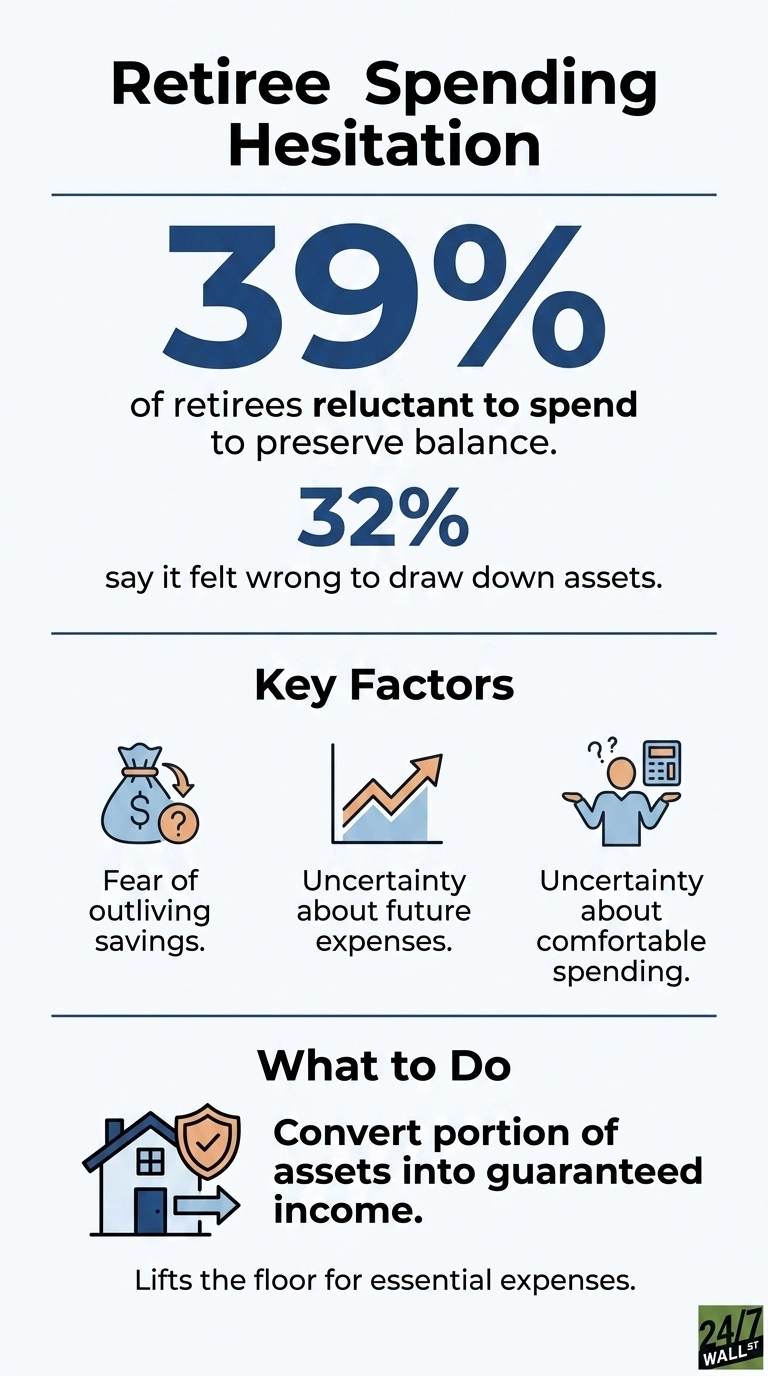

The Allianz Center for the Future of Retirement 2026 Annual Retirement Study surfaced a finding that rarely gets attention in standard personal finance coverage. After decades of disciplined saving, a meaningful share of retirees cannot bring themselves to use the money they set aside. Thirty-two percent say it felt wrong to start drawing down their assets after accumulating them for decades, and 39% are reluctant to spend money to preserve their account balance. The number that goes on the retirement projection is only half the story, and the behavior that follows is the other half, and it is the part most pre-retirees never plan for.

The Habit That Will Not Switch Off

Forty years of saving builds a reflex: when the paycheck arrives, a slice goes to the 401(k), and the rest gets budgeted. Retirement is supposed to flip that reflex: the portfolio becomes the paycheck. The Allianz data documents how often that switch fails to flip. The research identifies three core reasons: fear of outliving savings, uncertainty about future expenses, and uncertainty about how much they can comfortably spend. None of those concerns is unreasonable, and all three are reinforced by the current environment.

Inflation is the most obvious reinforcement. Core PCE, the Federal Reserve’s preferred inflation gauge, sits at the 90.9th percentile of its historical distribution as of April 2026, with the index climbing from 126.1 in June 2025 to 129.6 in April 2026. CPI tells the same story, hitting 332.4 in April 2026 after rising in nearly every month over the prior year. For a retiree drawing from a finite pot, every monthly grocery bill is a reminder that the pot has to stretch further than it did a year ago.

Pre-Retirees Are Calibrating to the Wrong Number

The Allianz study also exposes a calibration problem at the other end of the timeline: 60% of non-retired Americans expect to spend less than 75% of their current spending in retirement, while 45% of actual retirees report spending less than 75% of their current spending. The gap between expectation and reality is the meaningful figure. Pre-retirees are planning for a leaner future than most retirees actually live in, which understates the income they will need and makes the eventual decision to spend feel riskier than it is.

Macro consumption data points in the same direction. Healthcare spending alone climbed from $3,649.4 billion in November 2025 to $3.7 trillion in April 2026, and housing services rose from $3.8 trillion to $3,930.7 billion over the same period. Two of the largest categories in a retiree’s budget keep getting bigger, regardless of how much someone tried to budget them down in their planning spreadsheet.

The Savings Rate Is Falling, and the Cushion Is Thinner

The broader population is already spending more of what comes in. The personal savings rate has fallen from 6.2% in the first quarter of 2024 to 3.7% in the first quarter of 2026. University of Michigan consumer sentiment registered 49.8 in April 2026, a recessionary reading and down from 61.7 in July 2025. The macro backdrop validates retiree caution at a gut level, even when the math on an individual portfolio would support steady drawdowns.

Why Guaranteed Income Quiets the Anxiety

The Allianz study points to one factor that consistently lowers the psychological barrier. The survey takeaway indicates that 77% say a guaranteed income stream in retirement would reduce their anxiety about spending. Social Security is the largest such stream for most households, and the BEA data confirms its scale. Social Security transfer receipts totaled $1.6 trillion in the first quarter of 2026, up from $1.4 trillion two years earlier. A predictable monthly check covers essential expenses, reframing portfolio withdrawals as funding for everything above the floor rather than as survival money that might run out.

A Number Without a Spending Plan Is Half a Plan

The retirement industry spends most of its energy on the accumulation question: how big a balance is enough. The Allianz data argues that the decumulation question deserves equal weight. The study frames spending strategy as essential to retirement planning, noting that a retirement strategy starts with understanding what spending will realistically look like after leaving the workforce.

Pre-retirees calibrating to a 75% replacement rate should pressure-test that assumption against categories that keep rising regardless of personal choice, healthcare, and housing in particular.

Retirees uncomfortable with portfolio withdrawals can convert a portion of assets into guaranteed income to lift the floor, which the Allianz survey suggests is the single most effective lever for reducing spending anxiety. A balance is one input; a spending plan is what determines how those balance funds are used for retirement.

Contact [email protected] for any questions or corrections.