Fidelity’s 2026 Retirement Planning Study lands at a moment when Americans have plenty to be anxious about. The University of Michigan Consumer Sentiment Index sat at 49.8 in April 2026, deep in recessionary territory and well below the 60-point threshold that signals broad financial stress. Moreover, the personal savings rate has slipped from 5.2% in the first quarter of 2025 to 3.7% in the first quarter of 2026.

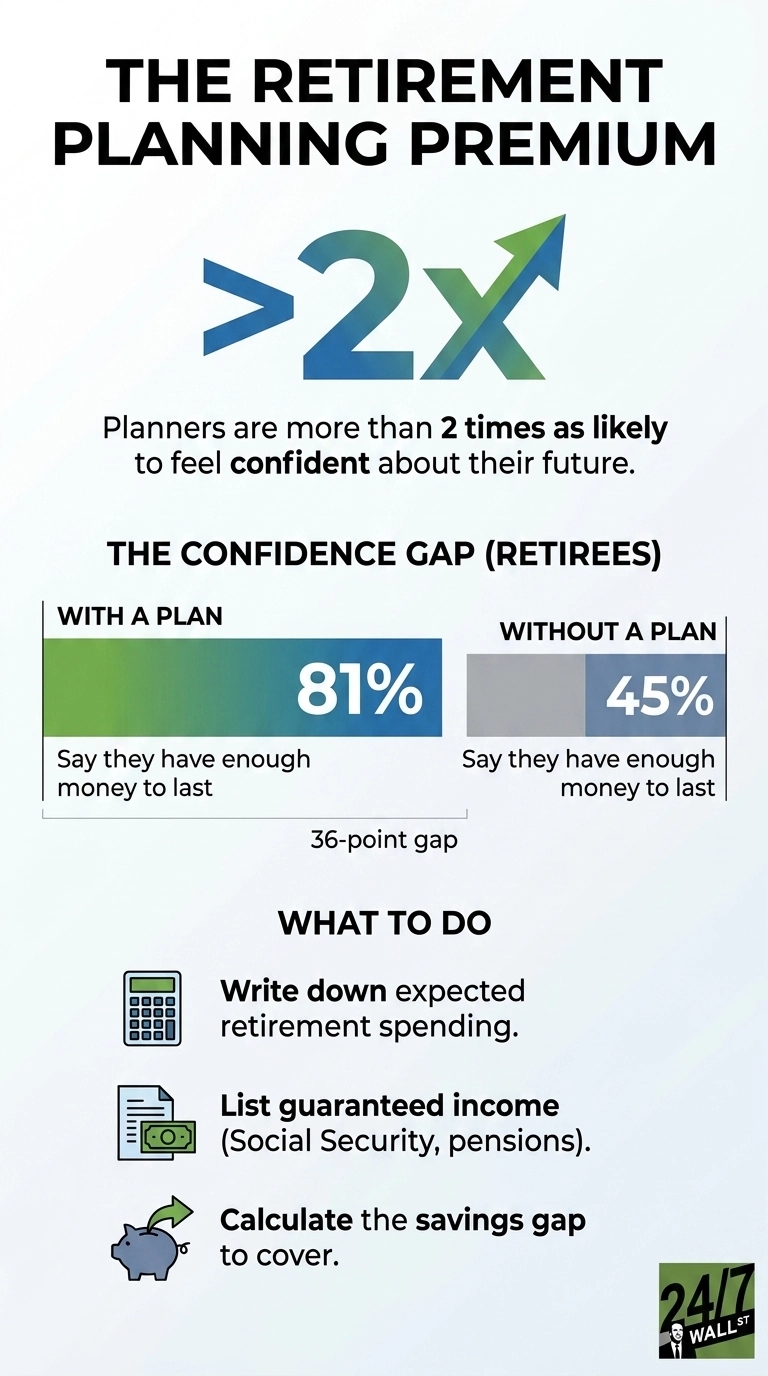

Against that backdrop, the study found something simple and striking: people who have actually written down a retirement plan are more than twice as likely to feel confident about their future as those who have not.

The headline number, the closing number, and almost every figure in between describe the same gap. Call it the planning premium: the difference between treating retirement as a calculation and as a hope.

What the Planning Premium Actually Buys

The study found that 74% of Americans say they have a plan to reach their retirement goals, and 90% agree that planning is still necessary even in retirement. That second number matters more than it looks. Retirement used to be framed as a finish line. The people in this survey describe it as a job that continues, with withdrawal sequencing, tax decisions, and spending adjustments that require ongoing management.

The planners are also doing the work that compounds quietly over decades, as 66% recognize that an IRA and a 401(k) play different roles and should be used differently. In total, 38% are actively contributing to tax-advantaged accounts, and 15% have completed Roth conversions. None of those decisions happens by accident. They happen because someone sat down, looked at their income, and asked which account would do more work for them this year and which would do more work in retirement.

Why the Confidence Gap Is So Wide

Confidence in retirement reflects knowing the numbers, and a written plan forces a household to confront three questions at once: how much income will be needed, where it will come from, and how long it has to last. Once those answers exist on paper, the unknowns shrink. Without a plan, every market headline becomes a personal threat.

The macro picture explains why that matters right now. Core PCE inflation, the Federal Reserve’s preferred gauge, climbed to 129.63 in April 2026, continuing a steady erosion of purchasing power. The Consumer Price Index reached 332.4 in April 2026, up 0.6% in a single month. Unemployment held at 4.3% in May 2026, which is healthy on paper but offers little comfort to anyone watching their grocery bill. A retiree without a plan is absorbing all of that uncertainty with no framework to filter it. A retiree with a plan already knows what their next withdrawal will look like.

The Retiree Reality Gap

Among people who are already retired, the difference between planners and non-planners is no longer theoretical. The study indicates that 81% of retirees who had a plan say they have enough money to last the rest of their lives. Among retirees without a plan, only 45% say the same. That is a 36-percentage-point gap between two groups who, on paper, are at the same stage of life.

Eight in ten planners feel financially secure for the rest of their lives. Fewer than half of non-planners do. The non-planners are operating without the document that tells them whether their money fits their life. In a year when the savings rate is falling and sentiment is at recessionary lows, the absence of that document is the difference between sleeping at night and not.

The Planning Premium in Practice

The planning premium is available to anyone willing to write down three things: expected annual spending in retirement, expected guaranteed income from Social Security and any pension, and the gap between those two numbers that personal savings will need to cover. That single page is what separates the 81% from the 45%. It does not require an advisor, a product, or a market call. It requires a quiet afternoon and a willingness to put real numbers on paper.

The data shows that planners know where they stand. In 2026, with sentiment depressed and savings rates falling, knowing where one stands is most of the battle.

Contact [email protected] for any questions or corrections.