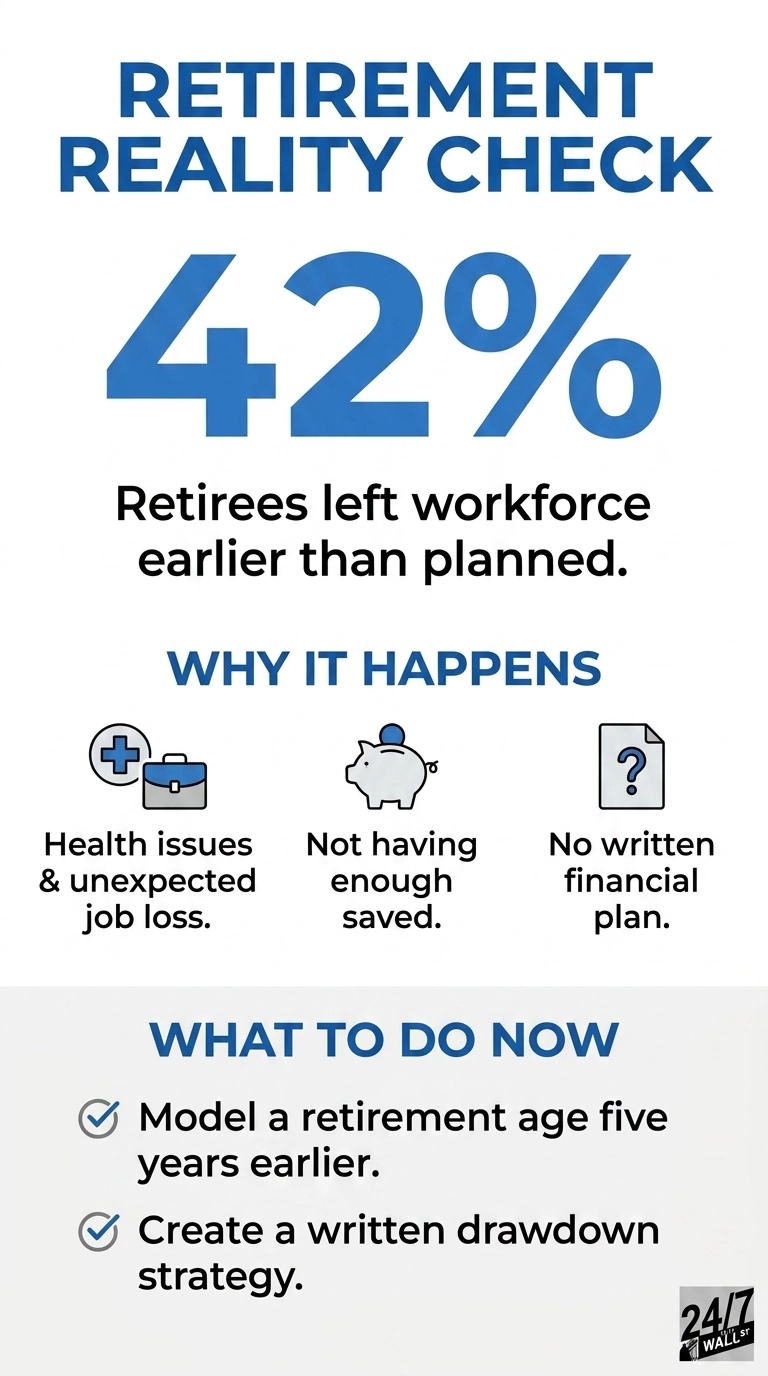

Retirement planning usually assumes a target date that the worker controls. The data say otherwise: 42% of retirees left the workforce earlier than expected, with health issues and unexpected job loss cited as the leading causes, according to the Allianz Center for the Future of Retirement’s 2026 Annual Retirement Study. Only 53% retired when they planned, and just 5% retired later. In other words, a plan built around a chosen retirement age is, for nearly half of workers, a plan built around a date that never arrives.

The financial mechanics of an early exit are unforgiving. Leaving the workforce ahead of schedule reduces the number of years spent saving and adds years the portfolio must fund. The Allianz study describes this as a “unique financial risk” precisely because the two variables move in opposite directions simultaneously. A worker who planned to retire at 67 but instead leaves at 62 loses five years of contributions and compounding, and gains five years of withdrawals. The same balance has to stretch further from a smaller starting point.

The Readiness Gap

Most Americans are not positioned to absorb that hit: 57% say not having enough saved is the biggest obstacle to retiring on their own terms, and 41% cite too many financial unknowns as a barrier. Those two answers point to the same underlying problem. Savings balances are below where they need to be, and the variables that determine whether those balances will last, like inflation, health costs, and market returns, are difficult to forecast, even for people paying close attention.

The macro backdrop is not helping. The personal savings rate has fallen from 6.2% in the first quarter of 2024 to 3.7% in the first quarter of 2026, according to the Bureau of Economic Analysis. Consumer sentiment sat at 49.8 in April 2026, down from 61.7 in July 2025, and initial jobless claims rose 18.4% over the prior month. This means that Americans are saving less of a smaller cushion at a moment when the labor market is showing the first signs of softening.

Saving Versus Planning

A second finding from the Allianz data further complicates the picture: 58% of Americans believe that simply having a retirement account, such as a 401(k), 403(b), or IRA, will be enough, and 48% do not have a written financial plan. In total, 56% admit they do not know what else they should be doing beyond contributing to a retirement account. Building a retirement balance and converting that balance into a sustainable, tax-efficient income stream are two different exercises. The first is largely automatic for anyone with payroll deductions. The second requires decisions about withdrawal order, claiming age, tax bracket management, and sequence-of-returns risk.

The Northwestern Mutual 2025 Planning & Progress Study put the target at $1.26 million for the average American and $1.57 million for Gen X. 51% of respondents think it is somewhat or very likely they will outlive their savings, and 35% have not taken any steps to address it. Among Gen X specifically, 54% do not think they will be financially prepared for retirement.

Risk Aversion Without a Strategy

The Allianz study also captured how Americans feel about market exposure, with 74% saying they would rather have financial products that protect against major losses, even if it means giving up bigger gains, and 57% feeling anxious about their financial well-being when retirement accounts suffer losses. That preference is consistent with the broader anxiety in the consumer sentiment data, though it functions as a preference rather than a complete plan. Risk aversion provides retirement security only when paired with a withdrawal strategy and a contingency plan for an early exit.

A Plan That Works Five Years Early

Planning for an on-time retirement without a contingency for an early one leaves a gap most households cannot afford. Three adjustments tend to address the early-exit risk directly. The first is to model the plan with a retirement age five years earlier than the target and check whether the projected income still covers fixed expenses. The second is a written drawdown strategy that names which accounts are tapped first and how Social Security claiming fits in, rather than treating the existence of a 401(k) as the strategy itself. The third is a cash reserve sized to cover the gap between an unexpected exit and the earliest Social Security claiming age of 62, so a forced retirement does not also force an early claim at a permanently reduced benefit.

Contact [email protected] for any questions or corrections.