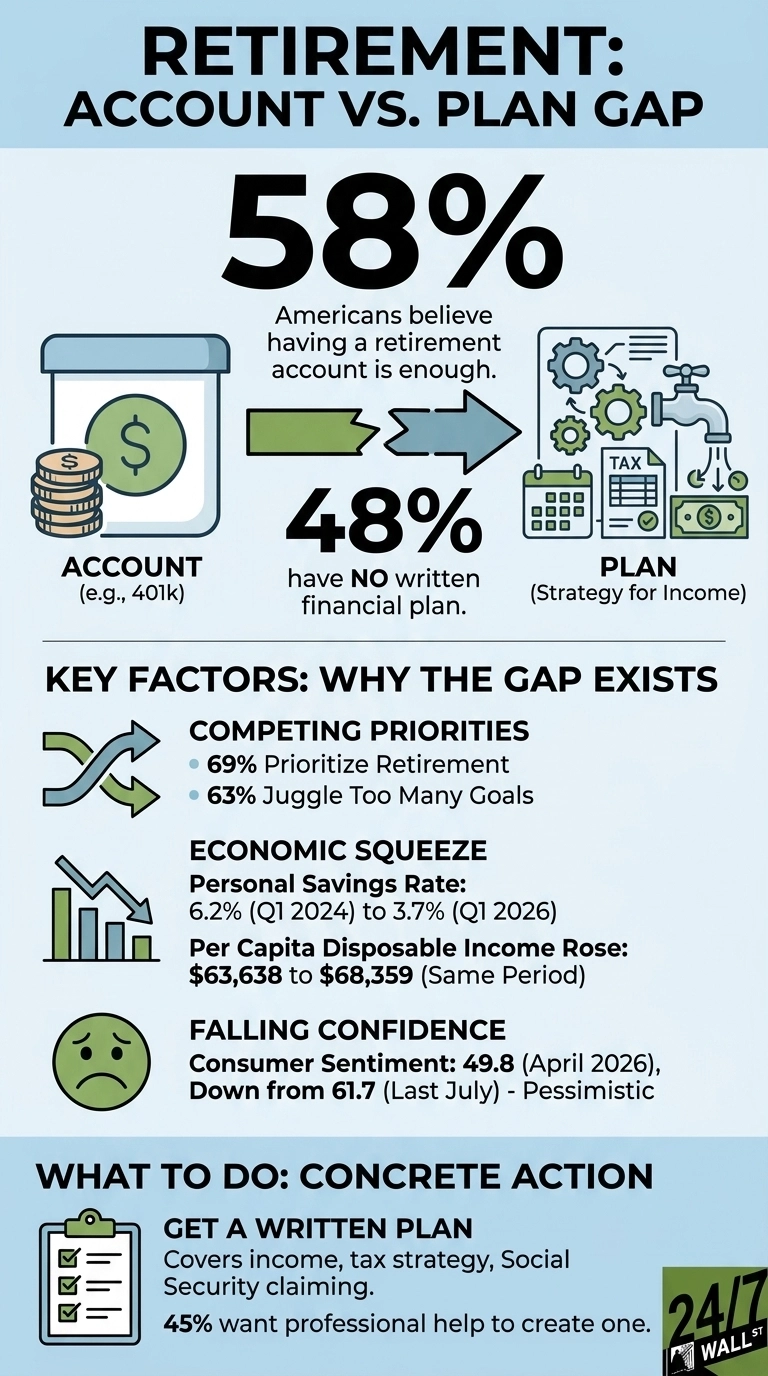

The Allianz Center for the Future of Retirement 2026 Annual Retirement Study arrived with a finding that is easy to misread on first pass. 58% of Americans believe that simply having a retirement account like a 401(k) or IRA will be enough to retire on. In the same survey, 48% have no written financial plan, and 56% admit they don’t know what else they should be doing to prepare for retirement. The country has, in large numbers, confused the vehicle with the destination.

The distinction matters because the two activities solve different problems. Saving accumulates assets. A retirement plan creates a strategy for converting those accumulated assets into a sustainable, tax-efficient stream of income in retirement. A 401(k) balance is a number on a screen. A plan is the set of decisions that turns that number into a paycheck that lasts 25 or 30 years, accounts for taxes, adjusts for inflation, and survives a bad market in year three.

The Gap Between Having an Account and Having a Strategy

For most of the working population, the account exists because an employer set it up. Contributions happen by default. Investment allocations were chosen once, often during onboarding, and rarely revisited. That is saving, which is distinct from planning. Planning answers a different set of questions: when to claim Social Security, which accounts to draw down first, how much to convert to a Roth and in which years, what to do with required minimum distributions, how to handle health care before Medicare, and what the withdrawal rate should actually be once the paychecks stop.

Those questions are answered by a plan, not by the existence of a 401(k) on its own. A plan addresses them directly. And the survey suggests the plan, for nearly half the country, does not exist on paper at all.

Why Planning Keeps Getting Pushed Off

The competing priorities are real. 69% say saving for retirement is a top priority, but 63% juggle so many financial goals it’s hard to focus, with day-to-day expenses, credit card debt, mortgage obligations, and health care costs taking precedence. The macro backdrop reinforces the squeeze. The personal savings rate has fallen from 6.2% in the first quarter of 2024 to 3.7% in the first quarter of 2026, even as per capita disposable income rose from $63,638 to $68,359 over the same period. Income rose while the savings rate declined.

Sentiment reflects the same pressure. The University of Michigan Consumer Sentiment Index sits at 49.8 as of April 2026, down from 61.7 last July, a reading the index itself classifies as pessimistic and approaching recessionary levels. CPI hit 332.4 in April 2026, the highest reading in the measured period. Average hourly earnings reached $37.41 in April 2026, up from $36.12 a year earlier, but rising costs and falling confidence make long-horizon planning feel like a luxury when the next bill is the more urgent problem.

What an Actual Plan Looks Like

A written retirement plan covers four things the account itself does not. First, a target income number in retirement, expressed in today’s dollars and adjusted for the inflation rate that compounded the CPI reading above. Second, a withdrawal sequence across taxable, tax-deferred, and Roth accounts, designed to manage the tax bracket year by year. Third, a Social Security claiming decision, which can swing lifetime benefits by tens of thousands of dollars depending on the age elected. Fourth, a contingency for the years before age 65 when Medicare is not yet available and private coverage is the largest single line item.

The survey points to where this is most likely to come from. 45% of Americans without a written financial plan would like to work with a professional to create one, yet most are not currently meeting with one despite identifying financial professionals as their top source of guidance. The willingness exists, while the follow-through lags.

The Allianz data points to a narrow and specific gap. A retirement account is a container. A retirement plan is the set of instructions for what to do with what is in the container, and when, and in what order. 58% of Americans treat the first as if it were the second. That is the gap. Closing it requires a document, a sequence, and a set of decisions that the account, on its own, will never produce.

Data Sources

- Allianz Center for the Future of Retirement 2026 Annual Retirement Study: Source of the central planning-gap statistics, including the 58% account-is-enough finding, the 48% no-written-plan figure, and the 56% don’t-know-what-else-to-do figure.

- Allianz Center for the Future of Retirement 2026 Annual Retirement Study: Source of the competing-priorities data (69% prioritize retirement, 63% juggle too many goals) and the 45% interested-in-professional-guidance figure.

Contact [email protected] for any questions or corrections.