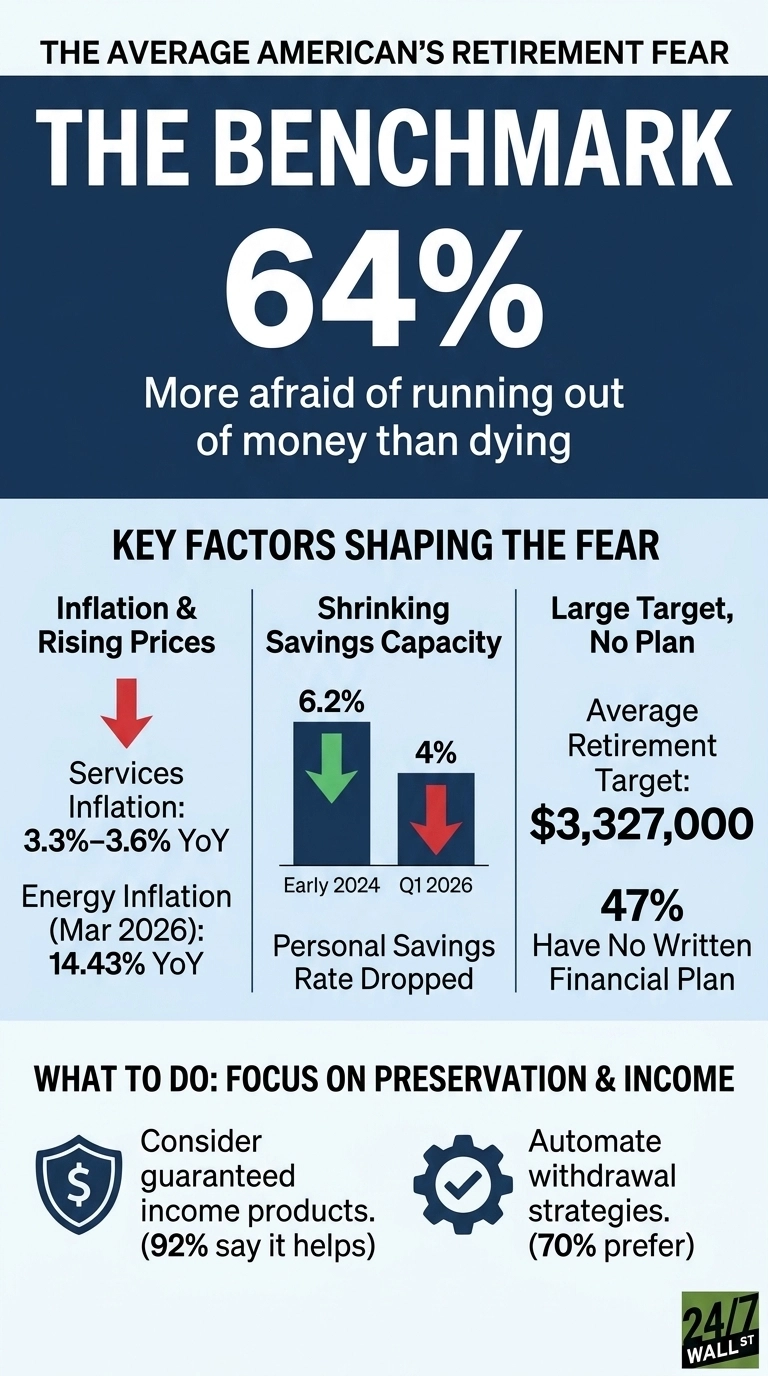

The Allianz study makes the hierarchy of financial fear unmistakable. A clear majority of Americans report that the possibility of running out of money outweighs the fear of death itself, a finding captured in the line from the report that says “64% worry more about running out of money than death itself.” When respondents were asked to compare the two outcomes, retirement presents, the end of their savings carried more weight than the end of their lives.

The sources of that anxiety are spelled out in the data. High inflation tops the list, with 64% citing rising prices as a driver of their concern. A significant share, 54%, worry that Social Security will not provide enough support.

Several pressures cluster together at 43%, including high taxes, everyday expenses becoming unaffordable, and the possibility of a market downturn eroding savings. Healthcare costs and the risk of outliving assets complete the picture. The fear is not abstract. It is a straightforward arithmetic problem in which prices rise, income eventually stops, and the gap between the two becomes the central threat to retirement security.

The inflation data matches the fear

Inflation continues to shape the financial backdrop. The Consumer Price Index reached 330.3 in March 2026, a 1.1% increase from the prior month and a reading that sits near the top of its 12‑month range. The Federal Reserve’s preferred measure, core PCE, registered an index value of 129.28, and services inflation, which captures healthcare, rent, and personal care, has held between 3.3% and 3.6% year over year for months. Those are the categories retirees cannot easily trim, and they are the ones that have remained the most persistent.

Energy adds another layer of instability, as the PCE energy index rose 14.43% year over year in March 2026 after posting a slightly negative reading just one month earlier. That kind of swing lands directly on the utility bill and the gas pump for a fixed‑income household. It is the practical reminder that a retiree’s monthly budget cannot be set once and left untouched, because the inputs that determine the cost of living do not move in straight lines.

Savings capacity is shrinking

The latest BEA release shows a personal savings rate that continues to thin out. The rate sits at 4% in the first quarter of 2026, down from 5.2% a year earlier and from 6.2% in early 2024. Per‑capita disposable income reached $68,617 on an annualized basis, but the additional income has not translated into a stronger cushion.

The Allianz survey reflects that pressure directly. A majority of respondents, 55%, say they are not saving enough to meet their long‑term financial goals, and 62% cite competing priorities, such as daily expenses and debt, as the reason. Confidence has slipped as well. The share of Americans who feel able to support the lifestyle they want in retirement has fallen from 83% in 2020 to 70% in 2025, a decline of thirteen percentage points that mirrors the broader strain households report.

The number people think they need

Among Americans with savings goals, the average target for a comfortable retirement is $3,327,000. Yet only 45% know how they will convert their savings into income, and 47% have no written financial plan, even among active contributors to retirement accounts. A further 59% admit they do not know what else to do to prepare. In other words, while the target might be large, the path to it is unclear, which is the structural condition that produces the fear in the first place.

The broader picture is also weak

The University of Michigan Consumer Sentiment Index stood at 48.2 in April 2026, well below the 60-recession threshold and at the 27th percentile historically. The 10-year Treasury yield closed at 4.38% on May 8, 2026, off its 2025 peak of 4.58%, a move that affects annuity rates and safe withdrawal math in meaningful ways. Unemployment held at 4.3% in April 2026, technically healthy, though the layoff risk that derails a savings plan never reaches zero.

Behavioral shift toward preservation

The Allianz study points to a behavioral shift that matches the macro picture, as 74% of Americans would rather own products that protect against major losses, even if it means giving up bigger gains, 92% say guaranteed income would help them financially support their desired life, and 70% prefer automatic withdrawal strategies. The definition of retirement security has shifted from accumulation toward preservation, from upside toward certainty.

Inflation has compounded faster than the savings rate has recovered, the target retirement number sits in the millions, and most households lack a written plan to reach it. Those conditions track with the survey finding that 64% of Americans worry more about running out of money than about dying.

Contact [email protected] for any questions or corrections.